Narratives are currently in beta

Key Takeaways

- Safety concerns and expansion delays could increase costs and slow growth, potentially impacting future margins and revenue.

- Ambitious energy and sustainability projects may strain short-term earnings through required investments and hedging activities.

- Strong operational performance and strategic cost reductions enhance profitability, while renewable energy and innovative projects position Hindustan Zinc for long-term growth and revenue potential.

Catalysts

About Hindustan Zinc- Explores for, extracts, and processes minerals in India, rest of Asia, and internationally.

- Concerns about safety incidents, such as the fatal accident at the Sindesar Khurd mine, could lead to increased scrutiny and potential operational changes. These could result in higher operating costs and possibly impact net margins negatively if additional safety investments are required.

- Expansion plans to reach a 2 million tonne production run rate are in early stages, and delays or execution risks associated with these plans could lead to slower-than-expected growth in production volumes, impacting future revenue growth.

- The transition to renewable energy to cover 70% of operational power is ambitious and, while potentially reducing long-term costs, could involve upfront investment costs that might temporarily affect net margins.

- Hedging activities, such as the forward sale of zinc and silver to manage market volatility, could limit financial flexibility and expose the company to potential losses if market prices exceed hedge prices, impacting earnings stability.

- The company's ongoing initiatives in zinc-based battery technology and other sustainability projects may require significant R&D investment with uncertain near-term returns, possibly affecting earnings if these projects do not yield expected commercial successes.

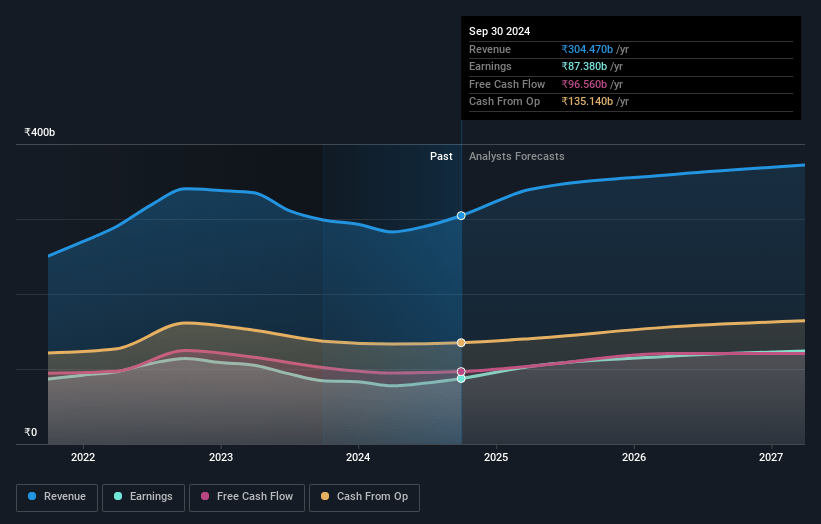

Hindustan Zinc Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Hindustan Zinc's revenue will grow by 8.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 28.7% today to 34.9% in 3 years time.

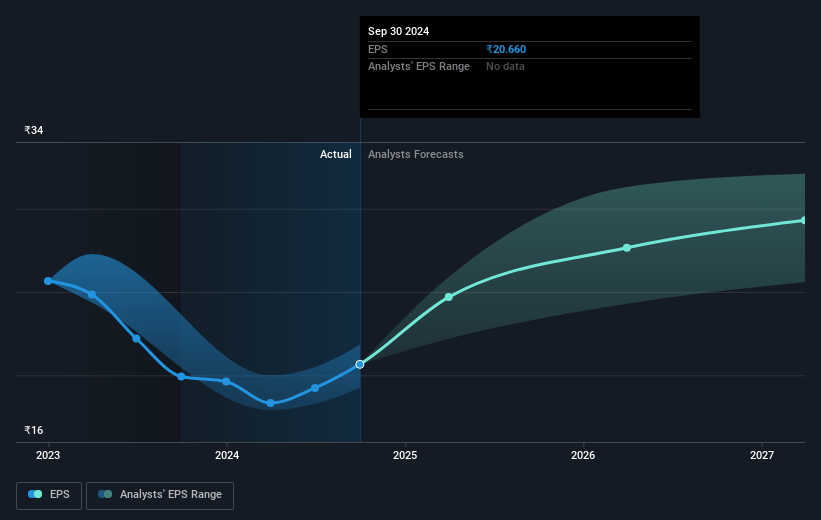

- Analysts expect earnings to reach ₹137.0 billion (and earnings per share of ₹29.3) by about December 2027, up from ₹87.4 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 21.5x on those 2027 earnings, down from 23.5x today. This future PE is greater than the current PE for the IN Metals and Mining industry at 16.2x.

- Analysts expect the number of shares outstanding to grow by 3.45% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.17%, as per the Simply Wall St company report.

Hindustan Zinc Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Hindustan Zinc has recorded its highest ever second quarter and half-year mined and refined metal production, which indicates a strong operational performance that supports potential revenue growth.

- The company is implementing significant cost reductions, including a 6% year-over-year reduction in costs, which has enhanced net profit by 35% and improved EBITDA margins to over 50%, benefiting earnings.

- A strategic shift towards renewable energy usage is expected to reduce power costs over 25 years, enhancing net margins by stabilizing energy costs long-term.

- There is a bullish outlook on metal prices, with zinc prices stabilizing around $3,000 and increased demand from India's expanding economy, potentially boosting future revenue.

- Hindustan Zinc's strategic partnerships and innovative projects, including zinc-based battery development and the scale-up of fumers, highlight the potential for future growth in earnings through diversified product offerings and reduced operational gaps.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹423.33 for Hindustan Zinc based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹570.0, and the most bearish reporting a price target of just ₹305.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be ₹393.0 billion, earnings will come to ₹137.0 billion, and it would be trading on a PE ratio of 21.5x, assuming you use a discount rate of 14.2%.

- Given the current share price of ₹485.3, the analyst's price target of ₹423.33 is 14.6% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives