Narratives are currently in beta

Key Takeaways

- Strategic focus on rural demand, government spending, and services exports growth positions HDFC Bank for revenue stream expansion.

- Effective cost management and improved liquidity indicate potential for enhanced net margins and earnings growth as macroeconomic conditions stabilize.

- Macroeconomic challenges and liquidity issues may pressure HDFC Bank's revenue, net margins, and profitability, with potential increased costs from PSL requirements and competition.

Catalysts

About HDFC Bank- Engages in the provision of banking and financial services to individuals and businesses in India, Bahrain, Hong Kong, Singapore, and Dubai.

- HDFC Bank's strategic focus on expanding rural demand, capturing increased government spending, and leveraging services exports growth positions it to potentially boost future revenue streams.

- The bank's ability to manage costs effectively with only a 7% year-on-year increase, despite adding over 1,000 branches, suggests potential to improve net margins through enhanced productivity and cost management.

- Improving liquidity, as evidenced by the deposit growth outpacing loan growth, allows HDFC Bank to maintain comfortable capital levels, which could enhance earnings as macroeconomic conditions stabilize.

- The focus on improving the credit-deposit (CD) ratio and continuing to invest in distribution and technology suggests future revenue growth as it aims to capture market share and expand its loan books when macroeconomic conditions become more favorable.

- HDFC Bank's stable net interest margins (NIMs) and provisioning coverage ratios, coupled with maintaining low slippage rates in a challenging environment, indicate resilience in core earnings performance and potential for future margin expansion.

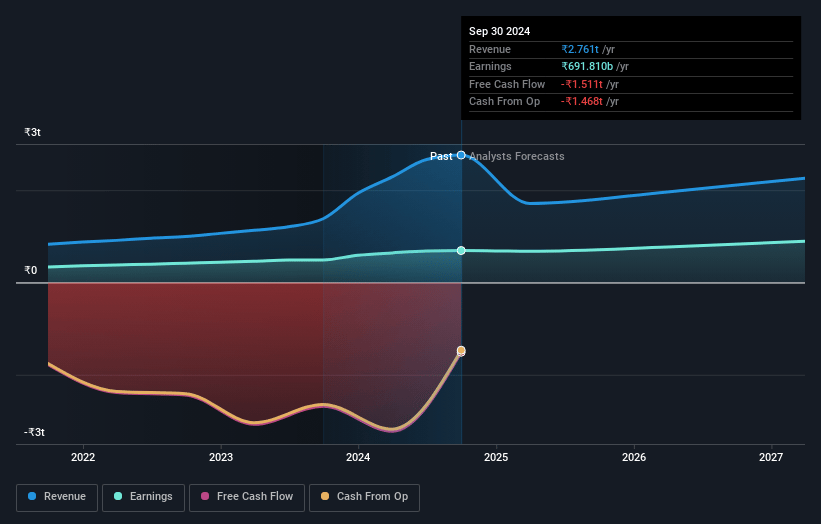

HDFC Bank Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming HDFC Bank's revenue will decrease by -5.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 25.7% today to 40.8% in 3 years time.

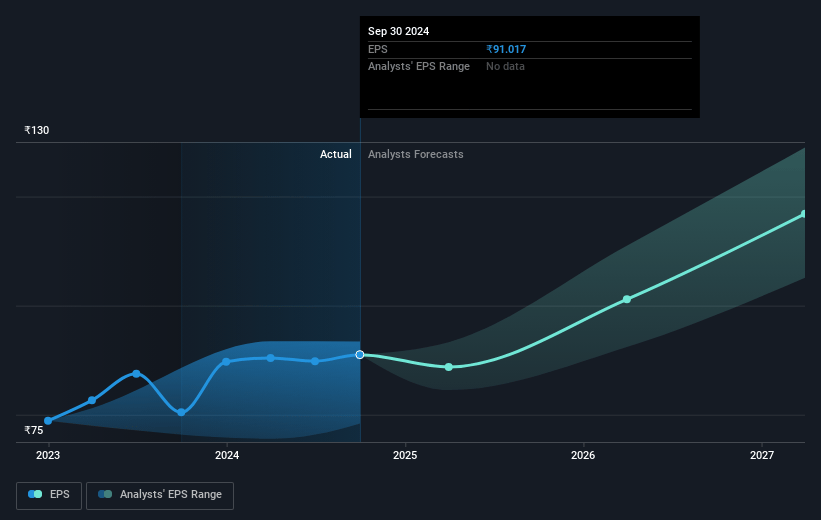

- Analysts expect earnings to reach ₹945.1 billion (and earnings per share of ₹121.16) by about January 2028, up from ₹695.8 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as ₹769.4 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 24.5x on those 2028 earnings, up from 18.4x today. This future PE is greater than the current PE for the US Banks industry at 9.6x.

- Analysts expect the number of shares outstanding to grow by 0.66% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.22%, as per the Simply Wall St company report.

HDFC Bank Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The challenging macroeconomic environment, including tight liquidity conditions, moderating urban demand, depreciation of the Indian rupee, and capital outflows due to geopolitical uncertainties, could negatively impact HDFC Bank's revenue growth and net margins.

- Volatility in private capital expenditure programs suggests potential headwinds for the bank's earnings growth if corporate loan demand does not improve.

- The tight pricing environment resulting from liquidity challenges may pressure the bank's net interest margins, implying potential difficulties in maintaining profitability.

- The ongoing uncertainties in completing priority sector lending (PSL) requirements, especially relating to SMF and weaker section classifications, could lead to increased costs if the bank needs to purchase PSL certificates, impacting the bank's overall earnings.

- The increase in slippages from the agricultural sector and challenges in capturing market opportunities due to aggressive pricing from competitors could lead to higher credit costs and impact the bank's ability to maintain healthy earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹1989.63 for HDFC Bank based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹2550.0, and the most bearish reporting a price target of just ₹1627.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹2318.5 billion, earnings will come to ₹945.1 billion, and it would be trading on a PE ratio of 24.5x, assuming you use a discount rate of 14.2%.

- Given the current share price of ₹1677.3, the analyst's price target of ₹1989.63 is 15.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives