Narratives are currently in beta

Key Takeaways

- U.S. FDA approval enhances export potential to the U.S., expected to significantly boost revenue starting in fiscal year '27.

- Investments in sustainability and niche market expansion are projected to enhance operational efficiency, margin improvement, and future revenue growth.

- Ongoing challenges in revenue stability and margin pressures, coupled with high CapEx and competitive markets, risk hindering projected growth and financial performance.

Catalysts

About Aarti Drugs- Through its subsidiaries, manufactures and markets active pharmaceutical ingredients (APIs), pharmaceutical intermediates, specialty chemicals, and formulations in India and internationally.

- The recent U.S. FDA approval for Aarti Drugs' API manufacturing facility allows the company to export products such as Ciprofloxacin HCL and Zolpidem Tartrate to the U.S. market, which is expected to increase revenue streams significantly beginning FY '27.

- Aarti Drugs' investment in a solar power plant for captive consumption is projected to result in annual cost savings and reduce carbon emissions, potentially improving net margins by reducing operational costs.

- The company's greenfield project for Specialty Chemicals in Sayakha, which aligns with backward integration, is expected to boost capacity utilization and gross margins as it begins production.

- Expansion of the Sayakha facility and the new product launches in niche segments such as antifungal agents and dermatology products could drive future revenue growth and EBITDA.

- Aarti Drugs aims to achieve 13% to 14% EBITDA margins by FY '26 through operational efficiencies and market expansion into highly regulated markets, enhancing overall profitability.

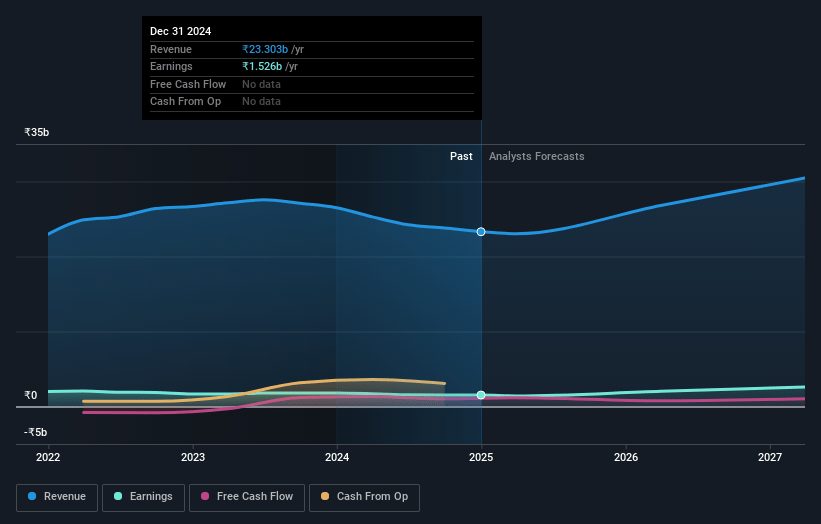

Aarti Drugs Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Aarti Drugs's revenue will grow by 12.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.5% today to 9.4% in 3 years time.

- Analysts expect earnings to reach ₹3.1 billion (and earnings per share of ₹34.32) by about February 2028, up from ₹1.5 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 19.0x on those 2028 earnings, down from 24.9x today. This future PE is lower than the current PE for the IN Pharmaceuticals industry at 31.0x.

- Analysts expect the number of shares outstanding to decline by 0.17% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.15%, as per the Simply Wall St company report.

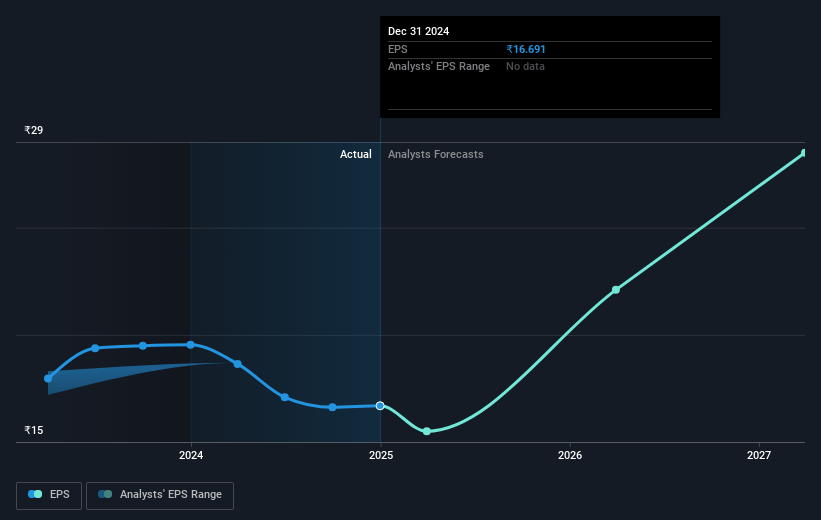

Aarti Drugs Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's revenue has declined by 6% year-over-year due to reduced market prices and weaker demand in the Formulation and Antibiotics API segments, which could impact future revenue stability.

- Despite new investments, there are ongoing pricing pressures in the API segment driven by fluctuating raw materials, heightened competition, and regulatory demands, which could impact gross and net margins.

- Financial performance may be adversely affected by high capital expenditure (CapEx) plans of around ₹200 crores primarily funded through internal accruals and term loans, potentially impacting earnings if expected returns do not materialize.

- There are operational risks due to ongoing challenges and past issues such as manufacturing setbacks that could hinder the expected ramp-up in production capacities, impacting expected revenue growth and gross margins.

- The competitive pressures in regulated markets like the U.S. and Europe could result in reduced market share or pricing power, which may prevent the company from achieving the projected EBITDA margin improvement targets.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹465.0 for Aarti Drugs based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹33.4 billion, earnings will come to ₹3.1 billion, and it would be trading on a PE ratio of 19.0x, assuming you use a discount rate of 12.2%.

- Given the current share price of ₹413.4, the analyst's price target of ₹465.0 is 11.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives