Key Takeaways

- Heavy reliance on bulk cargo and group companies exposes the business to demand fluctuations, related-party risks, and profit instability.

- Aggressive expansion and industry disruption heighten financial risks, margin pressure, and threats from evolving competition and technology.

- Strategic expansion of port and logistics operations, diversified revenue streams, and financial strength position the company for sustained growth, resilience, and improved profitability.

Catalysts

About JSW Infrastructure- An infrastructure development company, operates commercial ports in India and internationally.

- Rapid global decarbonization and the accelerating adoption of stricter ESG regulations threaten to reduce demand for coal and other bulk commodities, making JSW Infrastructure's reliance on bulk cargo growth vulnerable and risking both volume growth and revenue expansion over the long term.

- The company's aggressive capital expenditure plans-to double port capacity and significantly scale up the logistics segment by 2030-will require heavy debt funding. A deteriorating global trade environment, combined with possible project delays or cost overruns, may lead to higher finance costs, lower returns on capital, and long-term margin pressure.

- Increased automation and digitalization in global logistics raise the prospect of disruption from more agile, technology-led competitors, potentially eroding JSW Infrastructure's market share and compressing future EBITDA margins as pricing power shifts.

- JSW's high dependence on JSW Group companies for a significant portion of cargo throughputs exposes it to related-party concentration risks. Any downturn, restructuring, or stagnation within the broader JSW Group could translate directly into lower asset utilization and profit volatility, undermining the sustainability of earnings growth.

- Intensifying competition from private port operators as well as potential shifts in cargo movement from traditional ports to alternative freight corridors or inland waterways may diminish long-term demand for JSW Infrastructure's assets. This risks both revenue growth and industry-leading margin assumptions as the sector enters a structurally more competitive, less profitable phase.

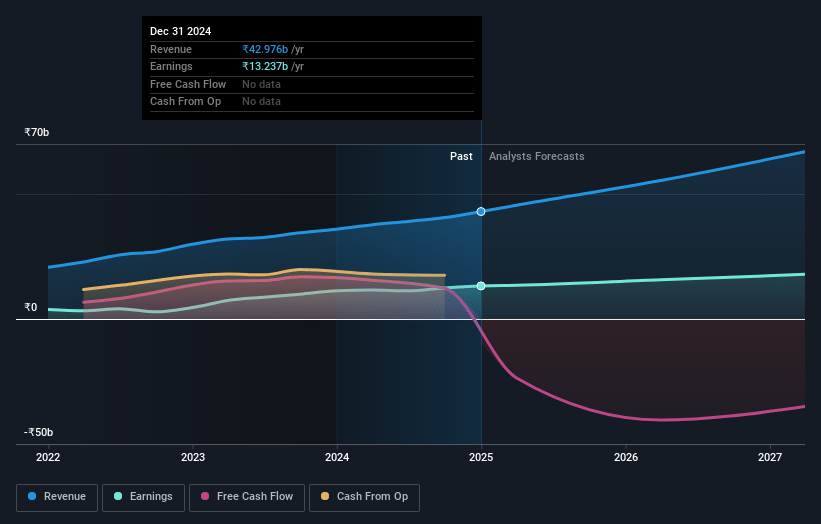

JSW Infrastructure Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on JSW Infrastructure compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming JSW Infrastructure's revenue will grow by 25.7% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 33.5% today to 18.4% in 3 years time.

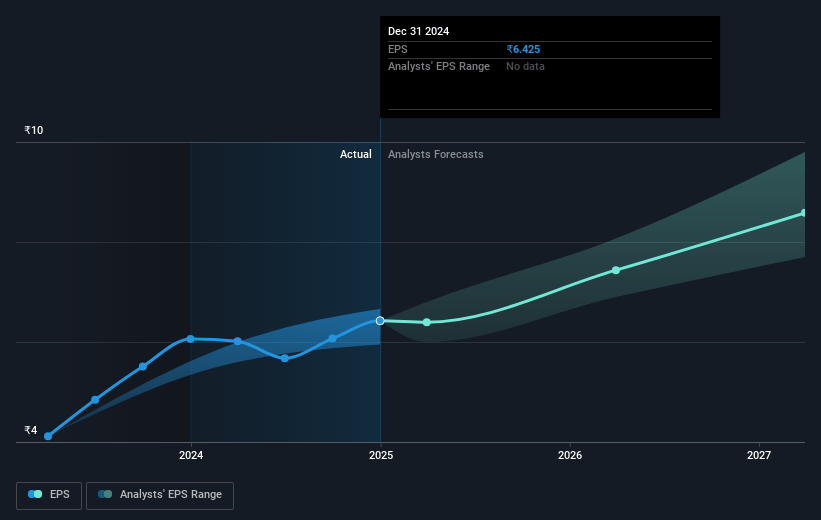

- The bearish analysts expect earnings to reach ₹16.4 billion (and earnings per share of ₹8.24) by about July 2028, up from ₹15.0 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 46.7x on those 2028 earnings, up from 42.9x today. This future PE is greater than the current PE for the IN Infrastructure industry at 17.3x.

- Analysts expect the number of shares outstanding to grow by 0.68% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 16.24%, as per the Simply Wall St company report.

JSW Infrastructure Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Significant government-driven expansion of India's port capacity, increased privatization, and focus on logistics infrastructure as part of major national initiatives position JSW Infrastructure to benefit from rising cargo volumes and improved asset utilization, supporting long-term revenue and earnings growth.

- Rapid growth in third-party cargo volumes and ongoing diversification efforts are reducing customer concentration risks, leading to a more balanced and resilient revenue mix while broadening the addressable market over time.

- Aggressive capacity expansion plans, both through greenfield and brownfield projects, along with timely execution and new long-term agreements-such as the slurry pipeline and take-or-pay contracts-indicate a strong pipeline for future volume and EBITDA growth.

- The company's commitment to an asset-light model in its logistics segment and integration of acquisitions like Navkar are expected to drive operational efficiencies, expand margins, and substantially increase logistics revenue and profitability in the coming years.

- JSW Infrastructure's industry-leading balance sheet with low net debt to EBITDA, combined with escalating annual cash flows, provides financial flexibility to fund future expansion while maintaining healthy profit margins and return on capital, supporting long-term net profit stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for JSW Infrastructure is ₹230.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of JSW Infrastructure's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹385.0, and the most bearish reporting a price target of just ₹230.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be ₹89.1 billion, earnings will come to ₹16.4 billion, and it would be trading on a PE ratio of 46.7x, assuming you use a discount rate of 16.2%.

- Given the current share price of ₹311.3, the bearish analyst price target of ₹230.0 is 35.3% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives