Narratives are currently in beta

Key Takeaways

- Enhanced rig utilization and high daily rate expansion in Brazil and Saudi Arabia will increase revenue and margins.

- R&D investment in self-developed equipment and strategic internationalization will drive revenue and profit growth.

- Exchange rate volatility, reduced rig utilization, reliance on high-cost imports, competitive international projects, and oil price fluctuations threaten COSL's revenue stability and margins.

Catalysts

About China Oilfield Services- Provides integrated oilfield services in China, Indonesia, Mexico, Norway, Rest of Middle East, and internationally.

- COSL plans to enhance utilization rates of semi-submersible rigs by overcoming current weather-related disruptions and repositioning rigs from unused to active areas such as Brazil and Saudi Arabia. This improvement will likely increase both revenues and earnings.

- The company is expanding its high daily rate operations, with projects set to begin in the North Sea and planned utilization of rigs in Brazil, potentially boosting revenue and profit margins across markets.

- Continuous investment in research and development to innovate and replace high-cost imported equipment with self-developed solutions is expected to drive growth in revenue, profit, and value creation.

- The ongoing bidding and contracting processes for rigs, particularly in high-growth regions like Southeast Asia and Saudi Arabia, indicate increased future utilization and revenue streams.

- COSL's internationalization strategy, coupled with industry stabilization and growth projections, suggests that their overseas margins, revenue, and profits will see a positive uptrend, particularly in regions like Norway and Brazil.

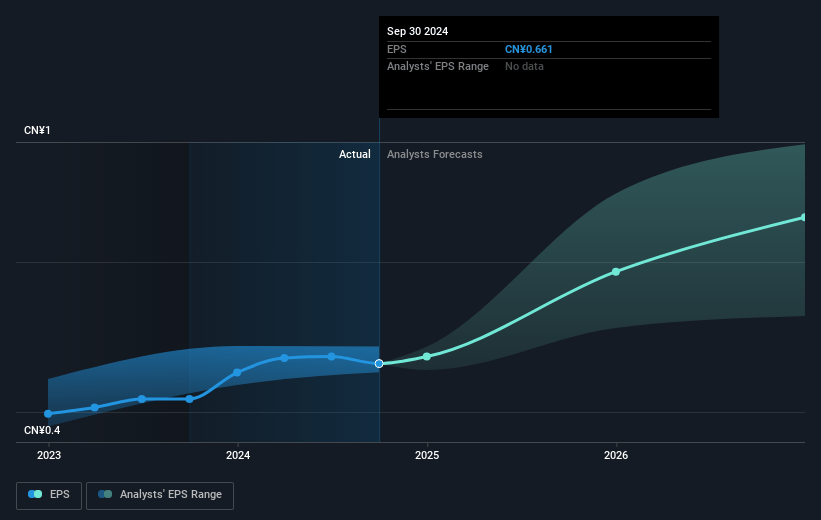

China Oilfield Services Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming China Oilfield Services's revenue will grow by 7.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.6% today to 10.9% in 3 years time.

- Analysts expect earnings to reach CN¥6.5 billion (and earnings per share of CN¥1.39) by about January 2028, up from CN¥3.2 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as CN¥3.9 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 9.3x on those 2028 earnings, down from 9.9x today. This future PE is lower than the current PE for the HK Energy Services industry at 16.1x.

- Analysts expect the number of shares outstanding to decline by 0.39% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.48%, as per the Simply Wall St company report.

China Oilfield Services Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Exchange rate fluctuations, particularly between the Chinese yuan and the US dollar, have negatively impacted COSL's financials, resulting in a CN¥200 million loss in Q3. This could continue to affect revenue and profit margins if exchange rates remain volatile.

- The temporary reduction in the utilization rate of semi-submersible rigs, due to factors like weather conditions and operational changes (e.g., moving operations to Brazil or not yet operational rigs in Norway), could reduce overall revenues and operational efficiencies.

- Continued reliance on high-cost imported equipment, despite efforts to replace them with more cost-effective alternatives, may affect net margins if not managed well due to high capital expenditure on technology upgrades and R&D.

- Despite successful bids and contracts, the competitive and fluctuating nature of international projects, which often require participation in open bidding, poses a risk to revenue stability and future growth, especially if contracts do not guarantee workload or price protection.

- Variability in oil prices and market conditions, particularly in key overseas markets like Norway and Saudi Arabia, could impact both revenues and cost structures, affecting the company's ability to achieve stable gross margins in the long-term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CN¥9.82 for China Oilfield Services based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CN¥14.46, and the most bearish reporting a price target of just CN¥7.43.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CN¥60.2 billion, earnings will come to CN¥6.5 billion, and it would be trading on a PE ratio of 9.3x, assuming you use a discount rate of 9.5%.

- Given the current share price of CN¥7.04, the analyst's price target of CN¥9.82 is 28.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives