Key Takeaways

- Expansion in energy storage and generative AI products is driving significant revenue growth and improved margins due to increased demand and pricing power.

- Strategic productivity improvements and market share growth in key sectors may enhance operating efficiency, boosting net margins and earnings.

- Panasonic faces revenue and profit challenges due to decreased automotive sales, energy demand declines, exchange rate fluctuation, and increased costs from new facility investments.

Catalysts

About Panasonic Holdings- Research, develops, manufactures, sells, and services various electrical and electronic products worldwide.

- Panasonic's energy storage systems for data centers are experiencing significant growth, driven by generative AI advancements, with full-year sales expected to reach ¥100 billion, representing a 1.8x year-on-year increase. This expansion could enhance revenue and earnings due to high demand and better product margins.

- The expansion of generative AI-related products in the Industry segment, including conductive polymer capacitors and multilayer circuit board materials, is rapidly increasing, with annual sales expected to reach ¥35 billion, 1.8 times higher year-on-year. This could contribute to higher revenue and improved margins given the high demand and pricing power.

- Panasonic's strategic focus on improving productivity at its North American factories and ramping up production at its new facilities in Kansas and Wakayama to meet EV battery demand may enhance operating efficiency, potentially leading to better net margins and increased earnings in the long term.

- The company's plans to ensure no business fails to meet the Weighted Average Cost of Capital (WACC) by the end of FY '27 indicate a proactive approach to increasing return on investments, which could lead to higher net margins and earnings growth by improving capital efficiency.

- Panasonic is experiencing market share growth in the domestic consumer electronics sector, with strong sales in categories like washing machines and personal care appliances. This could lead to higher revenue and profitability in the Lifestyle segment by leveraging strong brand recognition and market positioning.

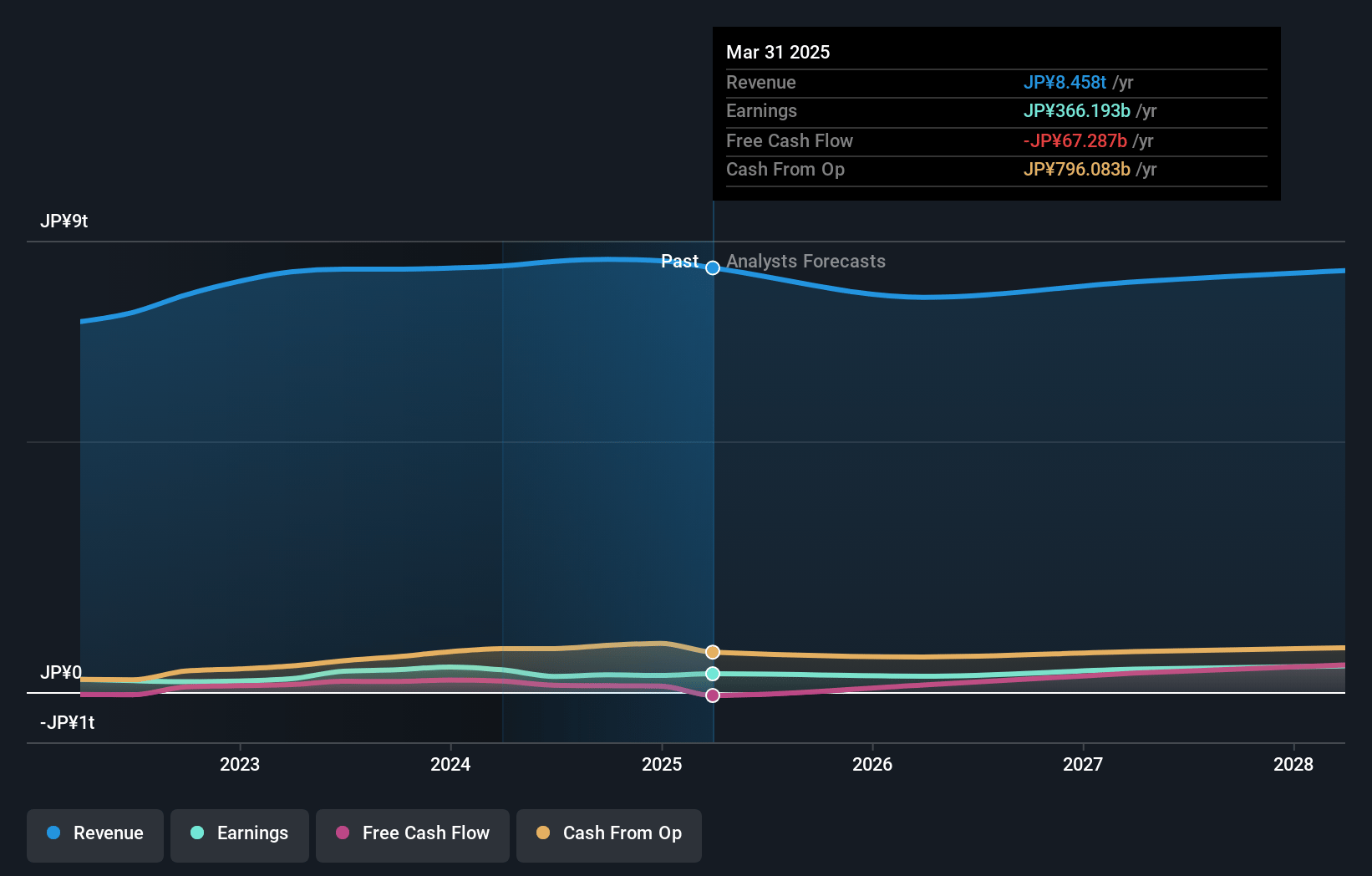

Panasonic Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Panasonic Holdings's revenue will decrease by -1.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.0% today to 5.5% in 3 years time.

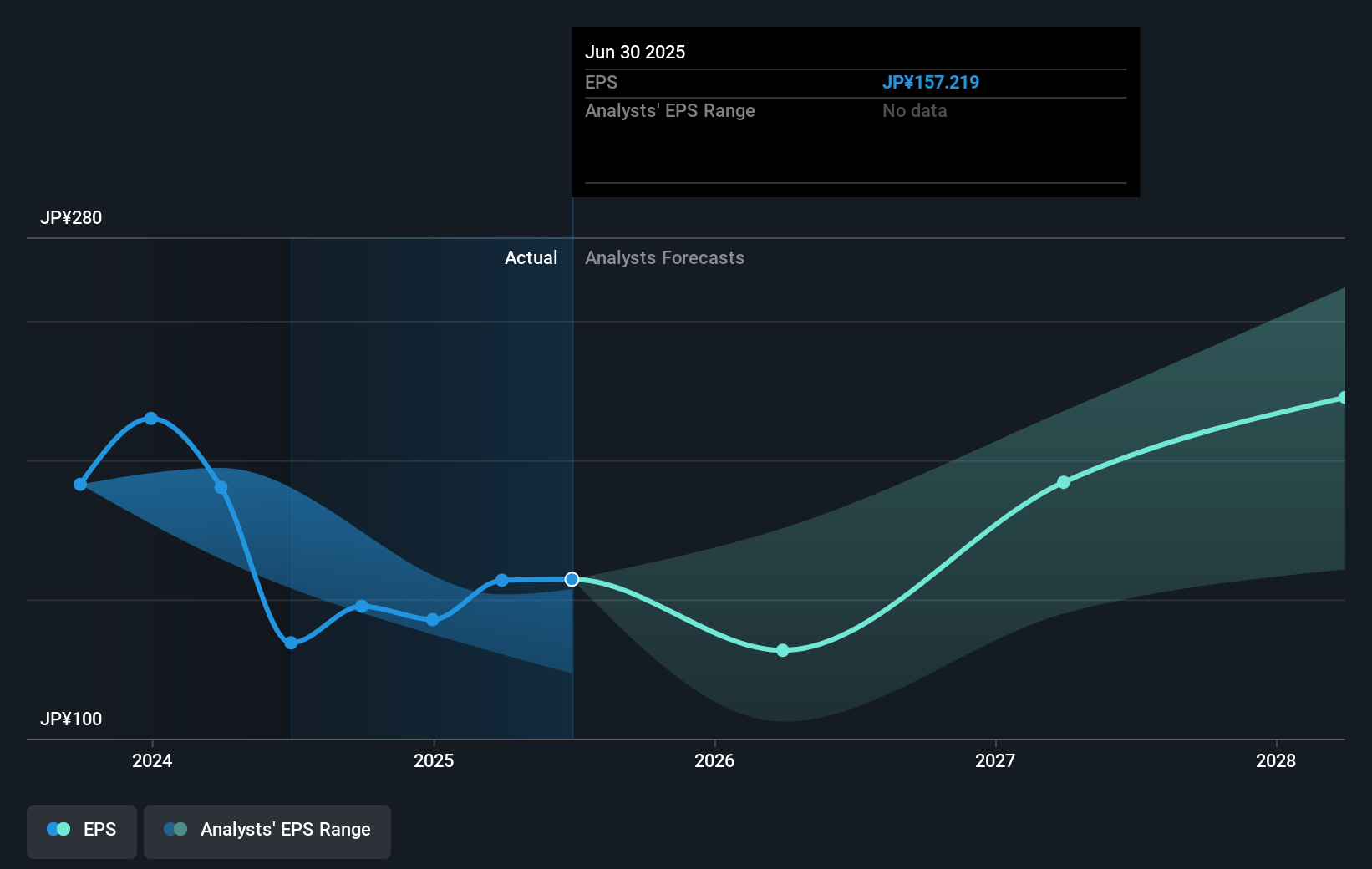

- Analysts expect earnings to reach ¥449.0 billion (and earnings per share of ¥199.67) by about January 2028, up from ¥344.5 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ¥525.0 billion in earnings, and the most bearish expecting ¥389.9 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.0x on those 2028 earnings, up from 10.3x today. This future PE is lower than the current PE for the JP Consumer Durables industry at 11.9x.

- Analysts expect the number of shares outstanding to decline by 1.24% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.84%, as per the Simply Wall St company report.

Panasonic Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Decreased sales in the Automotive sector due to discontinuation of production for certain models and sluggish sales mainly in China could negatively impact revenue growth.

- The Energy segment faces risks from a year-on-year decrease in demand for automotive batteries and price revisions reflecting lower raw material costs, which may affect future earnings.

- The Lifestyle division is experiencing lower sales in consumer electronics in China and reduced sales of air-to-water systems in Europe, potentially impacting net margins and revenue stability.

- Exchange rate fluctuations, particularly the yen's depreciation, create uncertainty and could adversely influence Panasonic's international earnings.

- Investments in new energy and automotive facilities, such as in the Kansas and Wakayama plants, could lead to increased fixed and ramp-up costs, affecting profit margins and free cash flow.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ¥1749.0 for Panasonic Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥2300.0, and the most bearish reporting a price target of just ¥1340.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ¥8230.4 billion, earnings will come to ¥449.0 billion, and it would be trading on a PE ratio of 11.0x, assuming you use a discount rate of 7.8%.

- Given the current share price of ¥1523.0, the analyst's price target of ¥1749.0 is 12.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives