Key Takeaways

- Strategic wins with multinationals and government sectors may significantly boost future revenue through increased global technology spending.

- Expansion into U.S. and Europe, coupled with AI and innovative strategies, could enhance profitability and stabilize net margins.

- Financial stability faces potential threats from increased employee costs, cybersecurity risks, geographic expansion challenges, and dependence on fluctuating public sector projects.

Catalysts

About Allied Digital Services- Designs, develops, deploys, and delivers end-to-end IT infrastructure services and digital solutions in India, the United States, the United kingdom, and internationally.

- Allied Digital Services has secured over ₹200 crores in new orders and contract renewals, including high-profile wins with multinational corporations and government sectors, which could significantly boost revenue growth in the future.

- With strengths in digital engineering, cloud, and cybersecurity solutions, Allied Digital is positioned to capitalize on increased global enterprise technology spending, which could lead to higher earnings.

- The company is expanding its geographical footprint, with growth opportunities identified in the U.S. and potential expansion into European markets, which may enhance revenue streams.

- Allied Digital is focusing on enhancing its recurring revenue base, evidenced by a strategy to maintain a recurring revenue to solutions business mix, potentially stabilizing and increasing net margins.

- The firm is leveraging AI and innovative technology strategies to enhance efficiency and productivity, which could lead to improved net margins and profitability in the long term.

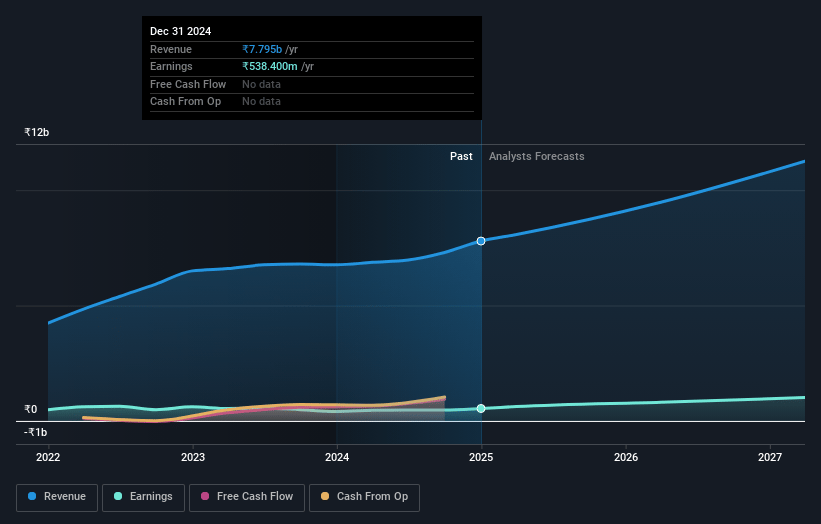

Allied Digital Services Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Allied Digital Services's revenue will grow by 16.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.0% today to 7.8% in 3 years time.

- Analysts expect earnings to reach ₹986.3 million (and earnings per share of ₹19.2) by about July 2028, up from ₹321.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 16.0x on those 2028 earnings, down from 31.2x today. This future PE is lower than the current PE for the IN IT industry at 30.1x.

- Analysts expect the number of shares outstanding to decline by 3.22% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 15.76%, as per the Simply Wall St company report.

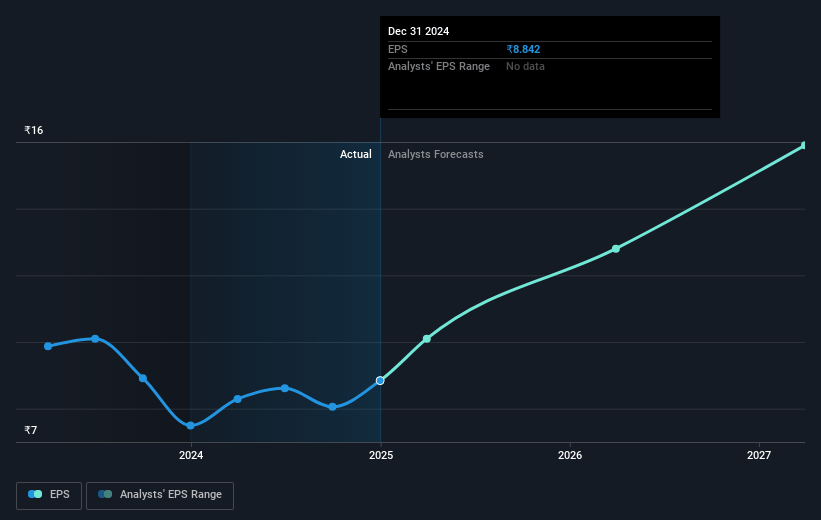

Allied Digital Services Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Allied Digital Services experienced an increase in employee costs due to rate hikes and the need to hire additional associates, which could potentially impact net margins in the future.

- The company faces cybersecurity risks, as evidenced by a recent incident involving a data breach with one of its clients, which could result in financial liabilities and impact earnings.

- The reclassification of employee costs and accounting adjustments affected gross margins, potentially complicating future financial stability and earnings predictability.

- Rapid geographic and service expansion, while potentially beneficial, carries execution risks and high initial investments, which could strain cash flow and net margins.

- While the company reports strong order wins, the reliance on public sector and smart city projects could expose it to regulatory changes and budget fluctuations, potentially impacting revenue consistency.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹200.0 for Allied Digital Services based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹12.7 billion, earnings will come to ₹986.3 million, and it would be trading on a PE ratio of 16.0x, assuming you use a discount rate of 15.8%.

- Given the current share price of ₹177.58, the analyst price target of ₹200.0 is 11.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.