Key Takeaways

- The merger with Banca Popolare di Sondrio aims to enhance market presence and shareholder value, leveraging synergies for improved earnings and commission income.

- Technological upgrades and cost reductions are set to improve efficiency and financial performance, underscoring a focus on sustainable growth and profitability.

- The potential merger with Banca Popolare di Sondrio and conservative financial strategies pose risks to earnings growth, shareholder value, and revenue stability amidst economic uncertainties.

Catalysts

About BPER Banca- Provides banking products and services for individuals, and businesses and professionals in Italy and internationally.

- The proposed business combination with Banca Popolare di Sondrio is expected to create synergies and a stronger, more resilient group, enhancing BPER's market position and future earnings potential. This initiative is anticipated to impact earnings positively by yielding significant value through synergies conservatively estimated at €290 million by 2027.

- Through the business combination, BPER aims to achieve a larger market footprint, especially in the rich northern regions of Italy, and expects the transaction to be mid-single-digit accretive on EPS, including run-rate synergies, suggesting improved shareholder value and earnings.

- The integration with Banca Popolare di Sondrio is planned to enhance revenue synergies by aligning productivity and leveraging BPER's commercial best practices, potentially boosting revenue streams from the combined customer base and enhancing commission income.

- BPER's robust capital position, evidenced by a CET1 ratio of around 15.8%, and the expectation of a 75% dividend payout ratio, highlight a strategy focused on sustainable capital generation and shareholder returns, supporting future profitability.

- BPER’s ongoing initiatives in technological modernization and efficiency improvements, including the reduction of operating costs and branch optimization, are expected to decrease expenses and improve net margins, strengthening overall financial performance.

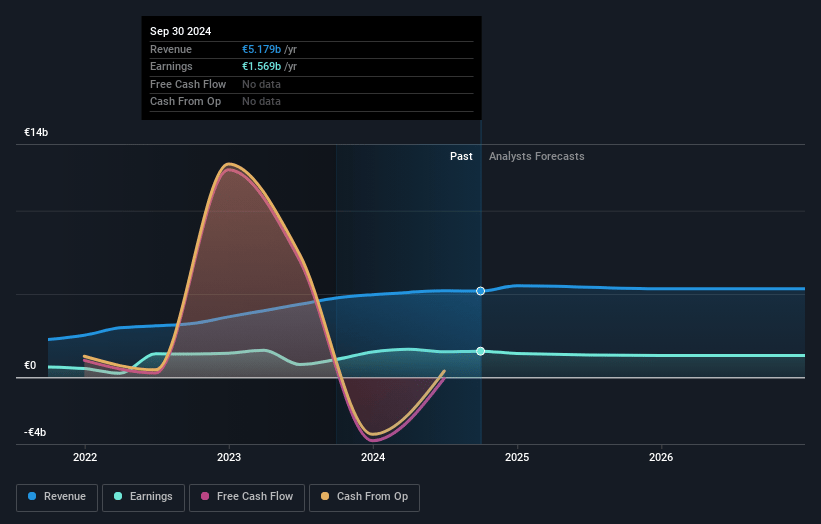

BPER Banca Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming BPER Banca's revenue will grow by 2.2% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 27.2% today to 26.0% in 3 years time.

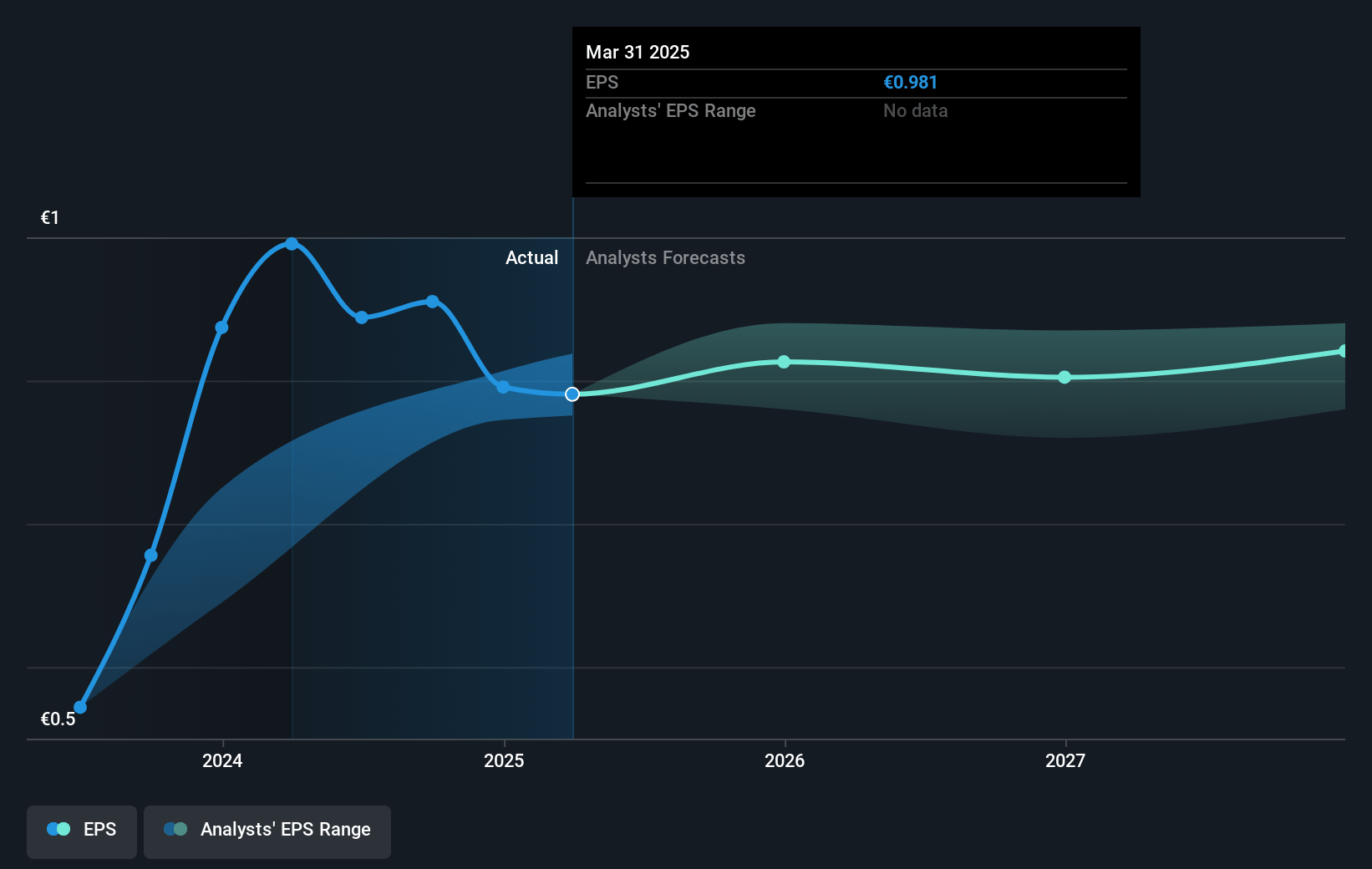

- Analysts expect earnings to remain at the same level they are now, that being €1.4 billion (with an earnings per share of €1.01). The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 10.4x on those 2028 earnings, up from 7.8x today. This future PE is greater than the current PE for the GB Banks industry at 8.5x.

- Analysts expect the number of shares outstanding to grow by 0.19% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.14%, as per the Simply Wall St company report.

BPER Banca Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The potential business combination with Banca Popolare di Sondrio introduces execution risks, such as integration challenges and unexpected costs, which could affect future net margins and overall earnings.

- The guidance for net interest income (NII) in 2025 is expected to be conservatively aligned with 2023, indicating limited growth potential in a changing interest rate environment, potentially impacting revenue and earnings growth.

- The transaction structure relies heavily on shares rather than cash, which might dilute existing shareholders and could result in EPS accretion concerns, affecting perceived earnings growth potential.

- Despite strong liquidity and a healthy CET1 ratio, there is a cautious approach to capital management and potential regulatory capital constraints, which might limit aggressive growth and shareholder returns, impacting future shareholder value creation.

- The focus on conservative approach and limited forward-looking guidance could indicate vulnerabilities to external economic conditions, such as fluctuations in interest rates and regional market dynamics, potentially affecting future revenue stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €7.61 for BPER Banca based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €9.5, and the most bearish reporting a price target of just €4.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €5.5 billion, earnings will come to €1.4 billion, and it would be trading on a PE ratio of 10.4x, assuming you use a discount rate of 11.1%.

- Given the current share price of €7.71, the analyst price target of €7.61 is 1.3% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.