Narratives are currently in beta

Key Takeaways

- Construction of the world's largest renewable plant and strategic power agreements boost Adani Green's revenue stability and operational growth.

- Battery storage innovation and TotalEnergies partnership optimize margins and diversify ownership, enhancing financial growth and reducing risks.

- Project delays, rising internal interest expenses, and competitive pressures could strain Adani Green Energy's profitability and revenue stability, impacting overall financial performance.

Catalysts

About Adani Green Energy- Generates and supplies renewable energy to central and state government entities, and government backed corporations in India.

- The ongoing construction of the world's largest renewable energy plant at Khavda in Gujarat, with a potential capacity addition of 30 gigawatts, positions Adani Green Energy to significantly boost its energy output in the coming years, potentially increasing revenue substantially.

- The company's commitment to adding 6 gigawatts of renewable capacity in the current financial year, backed by detailed planning and execution strategies, signals robust growth in operational capacity. This is likely to enhance revenues and improve net margins as operational efficiencies are realized.

- The receipt of a letter of award for the supply of 5 gigawatts of solar power to Maharashtra State Discom through a 25-year fixed tariff PPA secures guaranteed future revenue streams and enhances the company's contracted portfolio, contributing positively to revenue stability and predictability.

- Adani Green Energy's pursuit of battery storage opportunities, supported by a 66% drop in battery prices over the last two years, aims to optimize their energy offerings by capturing significant price arbitrage between peak and off-peak hours. This innovation could lead to higher future margins and earnings.

- The strategic partnership with TotalEnergies, which involves a new joint venture and an investment of USD 444 million, strengthens Adani Green's financial position and provides additional capital for expansion, enhancing earnings potential and reducing financial risk through diversified ownership.

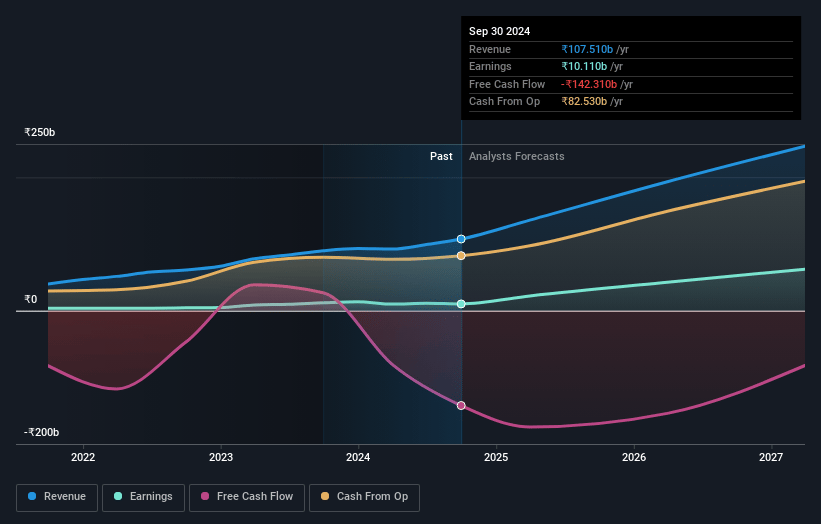

Adani Green Energy Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Adani Green Energy's revenue will grow by 41.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.4% today to 27.7% in 3 years time.

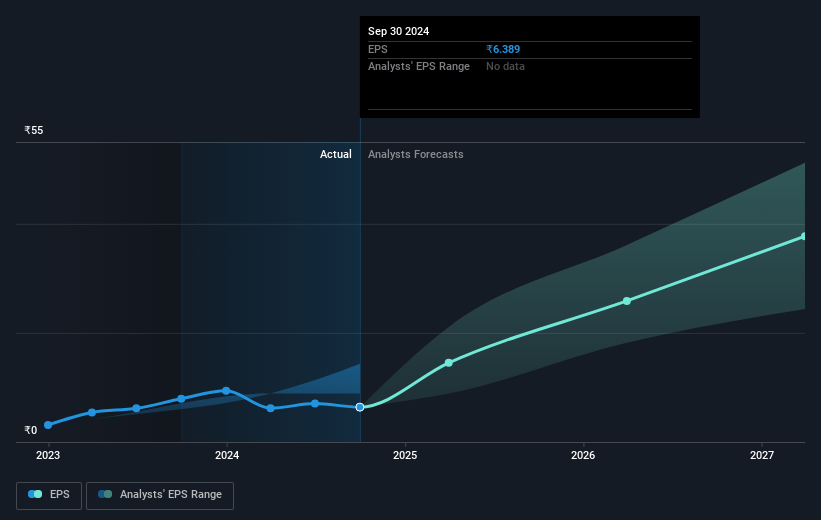

- Analysts expect earnings to reach ₹84.1 billion (and earnings per share of ₹37.69) by about January 2028, up from ₹10.1 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as ₹40.2 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 74.5x on those 2028 earnings, down from 163.9x today. This future PE is greater than the current PE for the IN Renewable Energy industry at 23.5x.

- Analysts expect the number of shares outstanding to grow by 12.12% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.64%, as per the Simply Wall St company report.

Adani Green Energy Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The extension of the monsoon has caused some delays in construction projects, which could lead to project completion being pushed back, potentially impacting revenue realization timelines and increasing costs.

- Increasing internal interest expenses and a significant minority interest can reduce the overall profitability accruing to Adani shareholders, as seen in the declining PAT figures, which could pressure net margins.

- The large merchant power exposure, especially with volatile prices, might lead to revenue fluctuations and earnings unpredictability, as merchant prices are affected by seasonal and hydel electricity variations.

- Although the company has plans for substantial capacity additions, any disruptions in securing and allocating land, or unforeseen transmission constraints, could impact future revenue growth and operational execution.

- The participation in highly competitive tenders with low pricing may not always result in securing sufficiently profitable contracts, which could strain net margins and financial sustainability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹1966.25 for Adani Green Energy based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹2550.0, and the most bearish reporting a price target of just ₹800.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹303.5 billion, earnings will come to ₹84.1 billion, and it would be trading on a PE ratio of 74.5x, assuming you use a discount rate of 12.6%.

- Given the current share price of ₹1046.4, the analyst's price target of ₹1966.25 is 46.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives