Narratives are currently in beta

Key Takeaways

- Expanding 5G infrastructure and efficient deployment is expected to enhance revenue and earnings through improved operational efficiencies and additional revenue streams.

- Renewable energy initiatives and strategic cost reduction measures are projected to significantly improve margins and financial stability, supporting future shareholder value initiatives.

- Heavy reliance on Vodafone Idea and high execution risks in new ventures could strain Indus Towers' financial stability and future profitability.

Catalysts

About Indus Towers- A telecom infrastructure company, engages in the operation and maintenance of wireless communication towers and related infrastructures for various telecom service providers in India.

- The implementation of the Right of Way Rules 2024, which aims to expedite telecom infrastructure deployment, is expected to improve operational efficiencies and streamline revenue growth as new deployments become easier and quicker. This could lead to enhanced revenue growth due to faster rollout capabilities and decreased deployment costs.

- As renewable energy initiatives expand, including solar site installations and strategic partnerships for energy procurement, Indus Towers is likely to reduce operational costs significantly. This will potentially improve net margins due to a decrease in energy expenditure and an increase in cost efficiency.

- The comprehensive rollout and gradual increase in 5G infrastructure by Indus Towers, coupled with the growing adoption of 5G technology, is expected to boost future earnings. The use of existing towers for 5G co-locations will likely generate additional revenue streams as demand for 5G infrastructure increases across regions.

- Indus Towers' focus on strategic operational efficiencies, such as reducing diesel consumption and transitioning to lithium-ion batteries, aims to optimize operational and capital expenses, thereby improving EBITDA margins and overall profitability in the medium to long term.

- The clearance of substantial overdues and favorable court rulings reducing liability risks enhance the financial stability of the company. This newfound financial flexibility and improved cash flow management are likely to support future dividends or buyback programs, possibly increasing EPS and enhancing shareholder value.

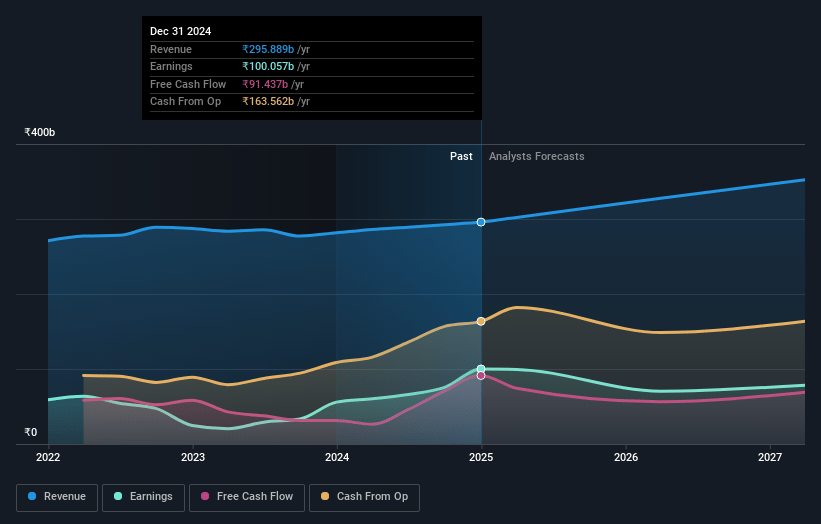

Indus Towers Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Indus Towers's revenue will grow by 7.8% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 33.8% today to 22.3% in 3 years time.

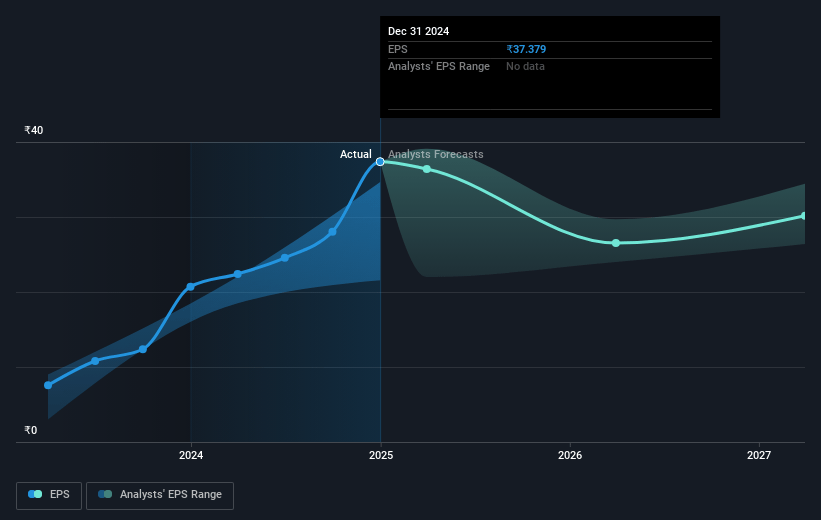

- Analysts expect earnings to reach ₹82.6 billion (and earnings per share of ₹25.93) by about January 2028, down from ₹100.1 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as ₹54.9 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 22.3x on those 2028 earnings, up from 9.1x today. This future PE is lower than the current PE for the IN Telecom industry at 35.6x.

- Analysts expect the number of shares outstanding to grow by 6.5% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.15%, as per the Simply Wall St company report.

Indus Towers Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The dependency on Vodafone Idea's expansion for tenancy growth could pose a risk if Vodafone Idea’s financial health declines, which might adversely affect future revenue projections.

- The energy margin losses remain a persistent issue, and despite the increase in renewable proportions, if these energy-related losses continue, it could impact net margins negatively.

- Intense competition in the telecommunications infrastructure sector, including from emerging competitors in small cells and IBS, might impact market share and future earnings.

- Any future rollout and financial delays with major clients like BSNL may lead to increased trade receivables and impact liquidity and cash flow, affecting net margins and earnings.

- The new strategic move into EV charging infrastructure, while diversifying potential revenue streams, carries high execution risk and uncertainty, which might strain financial resources and impact profitability in case of significant upfront investments without guaranteed returns.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹409.5 for Indus Towers based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹575.0, and the most bearish reporting a price target of just ₹280.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹371.0 billion, earnings will come to ₹82.6 billion, and it would be trading on a PE ratio of 22.3x, assuming you use a discount rate of 12.2%.

- Given the current share price of ₹346.7, the analyst's price target of ₹409.5 is 15.3% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives