Narratives are currently in beta

Key Takeaways

- Expanding product innovation and international reach is likely to drive revenue growth through a stronger EV market presence and increased market share in Africa.

- Strategic partnerships and investments in R&D aim to diversify offerings and enhance net margins through innovation and cost-sharing.

- Strains from regulatory changes, cost pressures, and international investments could impact TVS Motor's margins, profitability, and revenue growth.

Catalysts

About TVS Motor- Engages in the manufacture and sale of automotive vehicles and components, spare parts, and accessories in India.

- TVS Motor's focus on product innovation, including new product launches like the TVS King EV Max and enhancements to the iQube portfolio, could drive revenue growth by capturing a larger share of the growing EV market.

- Expanding international reach, particularly in Africa and North Africa with the introduction of products like the HLX 125 5-gear, is expected to boost revenue and market share in these regions.

- The strategic partnership with Hyundai focusing on micro mobility solutions presents an opportunity for revenue growth and diversification, potentially improving net margins through collaborative innovation and shared resources.

- Continued investments in R&D and capability building for digital and software enhancements across both ICE and EV models are likely to enhance product offerings, which could result in higher revenue and improved net margins.

- Upcoming recognition of PLI (Production-Linked Incentive) benefits, expected to be realized in Q4, could positively impact earnings by increasing operating margins and boosting profitability.

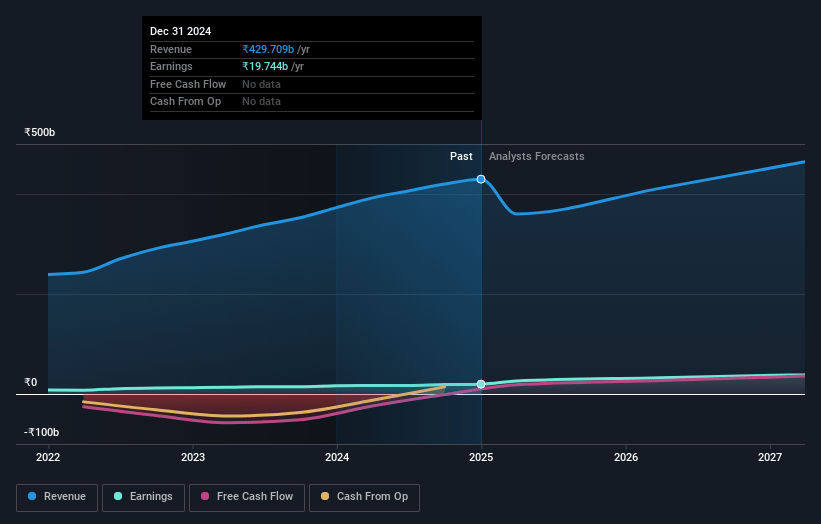

TVS Motor Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming TVS Motor's revenue will grow by 4.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.6% today to 10.6% in 3 years time.

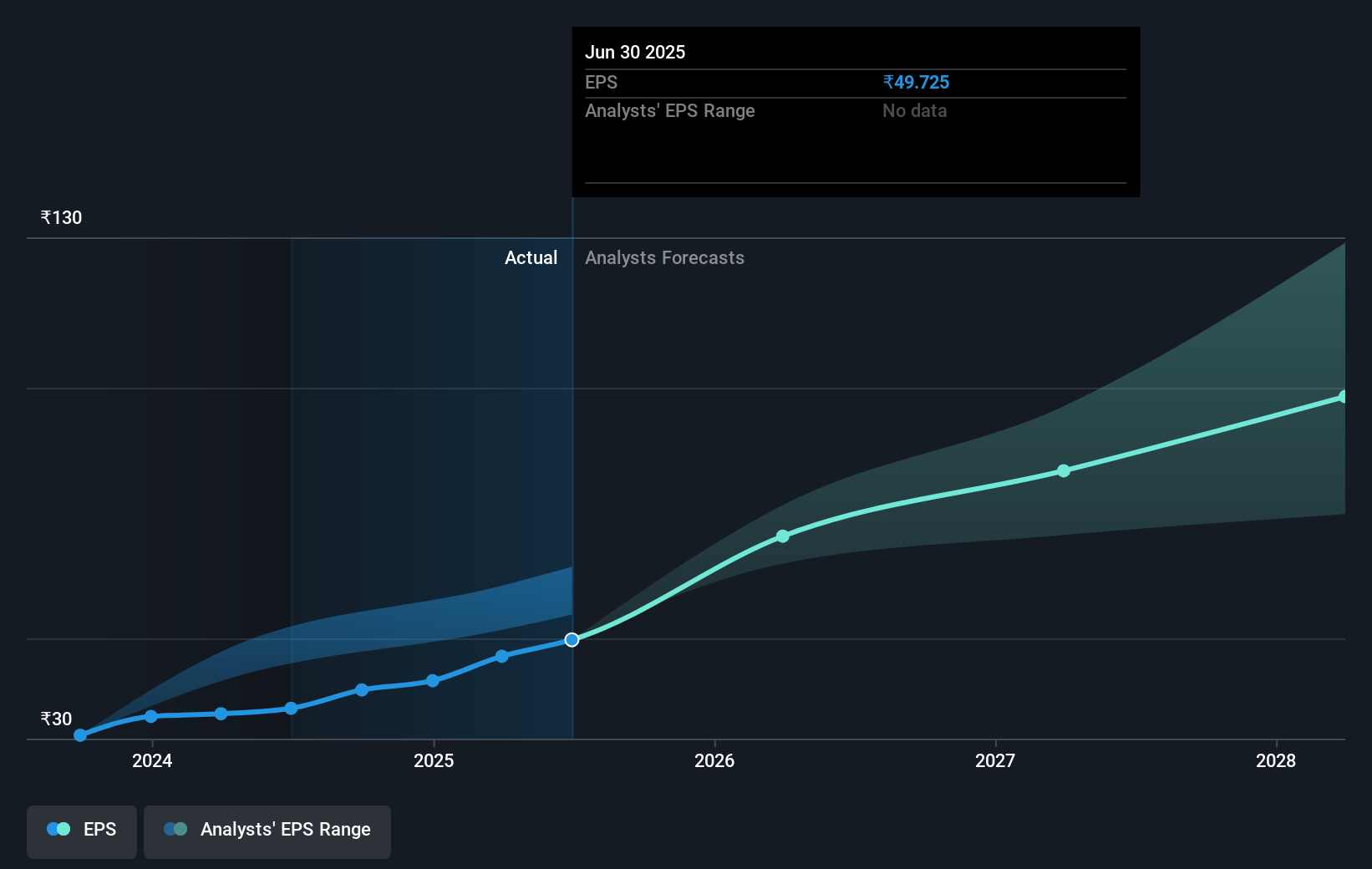

- Analysts expect earnings to reach ₹52.1 billion (and earnings per share of ₹109.57) by about January 2028, up from ₹19.7 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 41.1x on those 2028 earnings, down from 59.4x today. This future PE is greater than the current PE for the IN Auto industry at 29.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 19.8%, as per the Simply Wall St company report.

TVS Motor Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The impending introduction of the OBD2B norms and associated price hikes could pose a strain on pricing strategies and consumer demand, potentially impacting revenue and profit margins.

- Elevated employee and operational costs without corresponding revenue growth may challenge the realization of operating leverage, thereby impacting net margins and profitability.

- The slowdown in AUM growth at TVS Credit, attributed to tightened credit norms, may influence the financial subsidiary’s contribution to overall earnings.

- The industry-wide pressure in the entry-level motorcycle and moped segments might adversely affect sales volumes and revenue growth in these categories.

- Any delays or substantial further investments required in the international ventures and Norton product development could lead to increased operational costs, affecting overall margins and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹2620.43 for TVS Motor based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹3130.0, and the most bearish reporting a price target of just ₹1670.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹489.3 billion, earnings will come to ₹52.1 billion, and it would be trading on a PE ratio of 41.1x, assuming you use a discount rate of 19.8%.

- Given the current share price of ₹2467.2, the analyst's price target of ₹2620.43 is 5.8% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives