Narratives are currently in beta

Key Takeaways

- Strategic investments in advertising and rural initiatives indicate a focus on long-term revenue growth, despite short-term profitability pressures.

- Growing market share in household insecticides and international expansion in Indonesia and Latin America are expected to diversify and boost earnings.

- Underperformance in India, high palm oil prices, and weak urban markets could pressure sales, margins, and revenue growth for Godrej Consumer Products.

Catalysts

About Godrej Consumer Products- A fast-moving consumer goods company, engages in the manufacture and marketing of personal care and home care products in India, Africa, Indonesia, the Middle East, the United States of America, and internationally.

- The company expects that majority of their current issues are transitory and anticipates sequential improvement in both volume and value growth by Q4 FY '25, with hopes of margin growth by H1 FY '26. This should positively impact both revenue and net margins in the future.

- Godrej Consumer Products is gaining rapid market share in incense sticks and electrics within their household insecticide business, indicating potential for future revenue growth as these segments recover and expand.

- The company’s commitment to maintaining advertising spend and investment in programs like the rural van initiative despite short-term profitability pressures suggests a strategic focus on long-term revenue and market share growth, particularly in rural areas where growth outpaces urban areas.

- Their international businesses, especially in Indonesia and Latin America, show promising growth with potential margin improvements. This should help diversify and strengthen consolidated earnings, supporting overall financial performance.

- Improved supply chain management and pricing strategies in response to falling palm oil prices are expected to allow normalization of EBITDA margins in the soaps category, which should eventually enhance earnings as price adjustments stabilize.

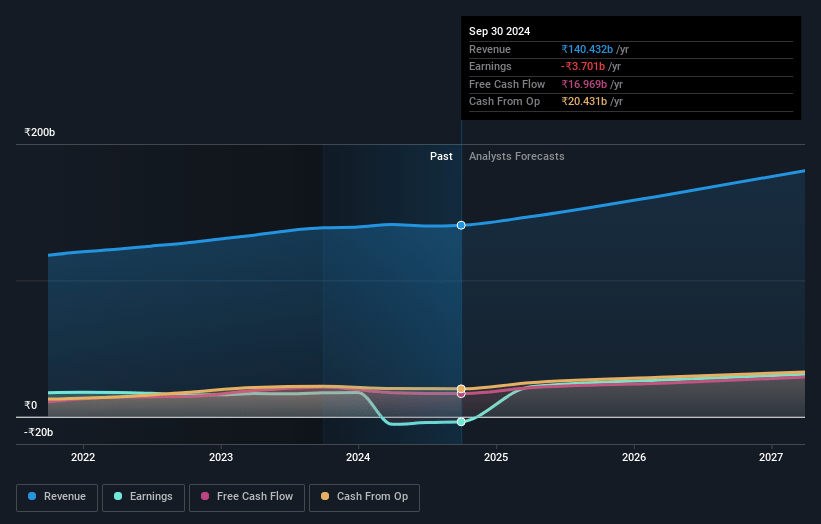

Godrej Consumer Products Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Godrej Consumer Products's revenue will grow by 9.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from -3.2% today to 23.6% in 3 years time.

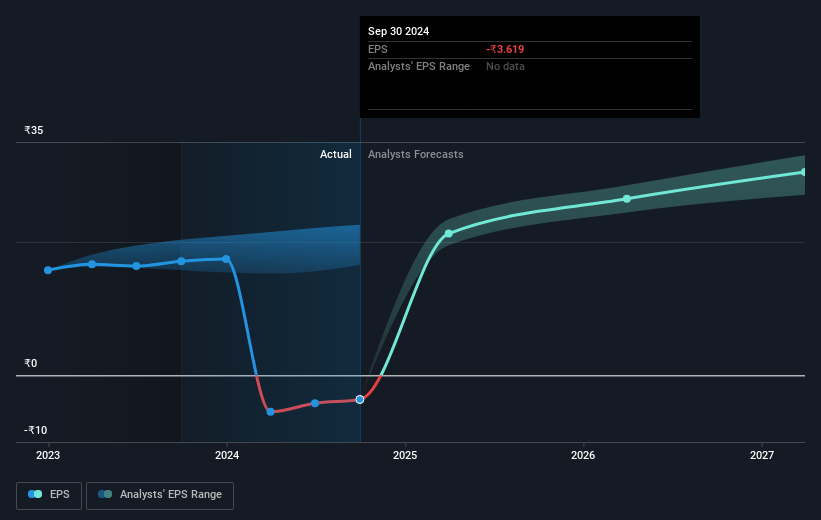

- Analysts expect earnings to reach ₹43.7 billion (and earnings per share of ₹42.86) by about January 2028, up from ₹-4.5 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 44.4x on those 2028 earnings, up from -252.6x today. This future PE is lower than the current PE for the IN Personal Products industry at 52.0x.

- Analysts expect the number of shares outstanding to decline by 0.09% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 13.5%, as per the Simply Wall St company report.

Godrej Consumer Products Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's India business has underperformed, with flat volume growth and a 21% decline in EBITDA, largely due to a slowdown in urban consumption and high palm oil prices, directly affecting revenue and net margins.

- Persistent inflation in palm oil prices and resulting increased prices for products like soaps could continue to pressure sales volumes and profitability, impacting future earnings.

- The complexity of rolling out the new RNF formulation for household insecticides, with only 40-50% market penetration, could affect consumer reception and thus revenue growth.

- Weakness in urban markets, particularly in modern trade and among premium products, poses a risk to expected revenue, as the company has a higher dependency on urban consumers.

- Competitive pressures and the need for further price hikes in the soap segment to maintain margins may impact market share and profitability, affecting future revenue and earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹1301.2 for Godrej Consumer Products based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹1530.0, and the most bearish reporting a price target of just ₹977.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹185.4 billion, earnings will come to ₹43.7 billion, and it would be trading on a PE ratio of 44.4x, assuming you use a discount rate of 13.5%.

- Given the current share price of ₹1118.15, the analyst's price target of ₹1301.2 is 14.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives