Key Takeaways

- Reliance on shrinking oil and gas markets and exposure to complex, high-risk contracts threaten margin stability and long-term growth.

- Rising competition, client bargaining power, and ESG pressures are likely to erode profitability and limit future capital access.

- Improved operational performance, reduced risk exposure, strong liquidity, and a robust project pipeline position Saipem for more stable earnings and long-term growth.

Catalysts

About Saipem- Provides energy and infrastructure solutions worldwide.

- The accelerating global shift toward renewable energy is expected to drive a sustained reduction in oil and gas project investments, shrinking Saipem's addressable market and making the company increasingly reliant on winning a smaller pool of large-scale projects. This will likely put downward pressure on revenues and long-term backlog growth.

- Saipem's continued heavy exposure to technically complex and costly oil and gas contracts increases the risk of future cost overruns, project delays, and contract disputes, potentially eroding net margins and generating volatility in future earnings, especially as new, lower-margin projects enter the portfolio.

- Industry consolidation among oil majors is increasing the bargaining power of Saipem's clients, leading to more competitive bidding, lower contract values, and margin compression, which threatens the sustainability of recent EBITDA margin improvements.

- Intensifying competition from lower-cost Asian EPC contractors is expected to squeeze Saipem's pricing power over time, resulting in lower realized margins on new contract awards and hampering the company's ability to defend its currently improved profitability.

- The proliferation of ESG-driven capital allocation and heightened regulatory scrutiny on decarbonization will increase Saipem's compliance costs, restrict funding access, and further depress valuation multiples, all of which pose long-term headwinds to earnings growth and capital returns.

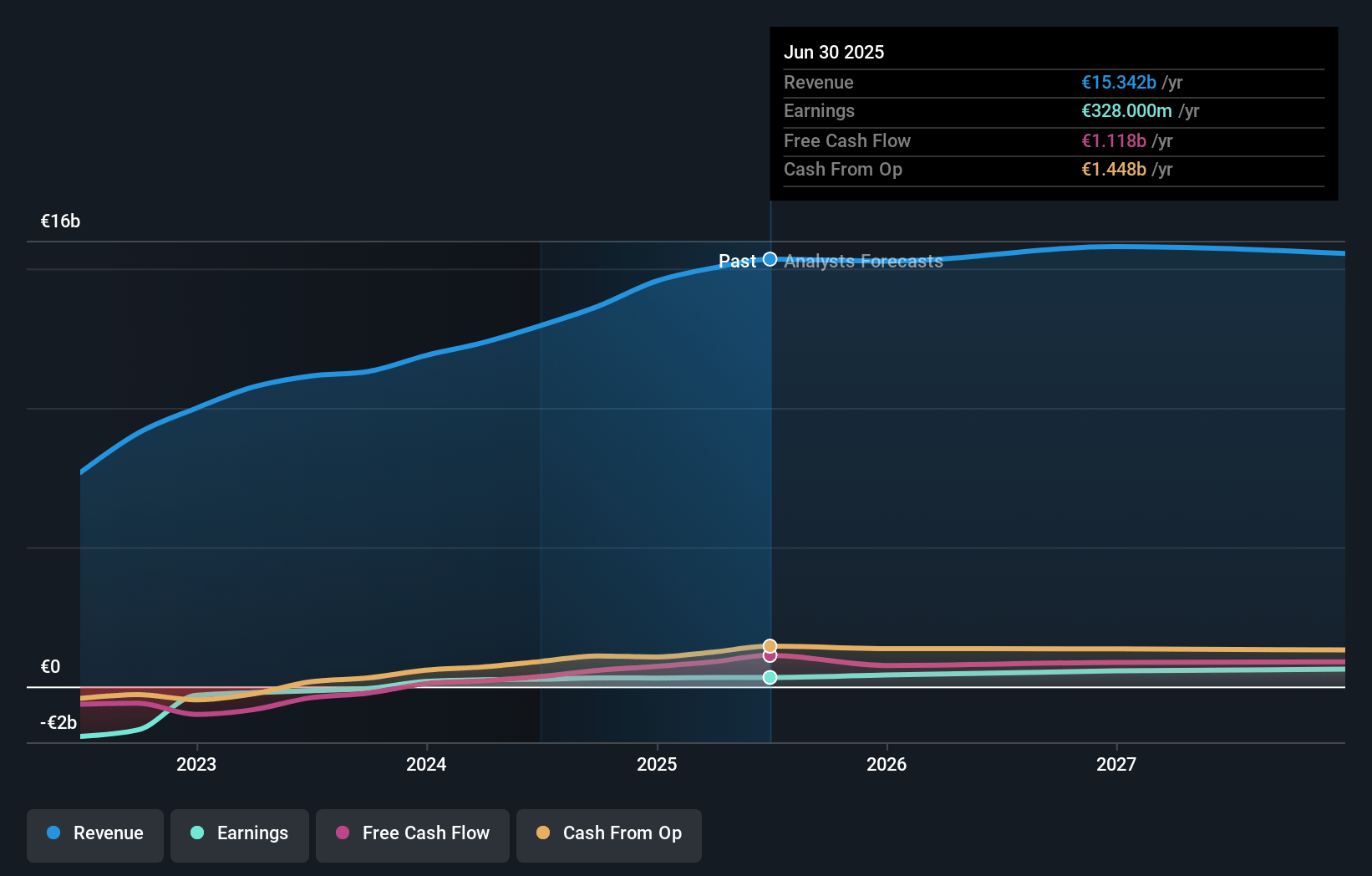

Saipem Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Saipem compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Saipem's revenue will decrease by 0.6% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 2.2% today to 3.8% in 3 years time.

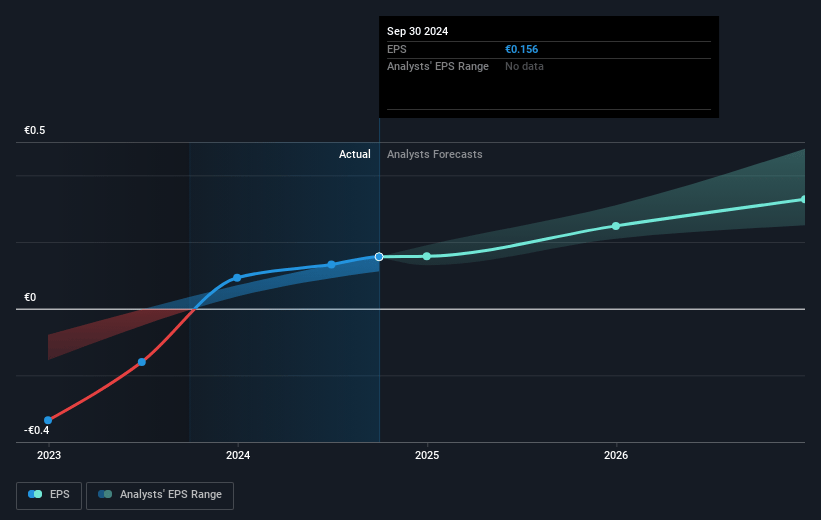

- The bearish analysts expect earnings to reach €564.2 million (and earnings per share of €0.28) by about June 2028, up from €326.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 9.8x on those 2028 earnings, down from 13.8x today. This future PE is lower than the current PE for the GB Energy Services industry at 12.7x.

- Analysts expect the number of shares outstanding to decline by 0.78% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.06%, as per the Simply Wall St company report.

Saipem Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Saipem's record high backlog, which now provides 90 percent coverage for 2025 and 70 percent for 2026, gives strong visibility on future revenue and reduces near-term top-line uncertainty, supporting stability in earnings and cash flow.

- The company has significantly improved operational performance over the past three years, nearly doubling revenue and tripling EBITDA, while EBITDA margin expanded by 440 basis points, suggesting a sustained trend of margin improvement that could support higher net margins.

- Strategic derisking in new contract awards, particularly in energy transition segments like CCUS and biorefineries, and the adoption of risk-sharing and reimbursable models, lowers historical exposure to cost overruns, which could translate to improved predictability and sustainability of earnings.

- Saipem's strong financial position, with over 1.6 billion euros in available cash and robust liquidity exceeding 3 billion euros, plus a clear priority to further reduce net debt, underpinned by recent credit rating upgrades, decreases refinancing risk and could lead to lower financial expenses and higher net profits.

- The global market environment remains favorable for offshore energy development, as evidenced by Saipem's fully booked construction fleet through 2026 and a stable, sizable commercial pipeline, which, combined with positive long-term secular trends such as the energy transition and infrastructure renewal, could drive sustained revenue growth and support long-term share price resilience.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Saipem is €2.18, which represents two standard deviations below the consensus price target of €3.06. This valuation is based on what can be assumed as the expectations of Saipem's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €3.54, and the most bearish reporting a price target of just €2.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be €14.7 billion, earnings will come to €564.2 million, and it would be trading on a PE ratio of 9.8x, assuming you use a discount rate of 10.1%.

- Given the current share price of €2.3, the bearish analyst price target of €2.18 is 5.6% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.