Key Takeaways

- Capital recycling and strategic divestments in high-growth sectors aim to boost profitability, ROA, and ROE, contributing to sustainable earnings growth.

- Asset management shift leveraging third-party capital enhances revenue streams, while share buybacks and dividend commitments increase shareholder returns and EPS growth.

- Prolonged higher interest rates and geopolitical risks impact ORIX's profitability, asset growth, and ability to meet profit targets amid rising costs and divestment challenges.

Catalysts

About ORIX- Provides diversified financial services in Japan, the United States, Asia, Europe, Australasia, and the Middle East.

- ORIX is focused on capital recycling, particularly within its Investment category, which is expected to improve profitability and push up ROA and ROE by efficiently reallocating capital towards high-growth opportunities such as domestic PE, real estate, and overseas renewable energy. This could enhance earnings growth.

- The company has emphasized its shift towards an asset management model, leveraging third-party capital for scaling operations, which could increase revenue streams and enhance net margins through fee-based income and potentially higher operating leverage.

- ORIX's divestment strategy, including the anticipated sale of its stake in Greenko and reinvestment in AM Green within the renewable energy sector, is positioned to create significant capital gains and contribute to a sustainable business model focused on clean energy, potentially boosting net income and driving long-term growth.

- Shareholder returns remain a priority, with completed share repurchases of ¥50 billion and a commitment to maintain an attractive dividend policy. These buybacks are anticipated to support EPS growth by reducing share count and effectively utilizing excess cash.

- ORIX's strategy to enhance profitability in the U.S. market involves improving origination volumes and focusing on higher profitability deals in real estate and private credit, which could stabilize and eventually grow earnings in the segment amid a recovering economic environment.

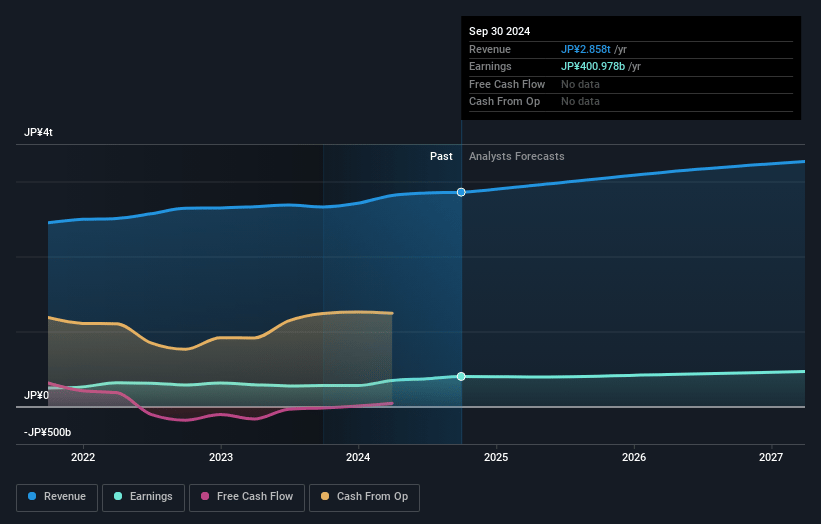

ORIX Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming ORIX's revenue will grow by 4.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 13.6% today to 14.0% in 3 years time.

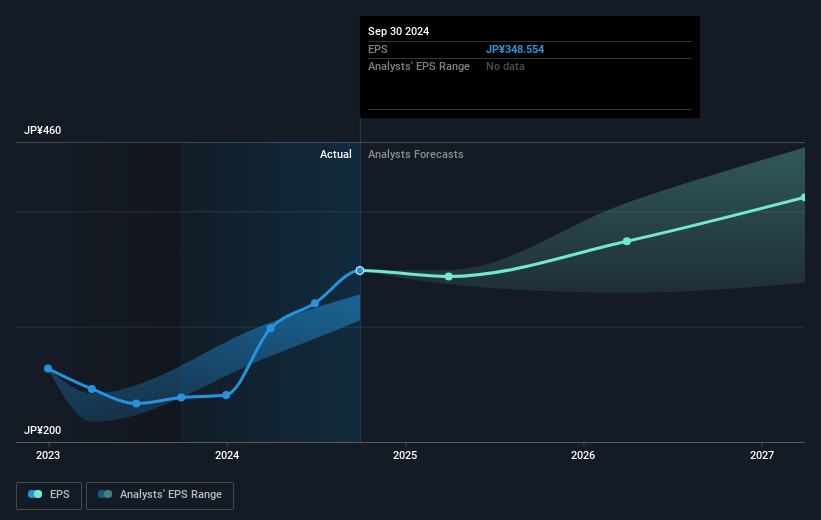

- Analysts expect earnings to reach ¥468.2 billion (and earnings per share of ¥425.19) by about April 2028, up from ¥398.7 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as ¥390.0 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.2x on those 2028 earnings, up from 7.8x today. This future PE is greater than the current PE for the US Diversified Financial industry at 11.6x.

- Analysts expect the number of shares outstanding to decline by 1.33% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.94%, as per the Simply Wall St company report.

ORIX Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The credit segment in ORIX USA has seen a decrease in profit, partially due to prolonged higher interest rates and lower contributions from ORIX Credit, impacting overall profitability (net margins).

- The Asia and Australia segment profits decreased, with business confidence remaining weak in Greater China and increasing credit costs cited as reasons, potentially affecting revenue and asset growth in the region.

- Financial market uncertainties, such as rising interest rates and geopolitical risks, could impact ORIX's investment returns and capital recycling efforts, affecting earnings.

- Higher construction costs and other macroeconomic factors may slow down the profitability growth of new development projects, potentially impacting future revenues and margins.

- Delays or failures in planned divestments, like the Greenko sale, might affect the company's ability to achieve its full-year profit targets, impacting net income expectations.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ¥3952.222 for ORIX based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥4450.0, and the most bearish reporting a price target of just ¥3400.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ¥3333.7 billion, earnings will come to ¥468.2 billion, and it would be trading on a PE ratio of 12.2x, assuming you use a discount rate of 9.9%.

- Given the current share price of ¥2733.0, the analyst price target of ¥3952.22 is 30.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.