Key Takeaways

- Leadership changes aim to enhance growth via digital transformation and improved market strategies, while focusing on innovative younger leadership.

- Expanding 5G coverage and digital services, alongside cost management initiatives, are set to boost revenue, diversify earnings, and improve net margins.

- High capital expenditures and customer churn challenge profitability, despite revenue growth and digital service expansion, potentially pressuring margins and earnings sustainability.

Catalysts

About Bharti Airtel- Operates as a telecommunications company in India and internationally.

- The appointment of Shashwat as CEO designate is part of a well-planned succession strategy, bringing in younger leadership to innovate and drive the India operations. This leadership change aims to enhance revenue growth through digital transformation and improved market strategies.

- Airtel's commitment to expanding its 5G coverage and improving service quality, as evidenced by its recent awards, is expected to drive higher Average Revenue Per User (ARPU) through new customer acquisition and upgrading existing customers to higher data plans, impacting earnings positively.

- Strategic investments in Airtel Finance, with plans to expand the portfolio across various financial products, aim to create a significant growth driver. This venture could positively impact the company's revenue and overall earnings as it scales.

- The focus on operational excellence and cost management, including its War on Waste initiative and switch to greener energy technologies, is anticipated to improve net margins over time by reducing expenses and capitalizing on efficiency gains.

- Airtel's expansion in digital services, including the cloud, IoT, CPaaS, and security, represents a substantial opportunity for non-mobile revenue streams. This diversification is expected to contribute significantly to overall revenue and earnings growth in the coming years.

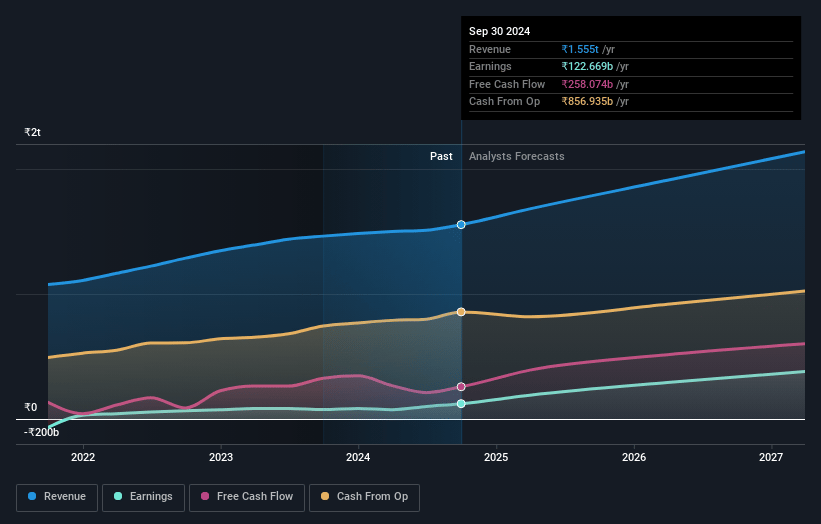

Bharti Airtel Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Bharti Airtel's revenue will grow by 13.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.9% today to 15.6% in 3 years time.

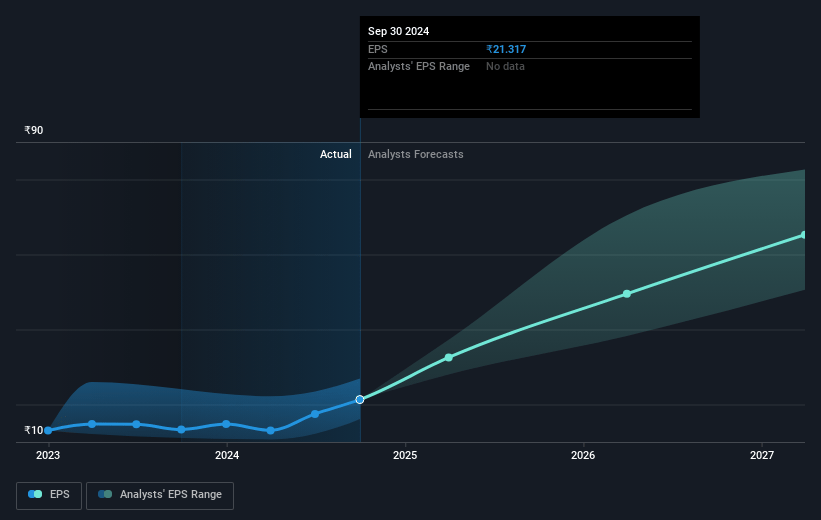

- Analysts expect earnings to reach ₹353.9 billion (and earnings per share of ₹64.91) by about January 2028, up from ₹122.7 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₹494.4 billion in earnings, and the most bearish expecting ₹212.0 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 39.5x on those 2028 earnings, down from 79.4x today. This future PE is lower than the current PE for the IN Wireless Telecom industry at 67.3x.

- Analysts expect the number of shares outstanding to decline by 3.61% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.15%, as per the Simply Wall St company report.

Bharti Airtel Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The loss of 2.9 million customers due to SIM consolidation triggered by a tariff repair suggests potential challenges in maintaining the customer base. This could impact revenues as it indicates customer churn and potential dissatisfaction.

- Despite the growth in revenues, the company acknowledges that the return on capital employed (ROCE) of the India business is still low at 11.2%, indicating that profitability may be an issue unless tariffs are further improved. This could impact net margins and overall earnings.

- The need to continuously invest in network expansion, such as the roll-out of additional 5,000 network sites and spectrum costs, indicates that high capital expenditures may continue, potentially impacting free cash flows and financial leverage.

- While there is growth in digital and financial services, the current revenue contribution is relatively small compared to the core business, suggesting limited immediate impact on revenue diversification or margin improvement.

- A large portion of the enterprise business revenue growth comes from adjacencies with lower margins and higher competition, such as cloud and security services, which might pressure overall EBITDA margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹1820.09 for Bharti Airtel based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹2350.0, and the most bearish reporting a price target of just ₹1120.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹2261.9 billion, earnings will come to ₹353.9 billion, and it would be trading on a PE ratio of 39.5x, assuming you use a discount rate of 12.2%.

- Given the current share price of ₹1599.5, the analyst's price target of ₹1820.09 is 12.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives