Narratives are currently in beta

Key Takeaways

- The company's capital-light strategy and high-margin management fees are poised to significantly enhance future profitability.

- Expansion in new business verticals and portfolio growth plans are expected to drive revenue and market share growth.

- The reliance on one-time gains, specific regions, early-stage ventures, and external factors may lead to uneven and unpredictable revenue for Indian Hotels.

Catalysts

About Indian Hotels- Owns, operates, and manages hotels, palaces, and resorts in India and internationally.

- The hospitality sector is experiencing a strong up cycle driven by increasing domestic demand, limited supply, and favorable demographics. This trend is expected to sustain, potentially boosting revenue growth for Indian Hotels in the mid

- to long term.

- IHCL's capital-light growth strategy, which has led to increasing management fees, is a significant margin driver. The income from management fees, having a high-margin profile, is expected to enhance the overall profitability of the company in the future.

- New business verticals such as Ginger, Qmin, and Ama Stays & Trails have shown substantial revenue growth, with Ginger achieving a 55% year-on-year growth in consolidated revenue. These new businesses expand IHCL's market reach and are likely to impact overall earnings positively.

- The company is on track for substantial portfolio growth with plans to open 25 hotels this financial year and up to 30 in the next. This expansion is expected to contribute significantly to revenue growth and market share expansion.

- Strategic brand expansions and management agreements, such as with The Claridges, as well as acquisitions like Tree of Life, are set to enhance IHCL's brandscape. Such initiatives can lead to an increase in revenue streams and strengthen competitive positioning in the luxury and boutique hotel segments.

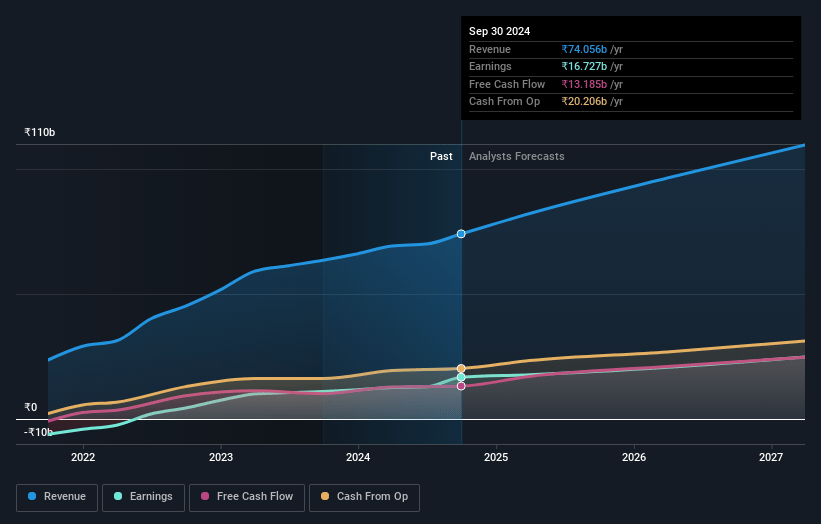

Indian Hotels Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Indian Hotels's revenue will grow by 17.2% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 22.6% today to 22.1% in 3 years time.

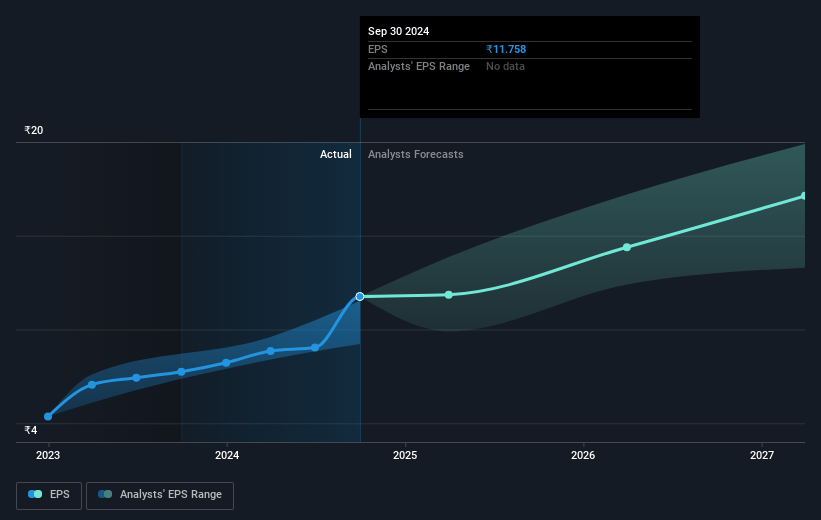

- Analysts expect earnings to reach ₹26.4 billion (and earnings per share of ₹17.12) by about December 2027, up from ₹16.7 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₹31.2 billion in earnings, and the most bearish expecting ₹18.9 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 65.7x on those 2027 earnings, down from 71.2x today. This future PE is greater than the current PE for the IN Hospitality industry at 24.3x.

- Analysts expect the number of shares outstanding to grow by 2.64% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.48%, as per the Simply Wall St company report.

Indian Hotels Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The exceptional accounting gain that bolstered IHCL's profit after tax may not be sustainable, potentially leading to variability in earnings if similar gains are not realized in future quarters. This could impact overall earnings consistency.

- There is a concentration of growth from specific regions and high-end property performance, such as the Taj Mahal Palace & Tower, which could pose a risk if those regions experience a downturn or if demand shifts. This regional dependence may result in uneven revenue streams.

- New businesses showed impressive growth; however, these ventures are in early stages and rely on collaborations and small, experiential formats, which may present scaling challenges and impact revenue reliability if partnerships do not mature as expected.

- A significant portion of expected growth stems from increased wedding bookings and foreign tourism recovery, both of which are susceptible to economic fluctuations or changes in travel trends, potentially leading to variability in revenue projections.

- The plan for international expansion remains capital-light and mainly through management contracts or joint ventures, which can limit IHCL's control over asset quality and strategic direction abroad, possibly affecting international revenue contributions.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹750.14 for Indian Hotels based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹910.0, and the most bearish reporting a price target of just ₹550.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2027, revenues will be ₹119.2 billion, earnings will come to ₹26.4 billion, and it would be trading on a PE ratio of 65.7x, assuming you use a discount rate of 14.5%.

- Given the current share price of ₹836.75, the analyst's price target of ₹750.14 is 11.5% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives