Key Takeaways

- TVS Motor's aggressive EV expansion and R&D investments are poised to boost revenue and net margins through product innovation and market capture.

- Strategic geographic diversification in LatAm and Africa is expected to significantly increase international sales, bolstering overall revenue growth.

- Reliance on government incentives and challenges in export markets could risk TVS Motor's profitability, with heavy investments yet to yield free cash flow.

Catalysts

About TVS Motor- Engages in the manufacture and sale of automotive vehicles and components, spare parts, and accessories in India.

- TVS Motor's aggressive expansion in the EV segment, including future product launches and network expansion, is a key catalyst for revenue growth, as they aim to capture a larger share of both domestic and international markets.

- The company's development of the TVS King Max three-wheeler EV signals strong growth potential in sustainable urban mobility, potentially improving revenue and net margins due to expected high demand.

- Strategic geographic diversification, such as expansion in the LatAm and African markets, foresees a substantial increase in international sales, positively impacting overall revenue growth.

- Continuous investment in R&D, technology, and digital transformation is expected to enhance operational efficiency and expand product offerings, likely improving net margins and revenue over time.

- Government incentives like the PLI scheme are anticipated to contribute to financial performance improvements, potentially enhancing EBITDA margins and further supporting earnings growth.

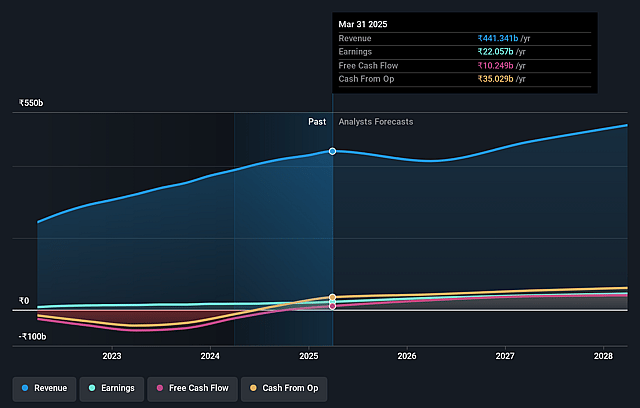

TVS Motor Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming TVS Motor's revenue will grow by 5.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.0% today to 8.8% in 3 years time.

- Analysts expect earnings to reach ₹45.0 billion (and earnings per share of ₹94.12) by about July 2028, up from ₹22.1 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₹56.4 billion in earnings, and the most bearish expecting ₹35.7 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 53.2x on those 2028 earnings, down from 60.4x today. This future PE is greater than the current PE for the IN Auto industry at 30.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 21.14%, as per the Simply Wall St company report.

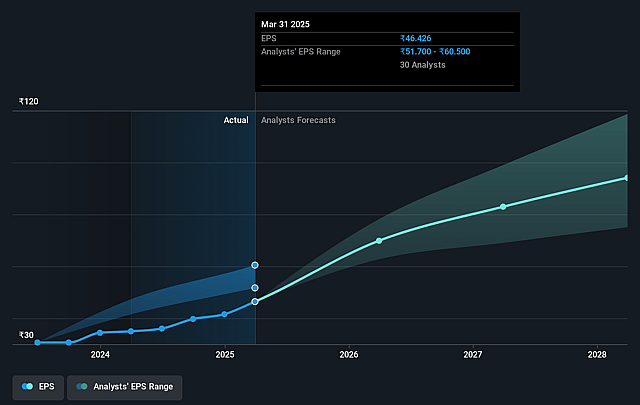

TVS Motor Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The strong growth in EV sales and the high operating EBITDA margin partly rely on government PLI benefits, indicating a potential risk if these incentives are reduced or if regulations change, which could affect future profitability margins.

- Despite achieving record sales and revenue, there was a reported decline in three-wheeler sales compared to the past year, which could signal potential market saturation or increased competition in this segment, potentially impacting revenue growth.

- The company acknowledges geopolitical and economic challenges in key export markets like Africa and the Middle East, including inflation and currency devaluation, which could adversely affect international sales and revenue.

- The company is heavily investing in new technologies and expansions, including significant CapEx and investments in subsidiaries like Norton and TVS Credit, but these are not yet yielding free cash flow, posing a risk of financial strain if returns are delayed or underperform.

- While the company reported positive trends in financing and credit operations, there's mention of tightened credit demand, which may continue to impact consumer purchasing power and, consequently, sales and revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹2837.25 for TVS Motor based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹3300.0, and the most bearish reporting a price target of just ₹1750.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹513.6 billion, earnings will come to ₹45.0 billion, and it would be trading on a PE ratio of 53.2x, assuming you use a discount rate of 21.1%.

- Given the current share price of ₹2802.65, the analyst price target of ₹2837.25 is 1.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.