Key Takeaways

- Robust expansion plans through major CapEx projects and partnerships may boost revenues by enhancing operational efficiency and exploring new funding avenues.

- Commitment to green energy projects and regulatory investments could enhance net margins and support sustained growth and capital expansion.

- Regulatory challenges, project execution delays, debt reliance, and delayed payments threaten Power Grid's profitability, liquidity, and earnings.

Catalysts

About Power Grid Corporation of India- An electric power transmission utility, engages in the transmission of power in India and internationally.

- Power Grid Corporation's increasing CapEx and project pipeline, including significant projects like the Khavda-Nagpur HVDC and Pang-Kaithal HVDC, indicate a robust expansion plan. This is expected to enhance future revenue through the commissioning of these high-value projects.

- The company's focus on dynamic line weighting and e-vegetation management for asset management optimization may lead to improved operational efficiencies. This has the potential to positively impact net margins by reducing operational costs and increasing asset reliability.

- Power Grid's securing of a USD 200 million green loan from Sumitomo Mitsui Banking Corporation highlights its commitment to renewable energy projects. This could contribute to revenue growth as the company aligns with India's green energy targets and explores new funding avenues.

- The partnership with the Electric Power Research Institute (EPRI) in the USA aims at enhancing transmission system construction and operation, which could lead to cost efficiencies and increase net margins through improved technology and reduced maintenance costs.

- Regulatory and policy-driven projects, like the ₹3.91 lakh crore interstate investment planned through 2032, provide a stable pipeline for Power Grid, potentially boosting earnings through increased regulated returns and capital base expansion.

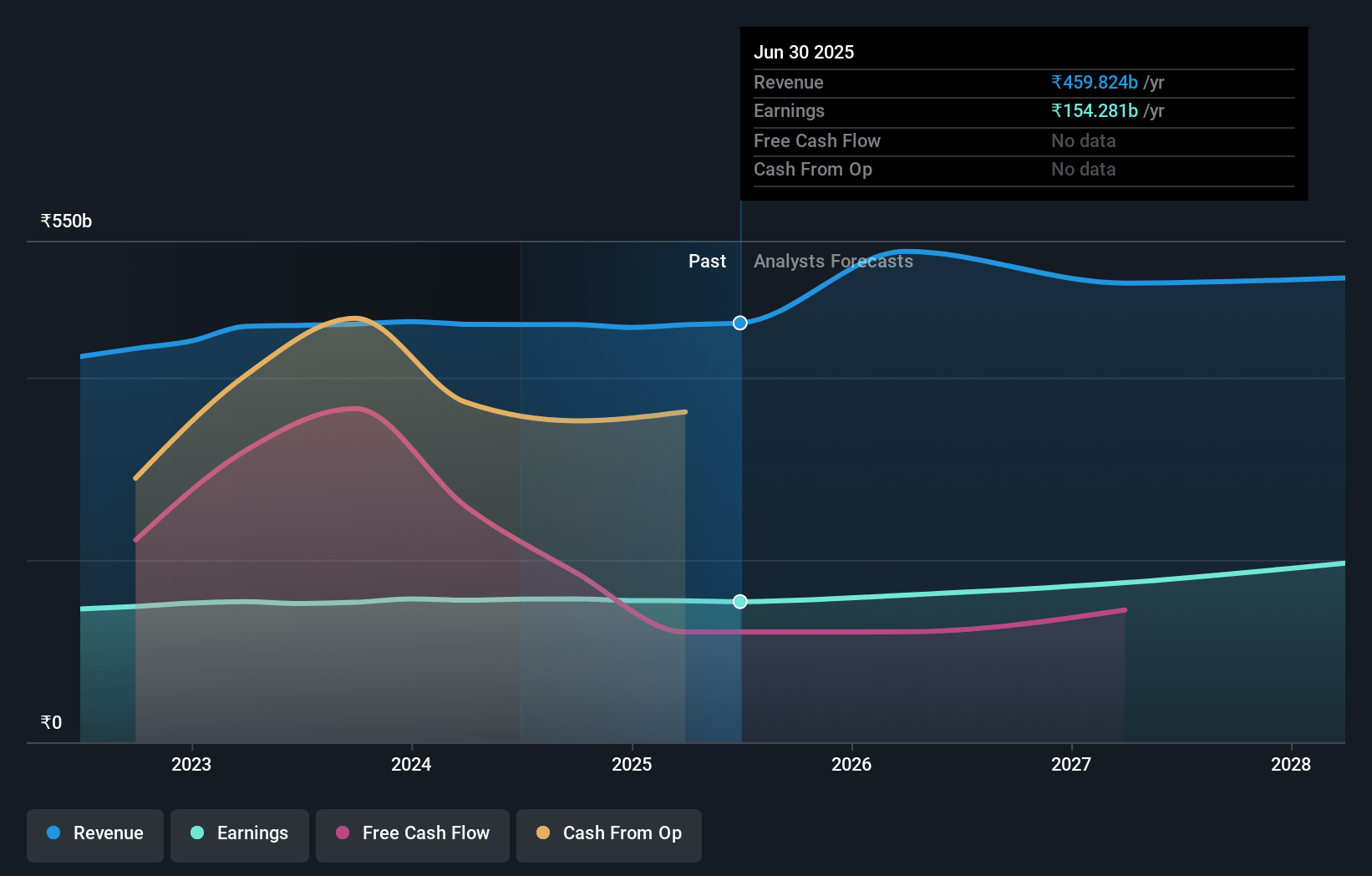

Power Grid Corporation of India Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Power Grid Corporation of India's revenue will grow by 5.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 34.2% today to 34.5% in 3 years time.

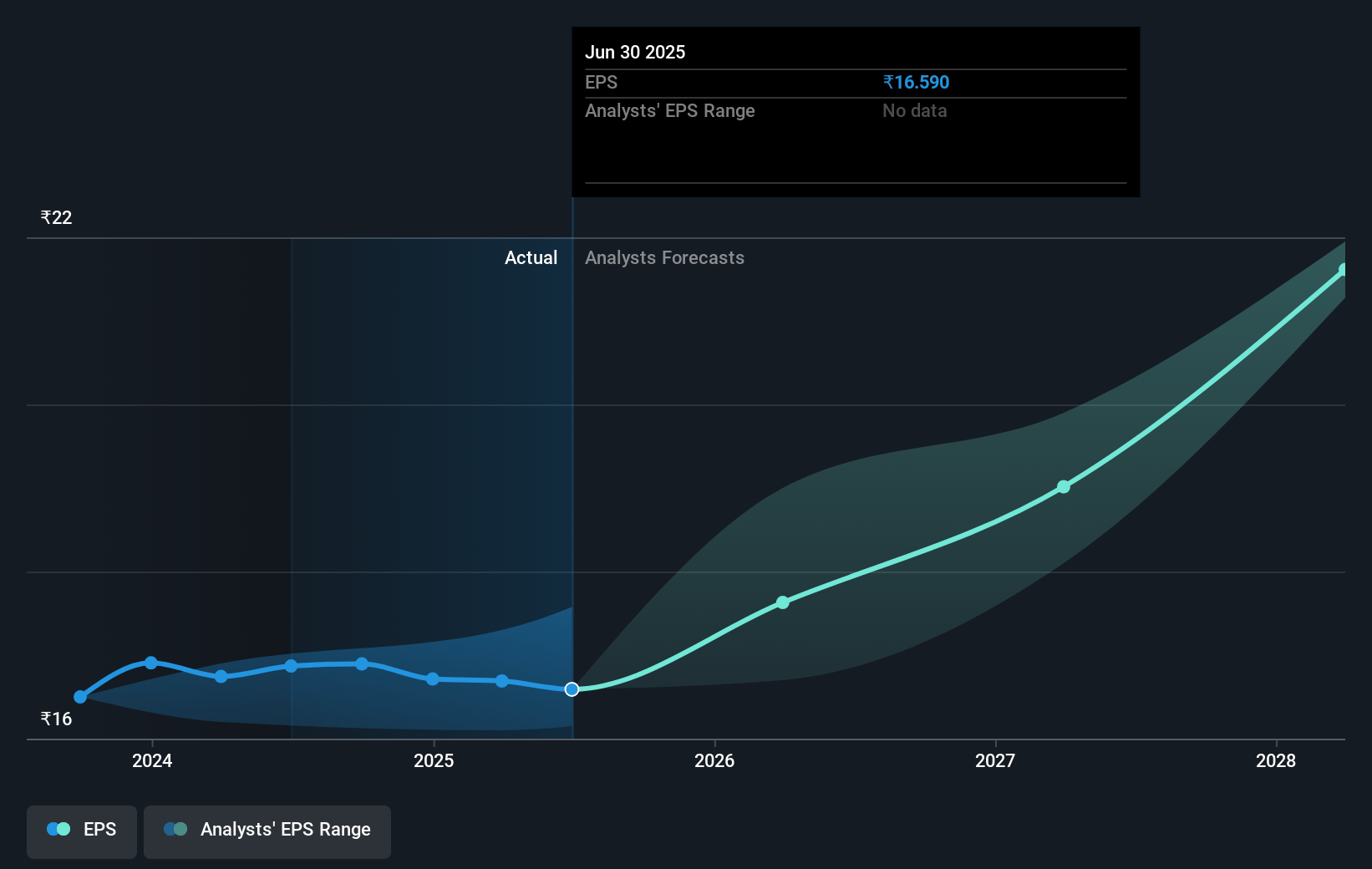

- Analysts expect earnings to reach ₹184.3 billion (and earnings per share of ₹19.66) by about May 2028, up from ₹155.4 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 23.7x on those 2028 earnings, up from 18.4x today. This future PE is lower than the current PE for the IN Electric Utilities industry at 33.2x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.53%, as per the Simply Wall St company report.

Power Grid Corporation of India Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The impact of the CERC tariff for regulations, showing a reduction of ₹140 crores in Q3, indicates regulatory challenges, which can affect the operating margins and profitability.

- There are significant challenges in project execution due to land acquisition and equipment supply, particularly with high voltage transformers and some conductors. These could lead to delays, affecting project capitalization timelines and revenue recognition.

- The reliance on debt to finance elevated CapEx plans, with a debt-equity ratio at 59:41, poses financial leverage risks that could impact net margins and profitability if interest rates fluctuate unfavorably or if debt levels become unsustainable.

- There are ongoing issues with delayed payments from several states like Tamil Nadu, Uttar Pradesh, Telangana, and Madhya Pradesh, contributing to a high accounts receivable figure, which could affect liquidity and net earnings.

- Losses from Power Grid's JV, EESL, which contributed ₹140 crores loss in the 9 months, create a potential drag on consolidated earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹329.833 for Power Grid Corporation of India based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹396.0, and the most bearish reporting a price target of just ₹241.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹534.1 billion, earnings will come to ₹184.3 billion, and it would be trading on a PE ratio of 23.7x, assuming you use a discount rate of 12.5%.

- Given the current share price of ₹307.45, the analyst price target of ₹329.83 is 6.8% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.