Key Takeaways

- Overdependence on a concentrated Chinese customer base and rising in-house equipment development by key clients threaten revenue stability and long-term market share.

- Stricter global regulations and slower technological advancement intensify cost pressures and limit growth, with industry headwinds casting doubt on sustained profitability.

- Market leadership in advanced semiconductor equipment, robust R&D and global customer diversification underpin strong long-term growth, stable earnings, and resilience to supply chain risks.

Catalysts

About Kokusai Electric- Engages in the development, manufacture, sale, repair, and maintenance of semiconductor manufacturing equipment worldwide.

- Kokusai Electric's heavy reliance on large orders from a limited number of Chinese memory customers leaves its revenue base exceptionally vulnerable to Chinese government policy decisions, supply chain realignment, and further escalation in US-China technology tensions, which could result in sudden and sustained revenue declines as export controls tighten or Chinese customers pivot to local equipment suppliers.

- Increased capital intensity and compliance costs driven by more stringent global environmental regulations risk squeezing Kokusai Electric's operating margins, as they must spend more on R&D for energy-efficient manufacturing and meet higher reporting and material standards without guaranteed pricing power or meaningful operating leverage.

- The slowdown in process node advancement across the industry, as reflected in the flattening of Moore's Law, is leading to longer equipment replacement cycles at major foundries, which directly suppresses future wafer fab equipment spending and, in turn, aligns Kokusai Electric's long-term revenue growth much closer to sluggish semiconductor wafer volume rather than more robust leading-edge transitions.

- The ongoing demographic headwinds from aging populations in developed economies and slower enterprise IT hardware demand growth mean that the secular uplift from digitalization, cloud, and EVs could be offset by a structural plateauing in semiconductor volumes, undercutting Kokusai Electric's projections of sustained growth and potentially leading to long-term EPS stagnation or decline.

- Rapid adoption of in-house equipment development, particularly by top-tier Asian foundries and memory makers, threatens to permanently erode Kokusai Electric's addressable market, as more customers opt to develop proprietary wafer process equipment, increasing competitive pressure, driving down pricing, and embedding significant uncertainty into the company's longer-term revenue and profit forecasts.

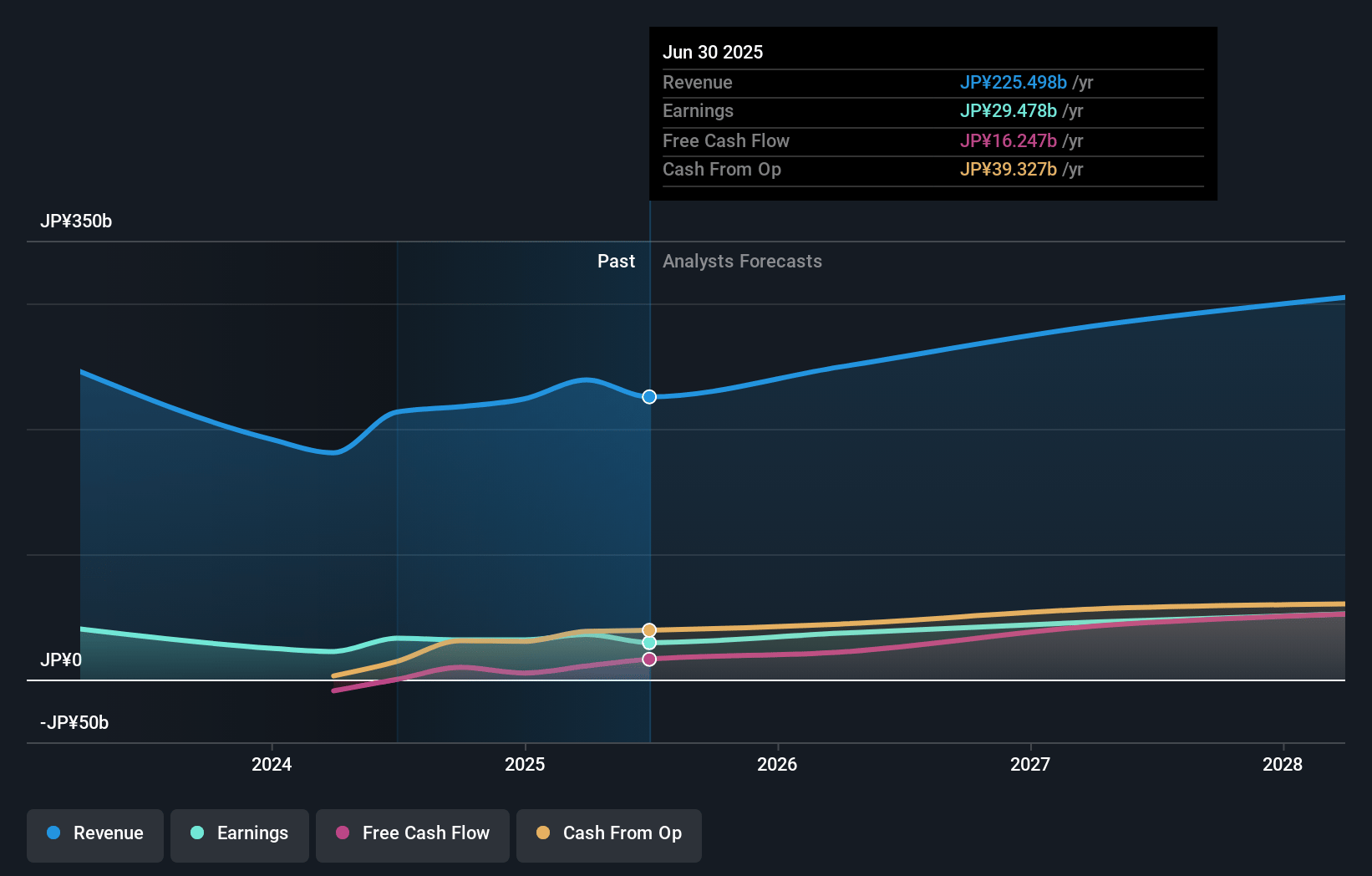

Kokusai Electric Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Kokusai Electric compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Kokusai Electric's revenue will grow by 7.5% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 15.1% today to 16.6% in 3 years time.

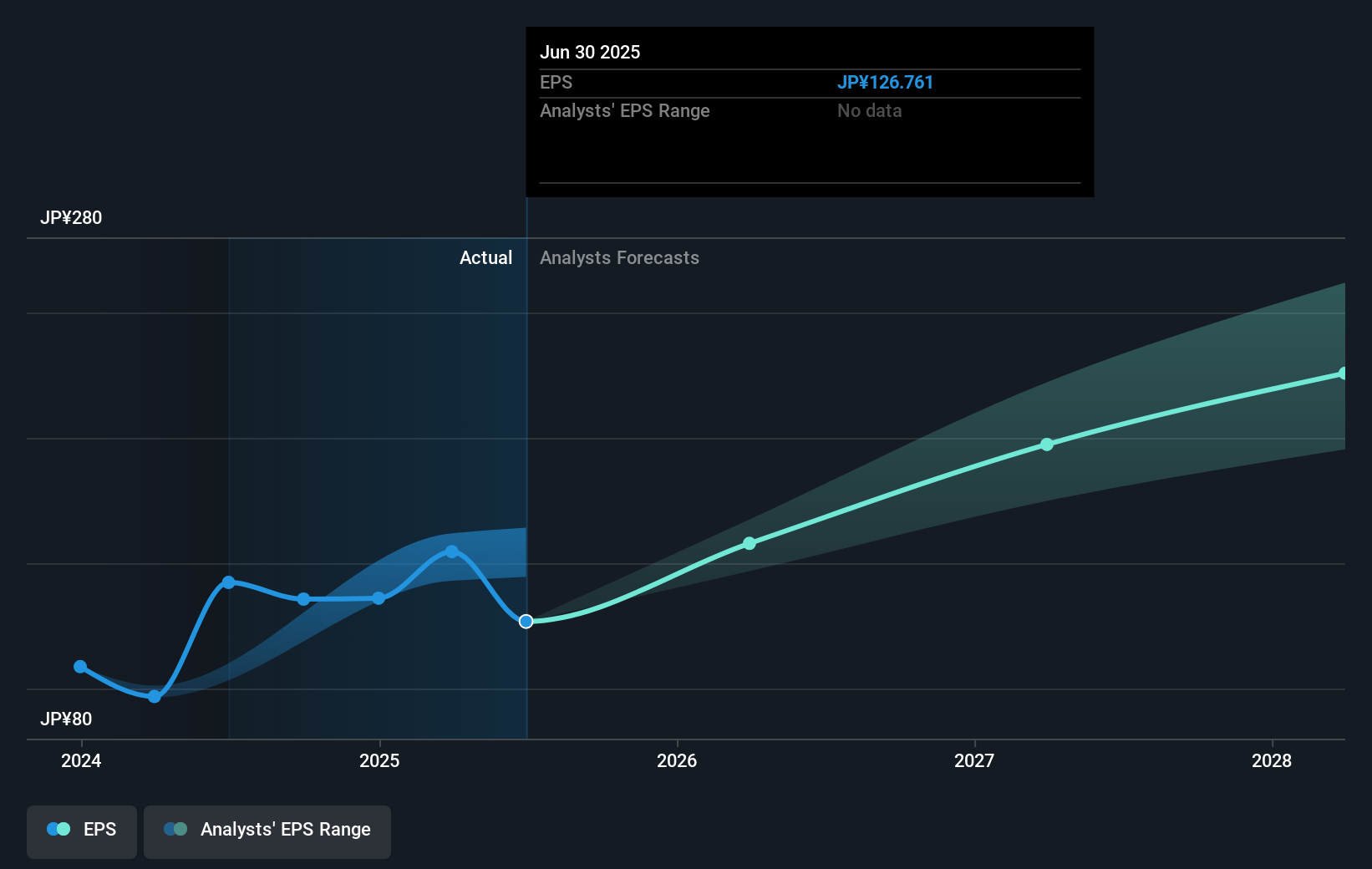

- The bearish analysts expect earnings to reach ¥49.2 billion (and earnings per share of ¥216.63) by about July 2028, up from ¥36.0 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 16.4x on those 2028 earnings, down from 21.6x today. This future PE is greater than the current PE for the JP Semiconductor industry at 16.0x.

- Analysts expect the number of shares outstanding to decline by 1.03% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.71%, as per the Simply Wall St company report.

Kokusai Electric Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Kokusai Electric continues to report strong revenue and profit growth due to increased demand for advanced semiconductor equipment, especially with the acceleration in NAND and DRAM technology investment, making future declines in earnings less likely.

- The company has increased its market share in key high-growth areas such as batch ALD equipment, surpassing 70% share in the batch ALD market and gaining new positions of record (PORs) with major manufacturers, supporting above-market revenue growth and profit margin expansion.

- Ongoing and accelerating investments in R&D and capacity expansion-including a new demonstration center in the U.S. and increased R&D spend to over 6% of revenues-position Kokusai to capture future technology shifts and maintain technological leadership, which is supportive for long-term earnings and margins.

- Strong secular trends, such as the ongoing proliferation of next-generation NAND (200-plus layer) and GAA (Gate-All-Around) technology nodes, as well as continued investment in global and regional semiconductor manufacturing, underpin robust multi-year capital equipment demand, which supports stable or rising long-term revenues.

- The company's strategy of diversifying its customer base across regions like Taiwan, South Korea, and the U.S., along with resilience to direct tariff impacts and export restrictions, reduces revenue volatility and supports sustained earnings growth even as global supply chains face challenges.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Kokusai Electric is ¥2800.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Kokusai Electric's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥4500.0, and the most bearish reporting a price target of just ¥2800.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be ¥297.2 billion, earnings will come to ¥49.2 billion, and it would be trading on a PE ratio of 16.4x, assuming you use a discount rate of 8.7%.

- Given the current share price of ¥3335.0, the bearish analyst price target of ¥2800.0 is 19.1% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.