Key Takeaways

- Praj Industries is set to benefit from India's ethanol policy and PLA partnership, boosting potential growth in both domestic and international markets.

- Expansion in bioenergy and new facility operations may enhance revenue diversity, operational margins, and future earnings stability.

- Liquidity challenges and project delays, along with intensified competition and regulatory uncertainties, could pressure revenue, margins, and innovation-driven growth.

Catalysts

About Praj Industries- Operates in the field of bio-based technologies and engineering worldwide.

- India achieving the 20% ethanol blending target ahead of schedule indicates a positive policy environment for bioenergy. Praj Industries is positioned to benefit from future expansion of the ethanol blending program, potentially enhancing domestic revenue growth.

- The partnership with Uhde Inventa-Fischer for PLA production could open new revenue streams for Praj Industries by tapping into the growing demand for bioplastics, thus boosting future revenues and improving operational margins.

- The international bioenergy business is expected to grow given the strong inquiry pipeline and recent contracts in South America. Strengthening presence in the Americas could lead to increased export revenues, diversifying and stabilizing the revenue base.

- The potential for enhanced operating margins through customer solutions such as co-product development and plant yield improvements will likely make existing bioenergy projects more financially viable, increasing client demand and subsequently Praj's earnings.

- The commencement of operations at the Praj GenX facility in Mangalore and its long-term agreements with key customers indicate expected contributions to revenue and profits from FY '26 onward, positively impacting future earnings and net margins.

Praj Industries Future Earnings and Revenue Growth

Assumptions

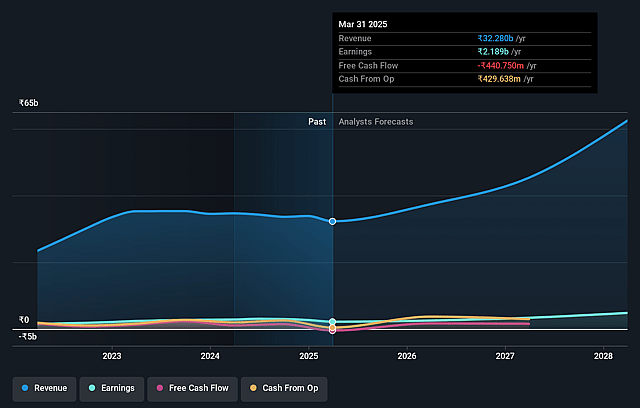

How have these above catalysts been quantified?- Analysts are assuming Praj Industries's revenue will grow by 24.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.8% today to 7.7% in 3 years time.

- Analysts expect earnings to reach ₹4.8 billion (and earnings per share of ₹26.2) by about July 2028, up from ₹2.2 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 33.7x on those 2028 earnings, down from 39.5x today. This future PE is greater than the current PE for the IN Construction industry at 21.0x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.63%, as per the Simply Wall St company report.

Praj Industries Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company is facing liquidity challenges, leading to a delay of almost 12 months in project execution cycles, which could negatively impact revenue recognition and cash flows.

- Although there is a strong inquiry pipeline from international markets, there are still uncertainties regarding the enactment of policies like the 45Z draft notification, which may delay expected revenues from these regions.

- The company's project expenses have increased due to site expenses related to setting up CBG plants, potentially affecting net margins if not managed effectively.

- Competition in the bioenergy industry is intensifying, with new players entering the market, which could result in pressure on pricing and margins, affecting overall earnings.

- The recent fire incident at the company's R&D center, although insured, temporarily disrupted activities and could have residual impacts on ongoing and future research and development output, potentially affecting innovation-driven revenue streams.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹589.0 for Praj Industries based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹700.0, and the most bearish reporting a price target of just ₹493.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹62.5 billion, earnings will come to ₹4.8 billion, and it would be trading on a PE ratio of 33.7x, assuming you use a discount rate of 14.6%.

- Given the current share price of ₹470.2, the analyst price target of ₹589.0 is 20.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.