Last Update01 May 25Fair value Increased 0.013%

AnalystConsensusTarget made no meaningful changes to valuation assumptions.

Read more...Key Takeaways

- NIIT's strategic adaptation and market volatility resilience likely favor sustained revenue growth through diversified offerings and operational improvements.

- Expansion into high-demand tech programs and BFSI sector penetration enhances revenue, margin stability, and long-term growth potential.

- Challenging market conditions, ineffective cash utilization, and sector-specific risks could hinder NIIT’s revenue growth and earnings in the immediate future.

Catalysts

About NIIT- Engages in providing learning and knowledge solutions to individuals, enterprises, and various institutions worldwide.

- The broad-basing of NIIT's go-to-market strategy has resulted in a steady recovery in business, suggesting potential for sustained revenue growth as they adapt to market volatility. This is expected to favorably impact revenue growth rates.

- NIIT's expansion into offering advanced technology programs like enterprise architects, cybersecurity, AI, and digital architects positions them to capitalize on the growing demand for tech skills, expected to boost revenues and potentially improve net margins due to higher-value offerings.

- The company’s increased penetration into large private banks in the BFSI sector indicates an opportunity for future growth, anticipated to contribute positively to revenue and margin stability.

- NIIT's investments in shifting fixed costs to variable costs along with reducing headcount indicate an operational strategy to improve net margins, potentially leading to enhanced earnings as revenue stabilizes and grows.

- The company is leveraging growth opportunities presented by AI and Generative AI, which are likely to enhance their educational offerings and differentiation in the market, expected to positively impact revenue and create long-term growth potential.

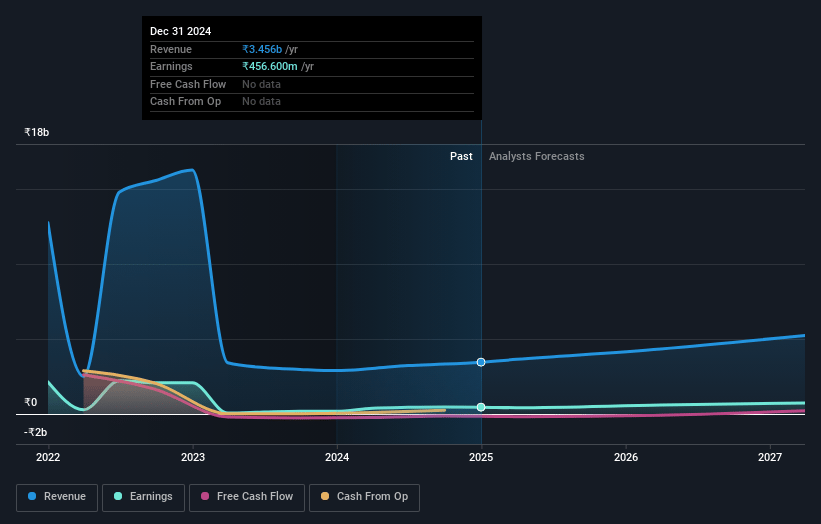

NIIT Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming NIIT's revenue will grow by 19.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 13.2% today to 14.6% in 3 years time.

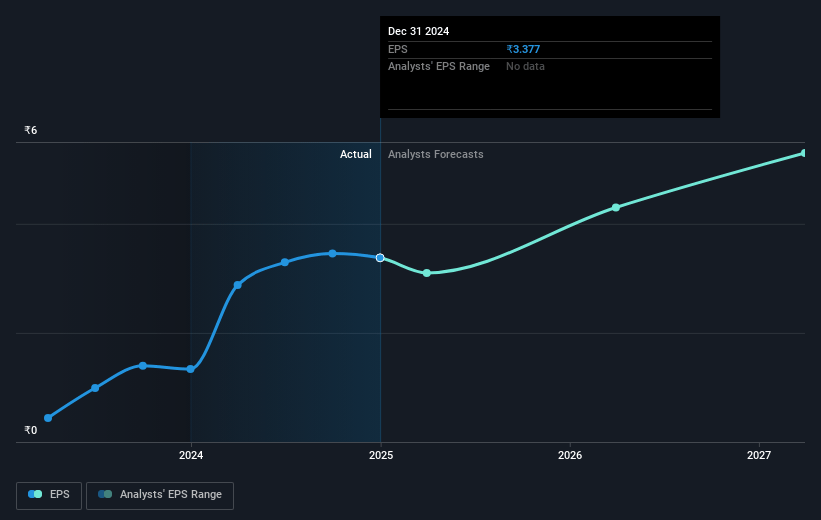

- Analysts expect earnings to reach ₹870.7 million (and earnings per share of ₹6.25) by about May 2028, up from ₹456.6 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 33.8x on those 2028 earnings, down from 38.5x today. This future PE is lower than the current PE for the IN Consumer Services industry at 43.2x.

- Analysts expect the number of shares outstanding to grow by 0.18% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.96%, as per the Simply Wall St company report.

NIIT Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company is experiencing a challenging and volatile environment, with a mix of positive and negative trends in different sectors, which could impact their revenue growth trajectory negatively in the short term.

- Despite having significant cash balances, the company's capability to effectively utilize the cash for growth-driving opportunities such as organic or inorganic investments is not evident, potentially impacting the company’s ability to enhance net margins.

- Lower-than-expected revenue growth in Q3 and forecasts of lower revenues in the coming quarter due to seasonal effects and sector trends (especially in tech and BFSI), indicates a potential risk to consistent earnings growth.

- Potential slowdown in the BFSI sector due to regulatory actions could have a larger impact on revenue in Q4, and a potential delay in the increase in tech hiring could create a net revenue impact, hindering the company's growth targets.

- There is a risk that the expected improvements based on AI and reskilling challenges may not materialize as quickly as planned, which could impact the company's ability to maintain or enhance its revenue growth and earnings amid increasing competition in the edtech market.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹150.0 for NIIT based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹6.0 billion, earnings will come to ₹870.7 million, and it would be trading on a PE ratio of 33.8x, assuming you use a discount rate of 13.0%.

- Given the current share price of ₹129.6, the analyst price target of ₹150.0 is 13.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.