Narratives are currently in beta

Key Takeaways

- Strategic branding and digital enhancements aim to expand retail banking, improve efficiency, and attract more customers for revenue growth.

- Asset quality improvements and optimized funding strategies support margin preservation and sustainable earnings growth.

- Elevated deposit costs, international margin fluctuations, and reliance on recoveries threaten profitability, while slippage in personal loans may impact credit quality and net margins.

Catalysts

About Bank of Baroda- Provides various banking products and services to individuals, government departments, and corporate customers in India and internationally.

- Bank of Baroda's management is focusing on expanding its retail banking presence with strategic branding efforts, including appointing a global brand ambassador. This initiative aims to increase revenue by attracting a larger customer base.

- The bank is concentrating on improving its digital capabilities, including the deployment of AI-driven virtual relationship managers. This digital focus can enhance operational efficiency and potentially boost net margins by reducing costs associated with traditional banking operations.

- Despite current challenges, the bank has strong asset quality metrics, with a reduction in gross NPAs and net NPAs. Continued improvement in asset quality could result in lower provisions and higher net earnings in the future.

- Bank of Baroda is working on optimizing its funding mix by focusing on CASA and retail term deposits while reducing dependency on wholesale deposits. This strategy is likely to contribute to maintaining or improving net interest margins.

- The management has adjusted growth expectations for loans and deposits, aiming for sustainable growth that supports margin preservation. This indicates a focus on earnings stability and margin management, which could drive future earnings growth.

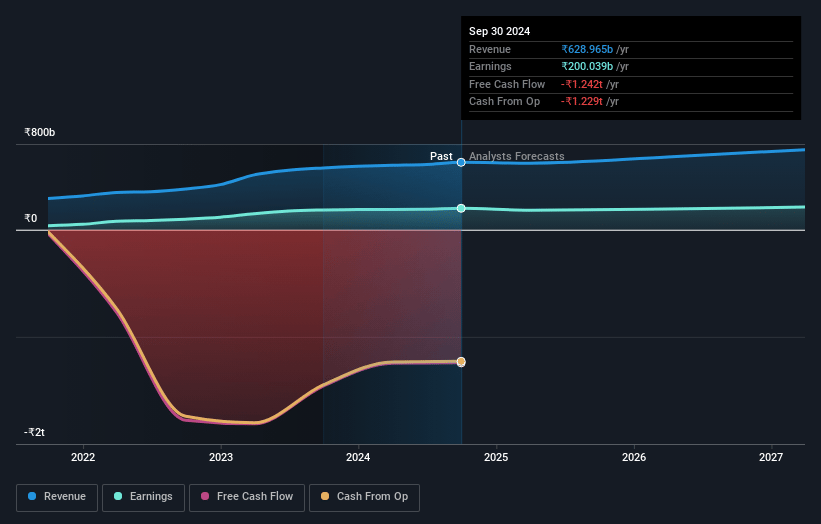

Bank of Baroda Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Bank of Baroda's revenue will grow by 7.8% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 31.8% today to 26.7% in 3 years time.

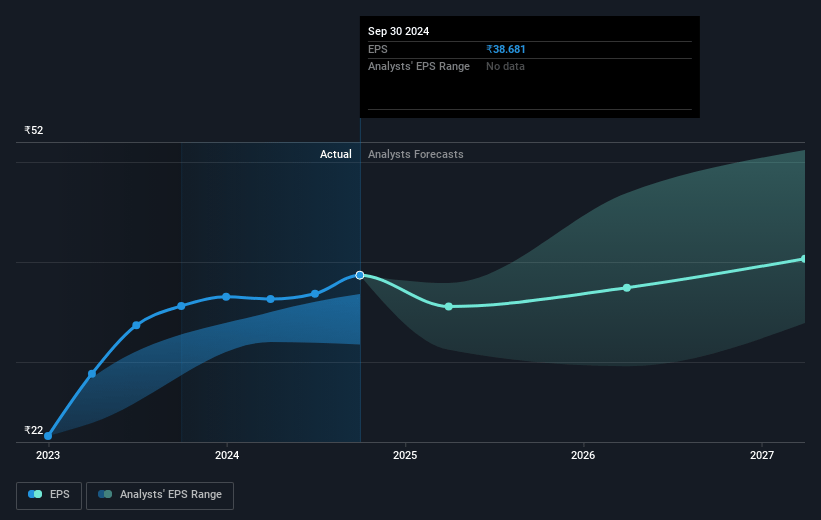

- Analysts expect earnings to reach ₹210.1 billion (and earnings per share of ₹40.37) by about January 2028, up from ₹200.0 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₹265.1 billion in earnings, and the most bearish expecting ₹175.3 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 10.6x on those 2028 earnings, up from 6.2x today. This future PE is lower than the current PE for the IN Banks industry at 12.4x.

- Analysts expect the number of shares outstanding to grow by 0.21% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.15%, as per the Simply Wall St company report.

Bank of Baroda Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The bank's cost of deposits is elevated and any further competition among banks could increase costs, impacting net interest margins and profitability.

- There has been a slight downward revision in the growth guidance for both deposits and advances, from earlier estimates, which might limit revenue growth.

- Fluctuations in the international book's interest margins due to market repricing could pressurize earnings from overseas operations.

- A high reliance on recovery from written-off accounts for a significant portion of income may not be sustainable, impacting future revenue stability if such recoveries shrink.

- Although retail growth is strong, there is a trend of increasing slippage in personal loans, which might impact the credit quality and necessitate higher provisions, affecting net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹287.84 for Bank of Baroda based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹325.0, and the most bearish reporting a price target of just ₹190.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹787.1 billion, earnings will come to ₹210.1 billion, and it would be trading on a PE ratio of 10.6x, assuming you use a discount rate of 14.2%.

- Given the current share price of ₹241.22, the analyst's price target of ₹287.84 is 16.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives