Narratives are currently in beta

Key Takeaways

- Strong growth in assets under advice indicates a positive trend for future revenue, driven by increased mutual fund folios and organized investments.

- Wealth Management and Asset Management sectors are poised for significant growth, leveraging distribution expansion and rising HNI wealth to improve margins.

- The company faces risks from potential revenue declines across broking, wealth management, housing finance, and asset management due to market conditions and regulatory pressures.

Catalysts

About Motilal Oswal Financial Services- Offers financial services in India.

- Strong growth in assets under advice, which have crossed ₹6 lakh crore, a 62% increase year-on-year, driven by low penetration of financial savings and a rise in mutual fund folios and demat accounts. This is expected to boost future revenue growth as the company benefits from the larger financial ecosystem shift towards organized investments.

- The Wealth Management business is poised for growth with a focus on distribution expansion, including a 67% year-on-year increase in assets under advice, leading to a potential rise in both revenue and net margins through economies of scale and higher fee-based income.

- Significant gains in the Asset Management business, with a mutual fund AUM up by 128% year-on-year, supported by strong performance and expanding distribution network. This is expected to contribute to revenue growth and improve net margins through operating leverage.

- The Private Wealth Management business is set to capitalize on rising wealth among HNIs/UHNIs with enhanced senior-level hiring and a focus on productivity improvements, leading to potentially higher earnings and net margins.

- Investment in expanding lending segments, such as the Housing Finance business with disbursements up by 92% year-on-year, anticipates further growth in net interest income and earnings due to increased lending activity and improved spread management.

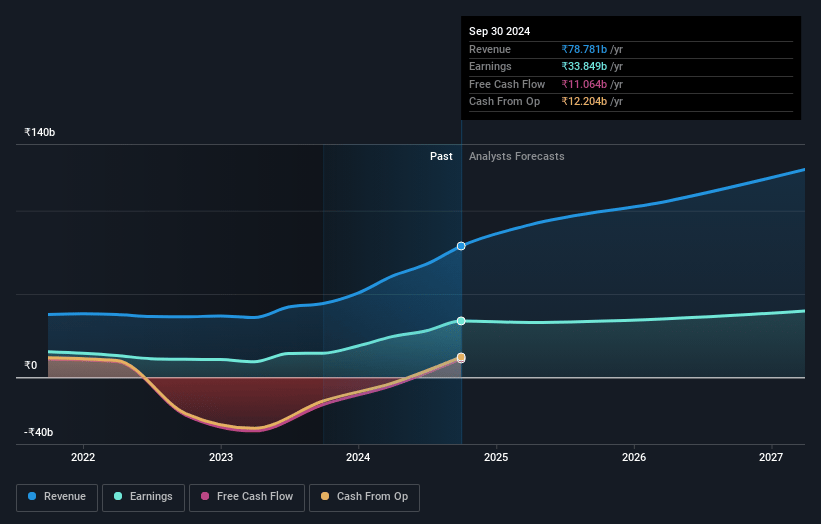

Motilal Oswal Financial Services Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Motilal Oswal Financial Services's revenue will grow by 21.6% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 41.1% today to 29.5% in 3 years time.

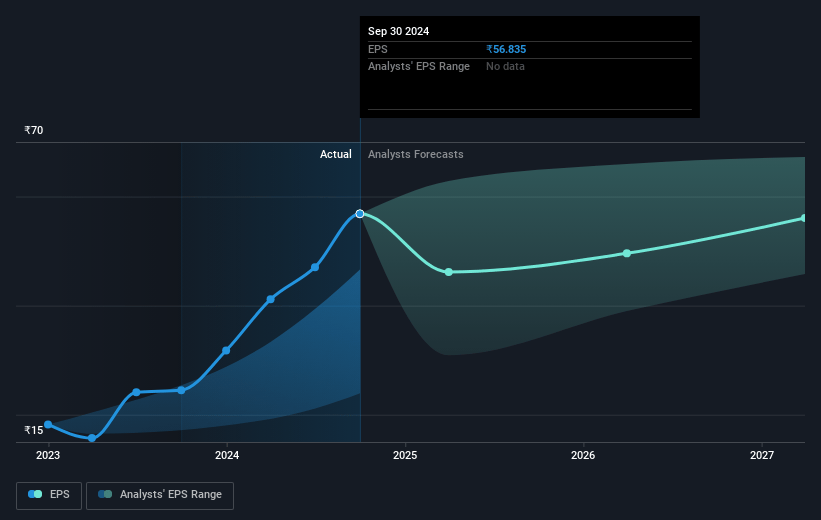

- Analysts expect earnings to reach ₹42.5 billion (and earnings per share of ₹59.21) by about January 2028, up from ₹32.9 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as ₹32.6 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 27.1x on those 2028 earnings, up from 12.2x today. This future PE is greater than the current PE for the IN Capital Markets industry at 20.7x.

- Analysts expect the number of shares outstanding to grow by 6.19% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.93%, as per the Simply Wall St company report.

Motilal Oswal Financial Services Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's revenue from broking might be impacted due to the potential decline in market share in both cash and derivatives segments, as well as regulatory changes affecting pricing and market volumes.

- There is a risk of declining revenue and profits from the wealth management segment due to increased compliance costs and the potential for market corrections, which could impact volumes and client activity levels.

- The housing finance business could face risks related to asset quality and credit losses, despite currently reporting strong numbers; any future deterioration in credit conditions could negatively impact net margins.

- The company's asset management business might face challenges if market volatility leads to reduced net inflows or increased redemption pressure, potentially impacting AUM growth and fee-based revenue.

- The reliance on increasing distribution and cross-sell efforts might not yield expected results if market conditions or customer behaviors change, affecting earnings growth projections for both wealth management and asset management segments.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹1059.5 for Motilal Oswal Financial Services based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹1200.0, and the most bearish reporting a price target of just ₹948.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹144.1 billion, earnings will come to ₹42.5 billion, and it would be trading on a PE ratio of 27.1x, assuming you use a discount rate of 14.9%.

- Given the current share price of ₹670.6, the analyst's price target of ₹1059.5 is 36.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives