Key Takeaways

- Wealth concentration in top cities and secular health trends drive sustained growth in premium beauty and medical aesthetic services, supporting higher margins and market expansion.

- Digital innovation, high membership-based recurring revenue, and successful M&A integration underpin scalable growth, cost efficiency, and predictable cash flows.

- Reliance on urban locations, physical stores, and a limited brand portfolio exposes the company to economic shifts, digital disruption, integration risks, and aggressive competition.

Catalysts

About Beauty Farm Medical and Health Industry- Beauty Farm Medical and Health Industry Inc.

- Structural urban wealth concentration and the ongoing growth of high-net-worth, health-conscious female consumers in China's top-tier cities provide a robust, expanding customer base for premium beauty, wellness, and medical aesthetic services, supporting sustained increases in foot traffic and revenue per store.

- Secular shifts toward holistic health, anti-aging, and preventative care-driven by a rising, aging population-are accelerating demand for higher-margin medical aesthetic and "subhealth" medical services, fueling cross-selling, increased average transaction values, and net margin expansion.

- Digital innovation, particularly via AI-driven diagnostics and data-informed service customization, is improving customer acquisition efficiency, lowering operating costs, and enhancing the scalability of both core and acquired brands, contributing to future EBITDA and margin gains.

- Industry consolidation and Beauty Farm's proven M&A integration capabilities (evident in Naturade's rapid post-acquisition margin uplift) position the company to gain further market share, benefit from scale effects, and maintain strong pricing power-supporting robust long-term revenue and profit growth.

- High recurring revenues and resilient membership-based business (with 91% of revenue from repeat customers and rising per-member spending) drive predictable cash flows and profitability, underpinning both future dividend capacity and capital allocation flexibility.

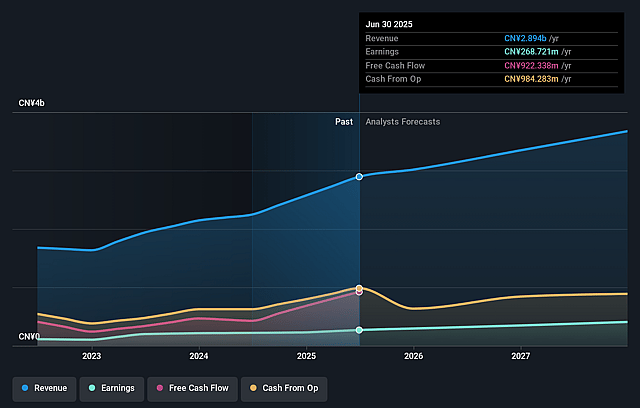

Beauty Farm Medical and Health Industry Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Beauty Farm Medical and Health Industry's revenue will grow by 9.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.3% today to 11.8% in 3 years time.

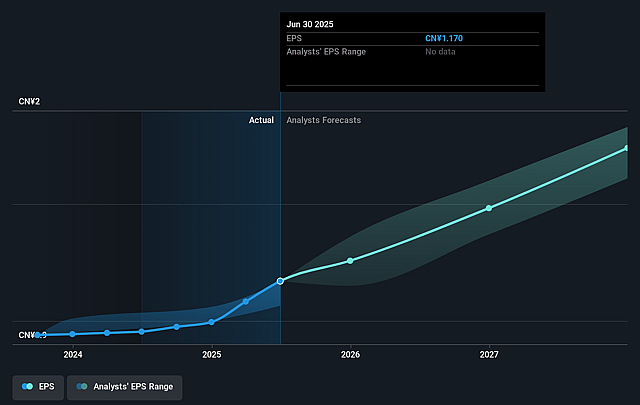

- Analysts expect earnings to reach CN¥448.6 million (and earnings per share of CN¥1.76) by about September 2028, up from CN¥268.7 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 21.0x on those 2028 earnings, down from 28.3x today. This future PE is greater than the current PE for the HK Consumer Services industry at 7.1x.

- Analysts expect the number of shares outstanding to decline by 2.62% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.43%, as per the Simply Wall St company report.

Beauty Farm Medical and Health Industry Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Heavy geographic concentration in Tier 1 cities (Beijing, Shanghai, Guangzhou, Shenzhen) increases dependency on the spending power and economic stability of urban high-net-worth consumers, heightening vulnerability to local economic slowdowns, policy shifts, or demographic changes that could reduce traffic, impacting revenue growth and earnings.

- The company's business relies upon in-person, service-based brick-and-mortar locations, while accelerating digitalization and rise of AI-powered home beauty devices may gradually erode demand for physical store visits, threatening same-store sales, utilization rates, and longer-term revenue stability.

- Continued rapid expansion via acquisitions and dense physical store rollouts increases operational complexity and exposes Beauty Farm to risks of integration execution failures, underperforming assets, or rising fixed costs, all of which could compress margins or dilute net profits during periods when organic growth slows.

- Lack of substantial international diversification and an over-reliance on the flagship Beauty Farm and a small number of premium brands makes the company sensitive to shifts in customer taste, negative publicity, or regulatory scrutiny targeting aesthetic medical or wellness services, posing risks to market share and recurring revenues.

- Intensifying competition in the beauty, wellness, and medical aesthetic industry-both from local boutique providers and international entrants-could drive down service prices and elevate labor costs, as well as prompt higher marketing spend for member retention, putting pressure on gross margins and EBITDA over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of HK$38.179 for Beauty Farm Medical and Health Industry based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CN¥3.8 billion, earnings will come to CN¥448.6 million, and it would be trading on a PE ratio of 21.0x, assuming you use a discount rate of 7.4%.

- Given the current share price of HK$35.26, the analyst price target of HK$38.18 is 7.6% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.