Key Takeaways

- Demographic decline and slow digital transformation are weakening Aeon's domestic sales growth and exposing it to structural underperformance.

- Rising competition, costs, and stringent regulations are pressuring margins, profitability, and reinvestment capacity.

- Strategic private label expansion, digital transformation, and ASEAN market growth are strengthening Aeon's margins, earnings potential, and competitive position against domestic and global headwinds.

Catalysts

About Aeon- Operates in the retail industry in Japan, China, ASEAN countries, and internationally.

- Ongoing demographic decline in Japan will gradually erode Aeon's domestic customer base, leading to structurally weaker same-store sales and stagnating revenue over the long term, with the growth from urbanization unlikely to compensate for headwinds from a shrinking and aging population.

- As the consumer shift towards e-commerce and digital-first shopping accelerates, Aeon's heavy exposure to traditional hypermarket and mall formats exposes the company to ongoing traffic declines and margin pressure, since store conversion and digital transformation have lagged leading online-focused competitors, risking structural underperformance in both revenue and net profit.

- Intensifying competition from discount retailers, convenience chains, and large e-commerce platforms will fuel price wars and the loss of market share, directly compressing Aeon's gross margins and eroding profitability, while ongoing investments in private brands alone may not be sufficient to restore pricing power or customer loyalty.

- Persistent inflation, rising energy costs, and labor shortages in Japan threaten to offset recent productivity improvements, with wage and utility expenses becoming a chronic burden on Aeon's already-thin operating margins and constraining the company's ability to reinvest for future growth or defend earnings.

- Escalating environmental regulations and growing ESG compliance demands will force Aeon to funnel substantial capital into supply chain upgrades, risk management, and reporting infrastructure, which will inflate capital expenditures and further pressure both free cash flow and returns on invested capital over the medium to long term.

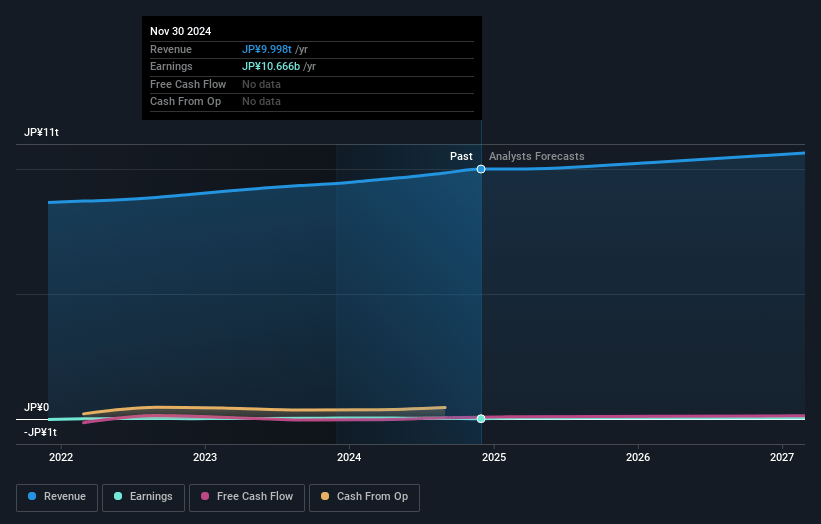

Aeon Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Aeon compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Aeon's revenue will grow by 1.7% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 0.3% today to 0.5% in 3 years time.

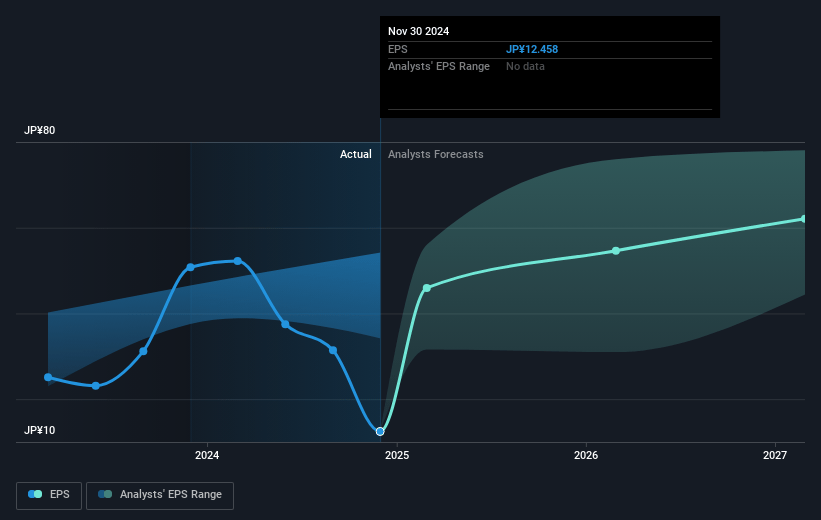

- The bearish analysts expect earnings to reach ¥49.4 billion (and earnings per share of ¥57.43) by about July 2028, up from ¥28.8 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 50.7x on those 2028 earnings, down from 141.6x today. This future PE is greater than the current PE for the JP Consumer Retailing industry at 13.1x.

- Analysts expect the number of shares outstanding to grow by 0.53% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.25%, as per the Simply Wall St company report.

Aeon Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Aeon's multi-year focus on expanding private brand offerings (such as Topvalu) and vertically integrating supply chains is driving consistent margin improvement and revenue resilience, with private brand sales showing robust annual growth and targets set for further expansion, which could support higher revenues and net margins over time.

- The company is demonstrating successful digital transformation and omnichannel strategies-like integrating customer and product IDs, scaling e-commerce, and leveraging digital payment platforms-poised to capitalize on secular growth in online retail and improve operational efficiencies, which could expand margins and support earnings growth.

- Ongoing scale-driven cost optimization across the group, such as group-wide procurement, labor productivity improvements, and store digitalization, suggests Aeon can structurally improve gross and net margins, even in the face of inflation and higher input costs.

- Strong growth and commitment to further expansion in high-potential ASEAN markets, especially Vietnam, position the company to tap into favorable demographic trends and rising middle-class consumption, creating a structural opportunity for long-term revenue and earnings growth that offsets domestic market headwinds.

- Industry consolidation trends and Aeon's ability to implement horizontal integration across group companies (including recent M&A and business model reform) are enhancing its competitive position, allowing for better economies of scale and potentially driving improved profitability and market share, directly benefiting top-line growth and long-term shareholder value.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Aeon is ¥2389.49, which represents two standard deviations below the consensus price target of ¥4121.44. This valuation is based on what can be assumed as the expectations of Aeon's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥4950.05, and the most bearish reporting a price target of just ¥2200.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be ¥10667.4 billion, earnings will come to ¥49.4 billion, and it would be trading on a PE ratio of 50.7x, assuming you use a discount rate of 6.2%.

- Given the current share price of ¥4734.0, the bearish analyst price target of ¥2389.49 is 98.1% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives