Narratives are currently in beta

Key Takeaways

- ONGC aims to boost oil and gas production through new wells and projects, potentially increasing revenues and profitability amid high market prices.

- Debt reduction in its subsidiary OPaL could decrease interest expenses, enhancing ONGC's profit margins and net earnings.

- Declining profits, lower crude oil prices, and increasing costs threaten ONGC's financial stability, while investments in subsidiaries pose significant operational and financial risks.

Catalysts

About Oil and Natural Gas- Engages in the exploration, development, and production of crude oil and natural gas in India and internationally.

- ONGC is focusing on reversing the declining trend in crude oil production by opening new oil wells, such as the three wells in the deepwater block KG-DWN-98/2, which could increase oil production, potentially leading to higher revenues.

- The allocation of gas resources from new wells and increased well intervention activities indicates a strategy to enhance gas production, which could improve net earnings due to potentially higher gas prices.

- Investments in ONGC's subsidiary, OPaL, include significant debt reduction, which may improve future profit margins for ONGC as interest expenses decrease, leading to a potential increase in net earnings.

- The development of new projects, such as the Daman upside and DSF-II gas projects, will come online by FY '26, possibly augmenting production volumes and contributing to future revenue growth.

- The company's strategic increase in gas production from high-profile projects like KG-DWN-98/2, with plans to achieve peak output, could lead to enhanced profitability and improved earnings given the potential for high gas prices in the market.

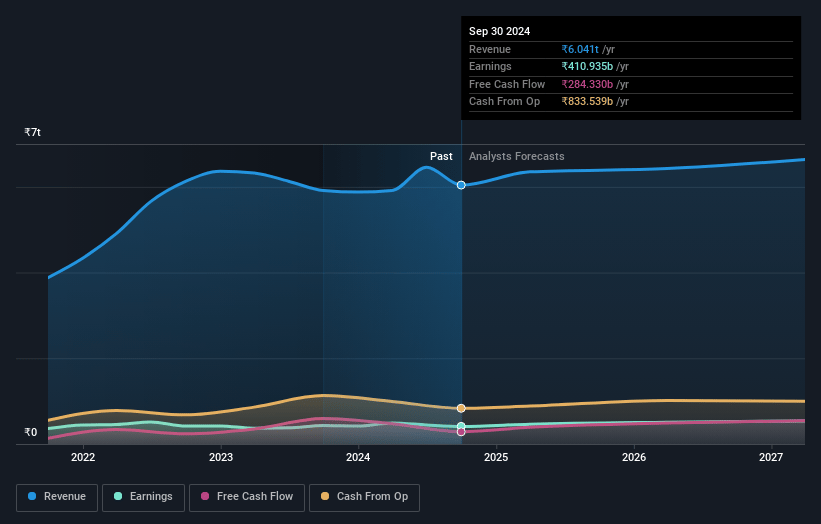

Oil and Natural Gas Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Oil and Natural Gas's revenue will grow by 3.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.8% today to 8.6% in 3 years time.

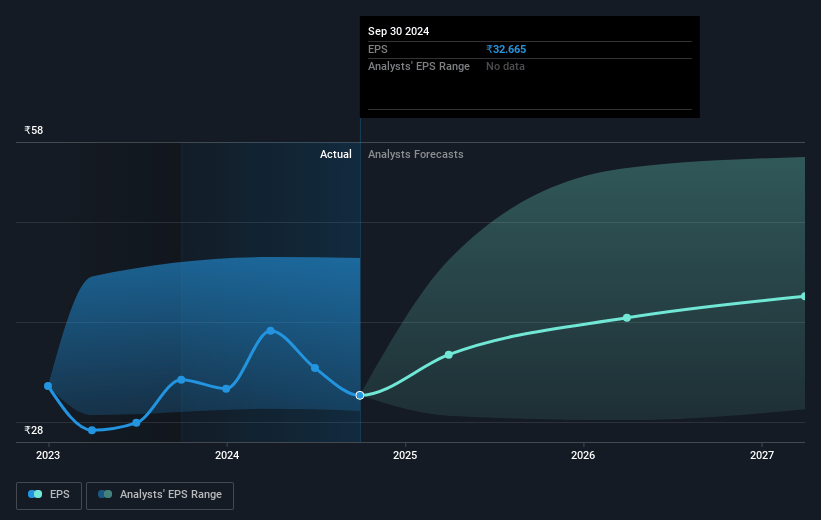

- Analysts expect earnings to reach ₹579.2 billion (and earnings per share of ₹42.28) by about January 2028, up from ₹410.9 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₹710.0 billion in earnings, and the most bearish expecting ₹393.4 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.5x on those 2028 earnings, up from 7.7x today. This future PE is lower than the current PE for the IN Oil and Gas industry at 20.6x.

- Analysts expect the number of shares outstanding to grow by 2.88% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 15.88%, as per the Simply Wall St company report.

Oil and Natural Gas Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The decline in net profit at the consolidated level by 38.92% for the second quarter and 41.52% for H1 FY '25, mainly due to the decline in profits of subsidiaries like HPCL and MRPL, could be a risk to ONGC’s overall earning potential in future quarters.

- Lower crude oil prices have led to a decrease in sales revenue for Q2 FY '25 by 3.5%, which could further impact revenue if the trend continues, given the reliance on oil prices for revenue generation.

- The increasing operating expenditure, with a rise of 4.5% from Q2 FY '24 to Q2 FY '25, poses a risk to net margins and overall profitability if expenses continue to outpace revenue growth.

- ONGC faces exploration cost pressures, reflected by an increase of ₹631 crores in exploration costs written off in H1 FY '25, due to expanded activities and unsuccessful ventures such as the Vindhyan Basin, impacting net margins.

- The substantial capital infusion in OPaL and acquisition of a 95.69% stake raises concerns about the high operational and financial risks associated with this investment, which may affect cash flow and profitability if OPaL fails to deliver improved financial performance quickly.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹313.28 for Oil and Natural Gas based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹430.0, and the most bearish reporting a price target of just ₹215.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹6738.6 billion, earnings will come to ₹579.2 billion, and it would be trading on a PE ratio of 11.5x, assuming you use a discount rate of 15.9%.

- Given the current share price of ₹251.4, the analyst's price target of ₹313.28 is 19.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives