Last Update 21 Aug 25

Fair value Increased 8.85%Despite a sharp decline in consensus revenue growth forecasts and a substantial jump in future P/E, analysts have raised Genscript Biotech's fair value estimate from HK$21.61 to HK$23.01.

What's in the News

- GenScript Biotech launched a new global brand platform, "Scripting Possibilities," alongside a refreshed visual identity and expanded marketing initiatives to drive growth and strengthen global brand presence.

- A board meeting is scheduled to review and approve interim results for H1 2025, with potential consideration of an interim dividend.

- The company provided earnings guidance expecting a substantial increase in H1 2025 pre-tax profit, primarily driven by a surge in license revenue from LaNova Medicines, and a significant decrease in non-cash fair value losses related to ProBio.

- ProBio, a GenScript subsidiary, received approximately USD 213.8 million in payments under the R&A Agreement, bolstering cash reserves and core competencies.

- Newly presented data from the CARTITUDE-1 and CARTITUDE-4 studies demonstrated long-term efficacy of CARVYKTI® in multiple myeloma and promising results from early-phase solid tumor trials, showcased at the 2025 ASCO Annual Meeting.

Valuation Changes

Summary of Valuation Changes for Genscript Biotech

- The Consensus Analyst Price Target has risen from HK$21.61 to HK$23.01.

- The Future P/E for Genscript Biotech has significantly risen from 21.35x to 154.54x.

- The Consensus Revenue Growth forecasts for Genscript Biotech has significantly fallen from 15.0% per annum to 4.4% per annum.

Key Takeaways

- Investments in automation, proprietary technology, and global expansion are positioning GenScript for increased market share, efficiency, and margin improvement in the life sciences sector.

- Innovative product launches and expanded regulatory compliance are supporting revenue diversification, pricing power, and long-term growth outside the China market.

- Intense competition, reliance on high-growth subsidiaries, and geopolitical and technological shifts threaten margins, revenue reliability, and the ongoing relevance of core service offerings.

Catalysts

About Genscript Biotech- An investment holding company, engages in the manufacture and sale of life science research products and services in the United States of America, Europe, Mainland China, Europe, Asia Pacific, and internationally.

- GenScript is capitalizing on the rapid expansion in biologics and cell/gene therapy demand by investing in automation, proprietary platforms, and global capacity, positioning the company for sustained revenue growth and market share gains as industry R&D cycles accelerate and outsourcing increases.

- Globalization initiatives, including expanded facilities in the US, Singapore, and Europe as well as enhanced regulatory compliance and robust data/IP protection, are enabling deeper penetration in high-growth ex-China markets-supporting long-term revenue diversification and potential margin improvement.

- The CARVYKTI launch by Legend Biotech (GenScript's major subsidiary) is exceeding industry expectations, with operational breakeven and group-level profitability targeted by 2026, which is likely to drive higher equity income and improve GenScript's net margins and overall earnings trajectory.

- Automation and digital transformation-including AI-driven lights-out manufacturing, streamlined CMC platforms, and platform integration-are expected to yield significant cost reductions, efficiency gains, and margin expansion as these investments scale across the company's global operations.

- Breakthrough innovation and pipeline momentum (e.g., launch of best-in-class enzymes, new amylases, express CMC services, and next-gen cell/gene therapy CDMO offerings) are creating high-value, differentiated products and services, supporting stronger pricing power and enhancing both top-line revenue and future profitability.

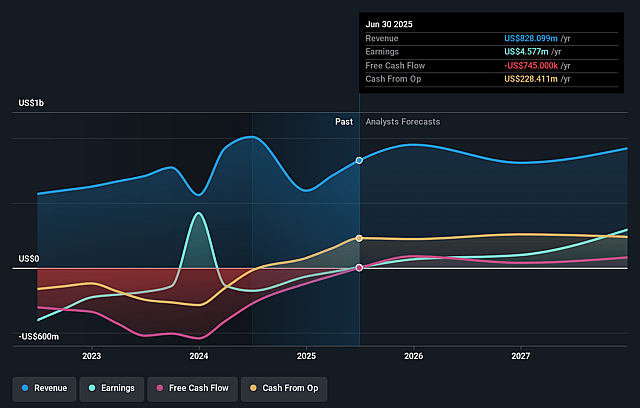

Genscript Biotech Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Genscript Biotech's revenue will grow by 4.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 0.6% today to 39.9% in 3 years time.

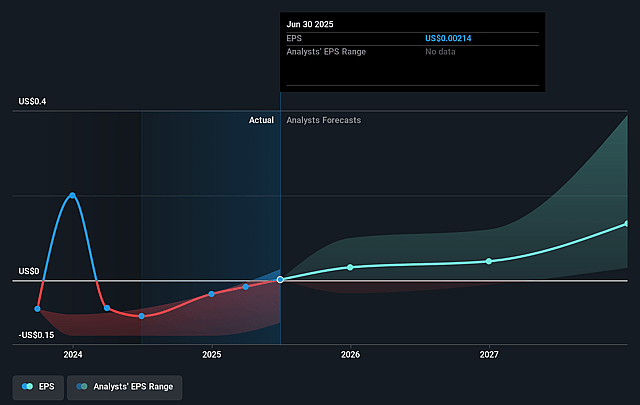

- Analysts expect earnings to reach $376.0 million (and earnings per share of $0.13) by about September 2028, up from $4.6 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $849.7 million in earnings, and the most bearish expecting $67.8 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 23.4x on those 2028 earnings, down from 1059.0x today. This future PE is lower than the current PE for the HK Life Sciences industry at 49.1x.

- Analysts expect the number of shares outstanding to grow by 2.43% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.54%, as per the Simply Wall St company report.

Genscript Biotech Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Intensifying global competition and commodity-style pricing pressures in gene synthesis, protein engineering, and CRO/CDMO services pose a risk to long-term gross margins, which could limit future profitability as noted by ongoing market mix changes and margin fluctuations.

- Substantial and increasing R&D and capacity expansion expenses-especially across new facilities (e.g., the Hopewell site in the U.S.) and product innovation-may not fully translate into scalable commercial products, potentially compressing net margins if growth investments outpace revenue growth.

- Heightened geopolitical risks-including rising global protectionism and potential regulatory tightening on cross-border biotech collaboration-could restrict international contract wins and create operational uncertainty, which would threaten revenue stability and increase compliance costs.

- Heavy dependence on high-growth subsidiaries (notably Legend Biotech and key CDMO platforms) exposes the company to concentration risks-any underperformance, regulatory delays, or increased competition in these areas could adversely impact consolidated earnings and revenue reliability.

- Rapid advancements in automation and AI-driven drug discovery have the potential to render some traditional service offerings less competitive or obsolete, risking reduced client retention and future revenue streams if GenScript fails to continuously differentiate and upgrade its platforms.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of HK$23.522 for Genscript Biotech based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of HK$26.21, and the most bearish reporting a price target of just HK$21.47.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $943.5 million, earnings will come to $376.0 million, and it would be trading on a PE ratio of 23.4x, assuming you use a discount rate of 7.5%.

- Given the current share price of HK$17.34, the analyst price target of HK$23.52 is 26.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.