Key Takeaways

- The integration of AI platforms enhances deal sizes and modernization opportunities, expanding the market and boosting future revenues and net margins.

- Strong pipeline growth and significant large deal activity highlight opportunities for revenue growth and improved operational efficiency.

- Challenges in logistics and high competitive intensity may pressure margins and question the sustainability of AI-led productivity gains impacting long-term revenue.

Catalysts

About Mphasis- Operates as an information technology solutions provider that specializes in cloud and cognitive services in the United States, India, Europe, the Middle East, Africa, and internationally.

- The integration of AI platforms like Mphasis NeoZeta and NeoCrux is expected to supersize deals, unlocking modernization opportunities and expanding the total addressable market, positively impacting future revenue growth.

- The ability to augment AI projects with human capabilities is changing ROI economics, allowing for quicker transformations and modernization efforts that were previously cost-prohibitive, likely leading to an increase in net margins.

- The strong pipeline growth, with BFS pipeline up 58% Y-o-Y and non-BFS pipeline up 44% Y-o-Y, alongside a 49% increase in large deals sequentially, indicates potential for significant revenue growth.

- The ongoing shift towards automation and productivity gains—from AI-driven efforts and the establishment of the Cyber Fusion Center—supports enhanced operational efficiency, likely improving net margins.

- Focus on large deal activity, proactive wins, and an improvement in TCV closures by $351 million, with a high conversion pace from TCV to revenue earmarked, suggests potential for earnings growth through revenue acceleration.

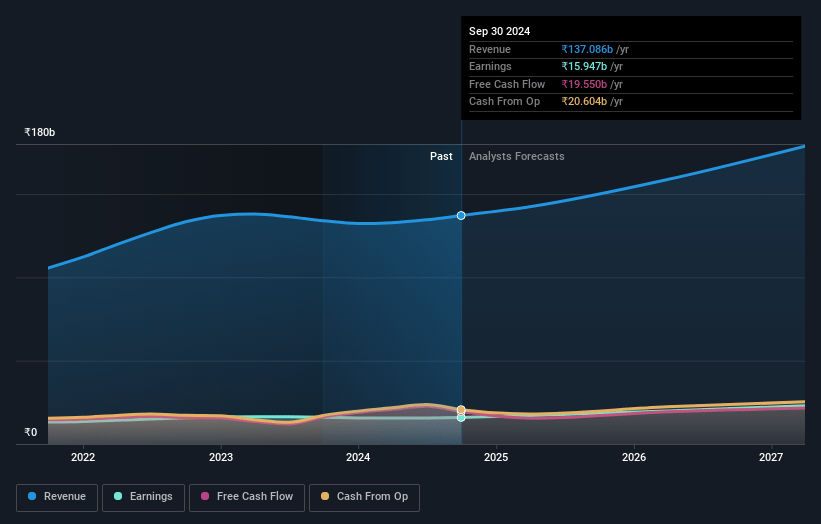

Mphasis Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Mphasis's revenue will grow by 11.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 11.8% today to 12.8% in 3 years time.

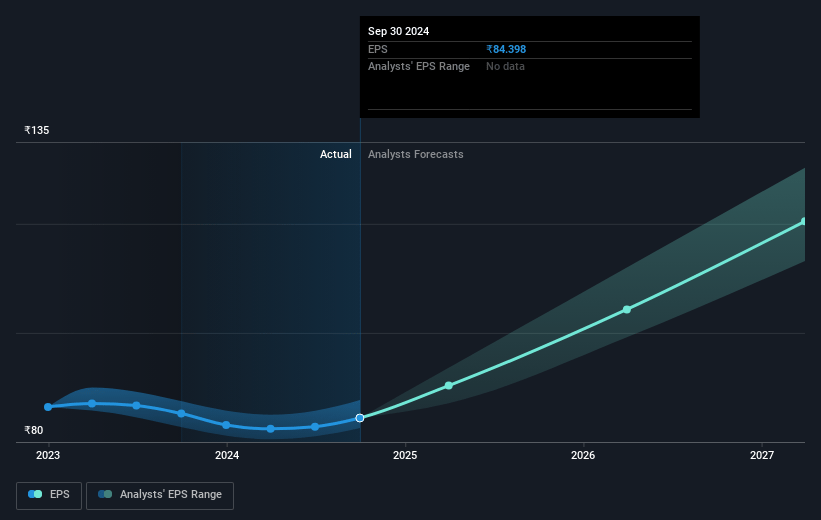

- Analysts expect earnings to reach ₹24.9 billion (and earnings per share of ₹138.55) by about April 2028, up from ₹16.5 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 33.2x on those 2028 earnings, up from 28.9x today. This future PE is greater than the current PE for the IN IT industry at 27.5x.

- Analysts expect the number of shares outstanding to grow by 0.35% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 15.25%, as per the Simply Wall St company report.

Mphasis Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company faces challenges in the logistics vertical, where there has been a decline not attributed to a single customer. This could indicate industry-specific challenges or broader macroeconomic factors impacting this segment, potentially affecting revenue negatively.

- The sharp decline in headcount over the last three years (down 15%) despite a 5% revenue increase during the same period may suggest over-reliance on productivity gains, which could lead to risks if efficiency gains do not sustain. This might pressure margins if increased hiring becomes necessary.

- There are supply chain and macroeconomic headwinds that could affect global demand in segments like logistics and non-airline transportation, potentially impacting the company's overall revenue growth.

- High competitive intensity in large deal consolidation, with some competitors possibly focusing more on savings, may limit Mphasis's ability to secure profitable pricing, thus compressing net margins.

- There are questions about the sustainability of AI-led productivity gains given that the company may need to pass on some benefits to customers, as industry peers have experienced, potentially affecting long-term earnings if efficiency-led gains are reinvested into pricing discounts.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹2807.424 for Mphasis based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹3700.0, and the most bearish reporting a price target of just ₹2140.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹194.4 billion, earnings will come to ₹24.9 billion, and it would be trading on a PE ratio of 33.2x, assuming you use a discount rate of 15.3%.

- Given the current share price of ₹2505.25, the analyst price target of ₹2807.42 is 10.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.