Narratives are currently in beta

Key Takeaways

- Robust uptake in large orders from core sectors and focus on energy efficiency suggest strong future revenue growth for ABB India.

- Capacity expansion with cost-effective strategies and deeper market penetration enhance net margins and stabilize revenue streams through diversification.

- Larger orders with longer gestation, cyclic market exposure, and intensified competition may drive revenue inconsistency and net margin pressures amidst economic uncertainties.

Catalysts

About ABB India- Develops and sells products and system solutions to utilities, industries, channel partners, and original equipment manufacturers in India and internationally.

- ABB India is seeing a robust uptake in large orders from core sectors, such as data centers and transportation, which suggest future growth in these areas. These large contracts, particularly from high-value-add sectors, are expected to positively impact future revenue generation.

- The company has been expanding its capacity efficiently, leveraging existing facilities with incremental investments rather than large outlays, which is likely to improve net margins by maintaining a cost-effective operational structure.

- There is a strong market outlook from new market segments like semiconductor electronics and packaged food, which are seeing substantial growth. This diversification in economic segments is projected to stabilize and eventually boost revenue streams.

- ABB's focus on energy efficiency and sustainability, combined with its leadership in the energy-efficient motors and drives segment, positions it well for future growth. This focus is expected to enhance earnings by tapping into the increasing demand for sustainable industrial solutions.

- ABB India's strategy of deeper market penetration and expansion of localized production, especially for the Electrification business line, holds promise for improving net margins through cost efficiencies and increasing revenue through market share gains.

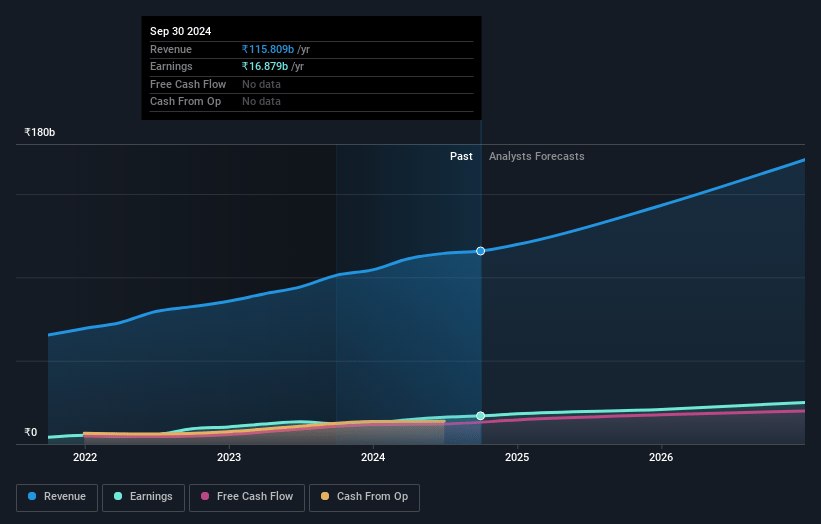

ABB India Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming ABB India's revenue will grow by 15.5% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 14.6% today to 14.3% in 3 years time.

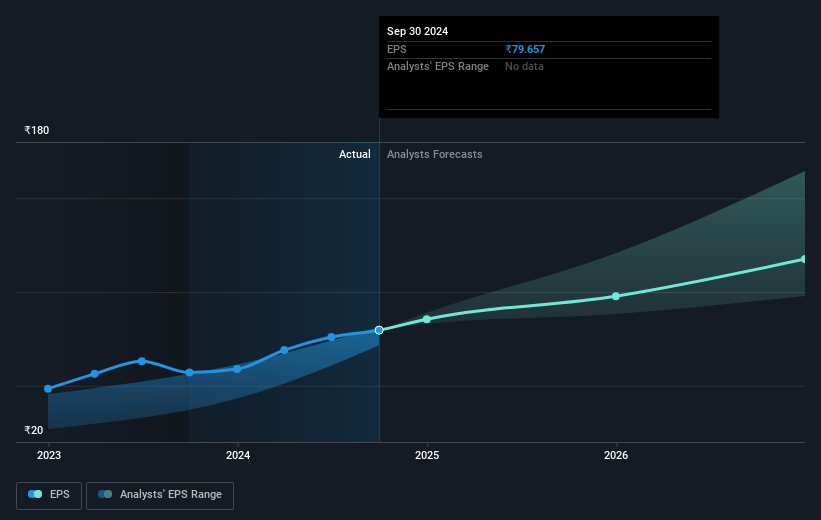

- Analysts expect earnings to reach ₹25.6 billion (and earnings per share of ₹120.69) by about January 2028, up from ₹16.9 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₹34.9 billion in earnings, and the most bearish expecting ₹20.7 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 95.2x on those 2028 earnings, up from 78.8x today. This future PE is greater than the current PE for the IN Electrical industry at 45.7x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.3%, as per the Simply Wall St company report.

ABB India Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The increasing mix of larger orders with longer gestation periods may slow down revenue conversion rates, affecting short-term revenue growth and causing variability in quarterly earnings.

- Exposure to cyclic market segments such as metals and oils, which are currently showing a muted outlook, could lead to variability in order intake and revenue, impacting the consistency of earnings.

- Intensified competition, especially in segments like low-voltage motors, could lead to pricing pressures and margin erosion, potentially affecting net margins.

- The reliance on high-value export allocations and the impact of global economic uncertainty could influence the stability of export revenue streams, thereby affecting total revenue.

- Any delays in government infrastructure projects or private sector CapEx, possibly due to elections or economic conditions, could impact order inflows and result in slower revenue and earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹7728.52 for ABB India based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹9050.0, and the most bearish reporting a price target of just ₹5608.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹178.4 billion, earnings will come to ₹25.6 billion, and it would be trading on a PE ratio of 95.2x, assuming you use a discount rate of 14.3%.

- Given the current share price of ₹6277.4, the analyst's price target of ₹7728.52 is 18.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives