Key Takeaways

- Heavy reliance on petroleum faces mounting threats from decarbonization policies, electric vehicle adoption, and regulatory pressures, jeopardizing stable long-term revenue streams.

- Weak diversification into renewables and demographic headwinds in Japan amplify the risk that legacy business profitability will erode faster than new growth can compensate.

- Strong performance in core energy and growing advanced materials, combined with diversification and capital discipline, could support future earnings resilience and shareholder value.

Catalysts

About ENEOS Holdings- Through its subsidiaries, operates in the energy, oil and natural gas exploration and production, and metals businesses in Japan, China, Asia, and internationally.

- ENEOS's core petroleum business is increasingly vulnerable to accelerating global decarbonization initiatives and policy shifts that threaten to structurally reduce long-term demand for gasoline and diesel, which is likely to produce sustained revenue declines even as the company pursues gradual low-carbon transitions.

- The rising adoption and affordability of electric vehicles and stricter fuel economy standards are expected to lead to a permanent drop in downstream fuel sales, resulting in compressing net margins and a shrinking earnings base for the overall group.

- Overexposure to a declining Japanese market with worsening demographics, combined with only incremental progress on renewable energy diversification, signals heightened risk that legacy asset returns will deteriorate faster than new business lines generate profits, endangering long-term earnings growth and free cash flow.

- Persistent regulatory pressures from tighter emissions caps, carbon pricing, and quality mandates will force significantly higher compliance expenditures and operating costs, eroding profit margins even in years of stable crude prices.

- Potentially rising decommissioning and environmental remediation liabilities from the company's aging oil refining and upstream assets will divert capital away from growth and shareholder returns, weighing on long-term return on equity and debt service capacity.

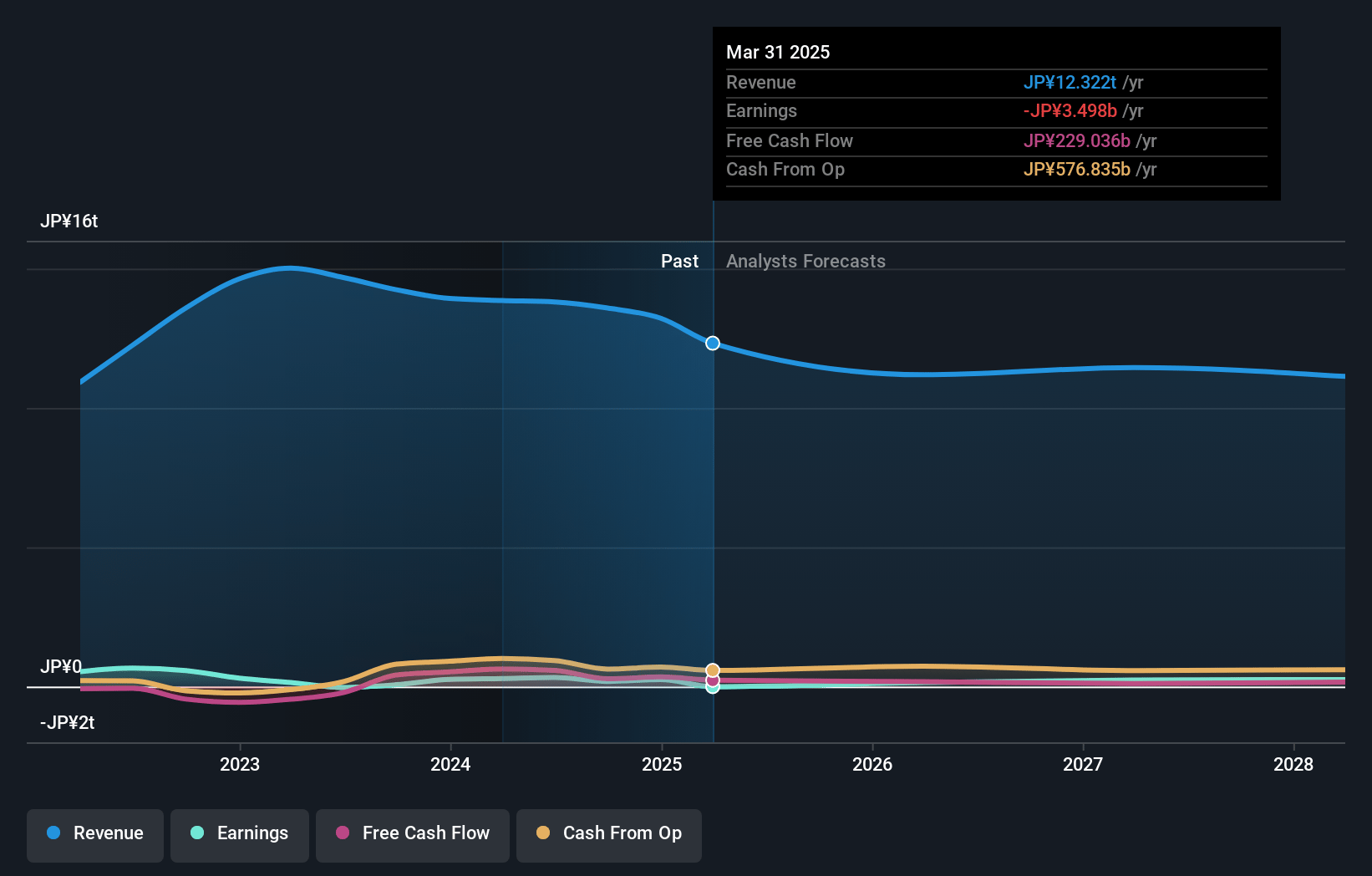

ENEOS Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on ENEOS Holdings compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming ENEOS Holdings's revenue will decrease by 10.5% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from -0.0% today to 2.6% in 3 years time.

- The bearish analysts expect earnings to reach ¥232.2 billion (and earnings per share of ¥89.56) by about June 2028, up from ¥-3.5 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 8.5x on those 2028 earnings, up from -558.6x today. This future PE is lower than the current PE for the JP Oil and Gas industry at 10.0x.

- Analysts expect the number of shares outstanding to decline by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.63%, as per the Simply Wall St company report.

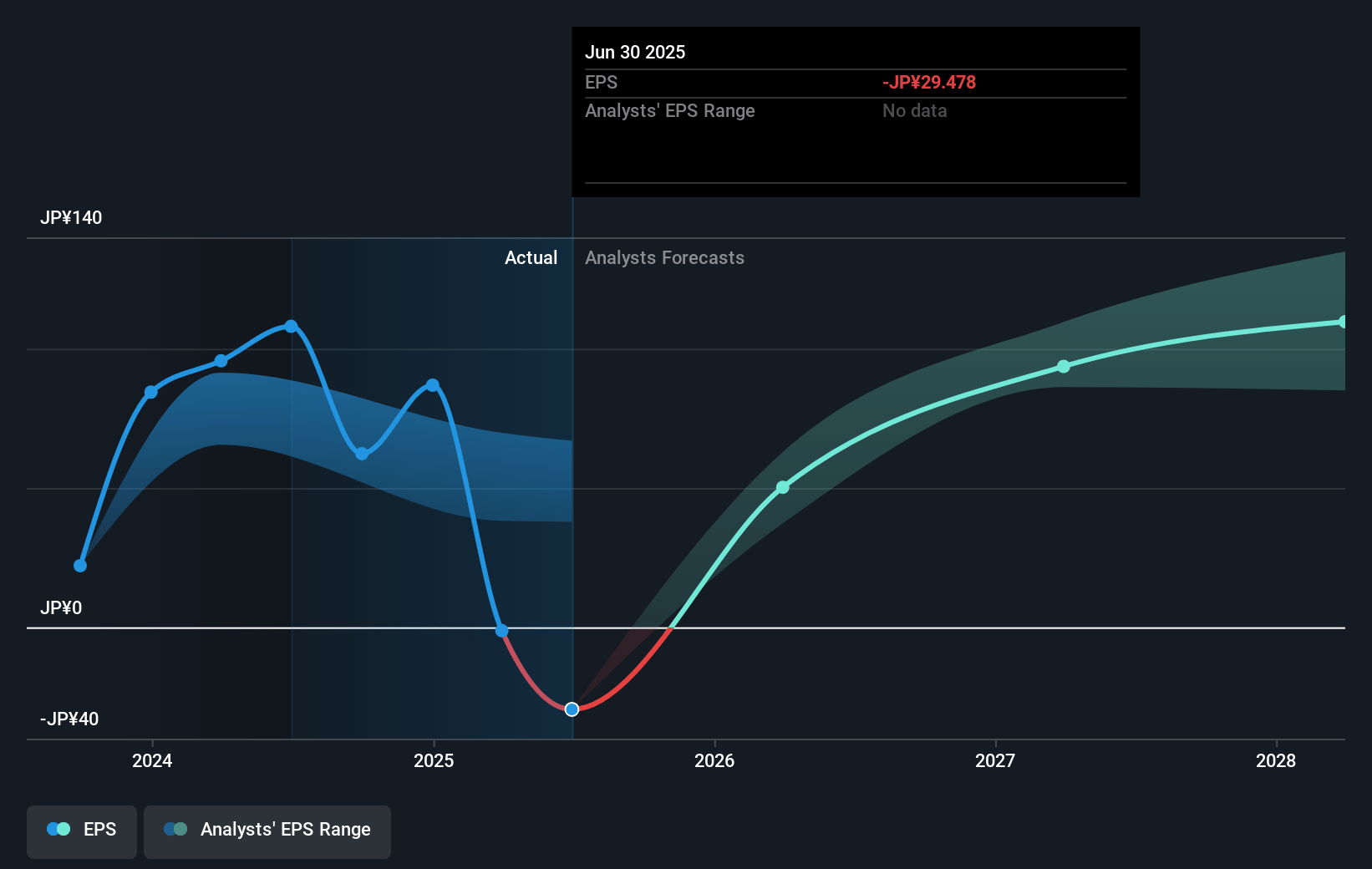

ENEOS Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Continued firm petroleum product margins and improved export margins, despite oil price declines, have supported operating profit and indicate that resilient downstream performance could sustain earnings and defend profit margins over the long term.

- Expansion and profit growth in the high-performance materials and metals businesses, including increased sales of semiconductor and thin-film materials driven by structural demand for data centers and electronics, point to new revenue streams that may offset declining traditional fuel revenues.

- Steady progress in renewable energy and low-carbon LNG projects, as well as operational improvements like lower unplanned capacity loss at refineries, demonstrate successful diversification and capital efficiency which could bolster both long-term revenue and net margins.

- The listing of JX Advanced Metals Corporation unlocks value by allowing ENEOS to rapidly execute strategic investments and business portfolio reforms, while also enabling shareholder returns and reducing capital intensity, supporting higher return on equity and potential earnings growth.

- Robust balance sheet management including strategic asset sales, share buybacks, and disciplined capital expenditure suggest strong governance and potential for sustained free cash flow generation, which can underpin long-term shareholder value and support share price resilience.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for ENEOS Holdings is ¥750.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of ENEOS Holdings's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥1100.0, and the most bearish reporting a price target of just ¥750.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be ¥8824.6 billion, earnings will come to ¥232.2 billion, and it would be trading on a PE ratio of 8.5x, assuming you use a discount rate of 6.6%.

- Given the current share price of ¥726.3, the bearish analyst price target of ¥750.0 is 3.2% higher. The relatively low difference between the current share price and the analyst bearish price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.