Narratives are currently in beta

Key Takeaways

- Strategic R&D investments in antibody-drug conjugates and collaborations indicate potential future revenue growth and enhanced market share in oncology.

- Collaboration with U.S. Merck may lead to shared costs, milestone payments, and expanded market opportunities, boosting net earnings and profitability.

- Delays in product launches, insurance reimbursement, and reliance on exchange rates and partnerships may pressure Daiichi Sankyo's earnings and market penetration.

Catalysts

About Daiichi Sankyo Company- Manufactures and sells pharmaceutical products in Japan, North America, Europe, and internationally.

- Daiichi Sankyo's significant R&D investments and advancements, particularly in the field of antibody-drug conjugates (ADCs) like ENHERTU and 5DXd-ADCs, indicate potential strong future revenue growth through new drug approvals and expanded indications. This is likely to enhance long-term revenue prospects and improve net earnings.

- The strategic collaboration with U.S. Merck for co-development and commercialization of ADCs such as HER3-DXd suggests potential milestone payments and shared commercialization costs, which can positively impact net margins and contribute to an increase in net earnings through synergies and expanded market opportunities.

- Enhertu's strong sales performance and market leadership in multiple regions and cancer indications, with ongoing regulatory approvals and market expansion efforts, underline a potential increase in revenue growth, particularly from oncology products. This may lead to improved market share and profitability.

- The recent inclusion of MK-6070 into the strategic collaboration with U.S. Merck and the continuation of its development highlights potential future revenue from combination therapy markets, complementing existing products and potentially enhancing overall margins due to increased pharmacological capabilities.

- The possibility of expanded indications, new drug launches, and ongoing market penetration of high-potential treatments, such as for breast cancer and lung cancer, presents an opportunity for sustained revenue growth, improved profit margins, and net earnings. This is supported by ongoing clinical trials and anticipated regulatory decisions on their ADC pipeline.

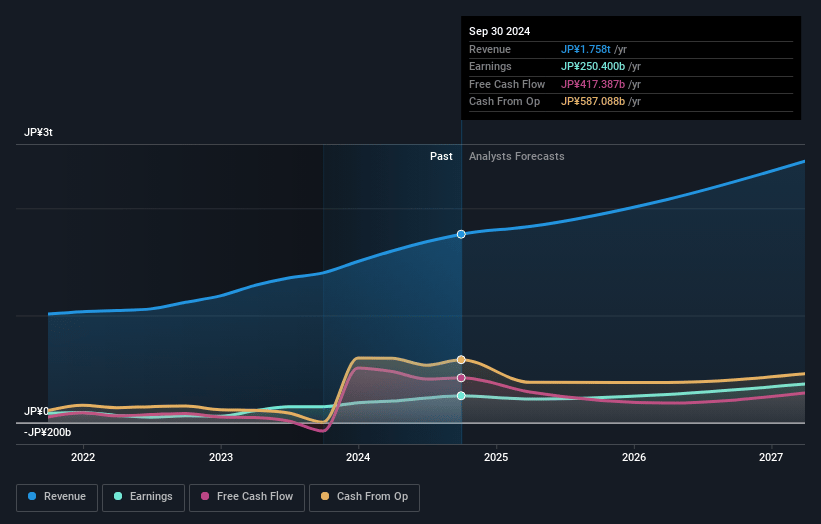

Daiichi Sankyo Company Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Daiichi Sankyo Company's revenue will grow by 13.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 14.2% today to 15.9% in 3 years time.

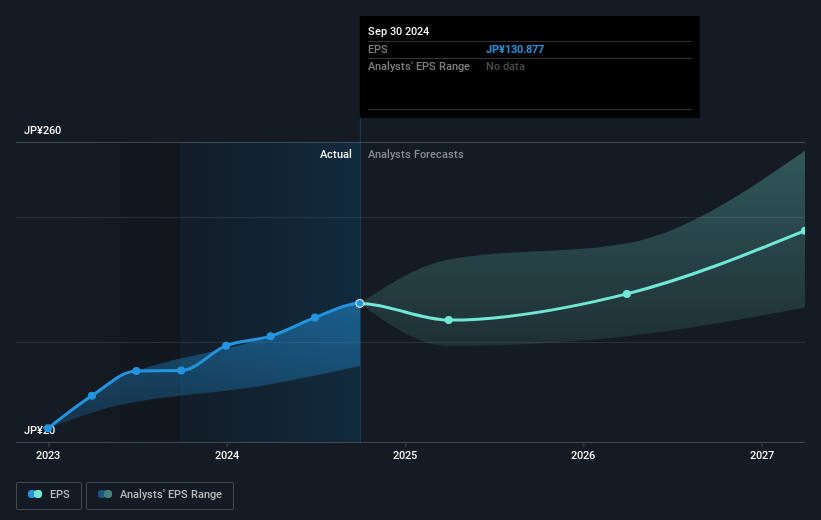

- Analysts expect earnings to reach ¥408.4 billion (and earnings per share of ¥216.14) by about January 2028, up from ¥250.4 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ¥477.0 billion in earnings, and the most bearish expecting ¥244.9 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 33.2x on those 2028 earnings, up from 32.7x today. This future PE is greater than the current PE for the JP Pharmaceuticals industry at 16.5x.

- Analysts expect the number of shares outstanding to grow by 0.1% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 4.29%, as per the Simply Wall St company report.

Daiichi Sankyo Company Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The delay in the launch of HER3-DXd in the U.S. and challenges related to its regulatory approval could impact future revenues by postponing potential sales and market penetration associated with this product.

- Delays in securing insurance reimbursement for Enhertu in countries like Spain and the U.K. introduce uncertainty in revenue projections and may affect the company's ability to capture market share effectively in Europe.

- High R&D expenses and increased costs related to expanding personnel for further development are likely to pressure margins and limit earnings if not offset by corresponding increases in successful product launches and sales.

- Daiichi Sankyo's dependence on favorable foreign exchange impacts to offset costs and boost revenue introduces financial risk, as currency fluctuations can unpredictably affect both top-line and net income figures.

- The reliance on a strategic partnership with U.S. Merck, and uncertainty around collaborative and licensing agreements, could lead to potential profit-sharing challenges that impact net margins and earnings if market conditions shift or if agreements need renegotiation.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ¥6333.33 for Daiichi Sankyo Company based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥7600.0, and the most bearish reporting a price target of just ¥5500.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ¥2568.2 billion, earnings will come to ¥408.4 billion, and it would be trading on a PE ratio of 33.2x, assuming you use a discount rate of 4.3%.

- Given the current share price of ¥4352.0, the analyst's price target of ¥6333.33 is 31.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives