Last Update 17 Dec 25

TEP: Increased Interim Dividend Will Support Attractive Future Shareholder Returns

Analysts have nudged their price target on Telecom Plus modestly higher to reflect steady expectations for fair value, discount rates, and long term profitability, while confirming that the shares remain appropriately valued against projected growth and earnings multiples.

What's in the News

- Proposed increase to the interim dividend to 38 pence per share for the six months ended 30 September 2025, up from 37 pence in H1 FY25 (Company announcement)

- Dividend scheduled to be paid on 19 December 2025 to shareholders on the register as of 5 December 2025 (Company announcement)

- Shares to trade ex dividend on 4 December 2025, setting the cutoff date for eligibility for the increased interim payout (Company announcement)

Valuation Changes

- Fair Value Estimate, unchanged at £23.48 per share, indicating no revision to the intrinsic value assessment.

- Discount Rate, steady at 7.07 percent, reflecting an unchanged view of the company’s risk profile and cost of capital.

- Revenue Growth, effectively unchanged at approximately 6.54 percent, with only immaterial rounding differences versus prior assumptions.

- Net Profit Margin, effectively flat at around 4.60 percent, with no meaningful adjustment to long term profitability expectations.

- Future P/E, maintained at about 22.0 times earnings, signalling a stable view of Telecom Plus’s forward valuation multiple.

Key Takeaways

- Telecom Plus's multiservice model and innovation in product offerings aim to drive customer growth and enhance EBITDA per customer.

- Focusing on AI-driven efficiency and disciplined capital policy supports operating margins and earnings stability, appealing to income-focused investors.

- Telecom Plus faces revenue growth challenges due to competition, energy price volatility, rising costs, service bundling changes, and increasing industry bad debts.

Catalysts

About Telecom Plus- Engages in the provision of utility services in the United Kingdom.

- Telecom Plus is focused on achieving double-digit growth, primarily via their unique multiservice business model and partner route to market, aiming to increase customer numbers by 10% to 15% annually. This is expected to enhance revenue.

- The company is investing in enhancing its product offerings, including launching energy-efficient EV tariffs and ultrafast broadband, alongside reintroducing its insurance products. This diversification is likely to improve EBITDA per customer and overall earnings.

- Telecom Plus is implementing AI and technology-driven efficiency improvements, expected to reduce administrative costs and improve operating margins, positively impacting net margins.

- A strategic focus on growing market share in sectors where they currently hold a smaller share, like insurance, shows potential for substantial revenue growth through diversification.

- Despite operational expansions, the company maintains a disciplined capital allocation policy, focusing on dividend growth. This financial prudence is likely to improve earnings stability and appeal to income-focused investors.

Telecom Plus Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Telecom Plus's revenue will grow by 7.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 4.1% today to 4.8% in 3 years time.

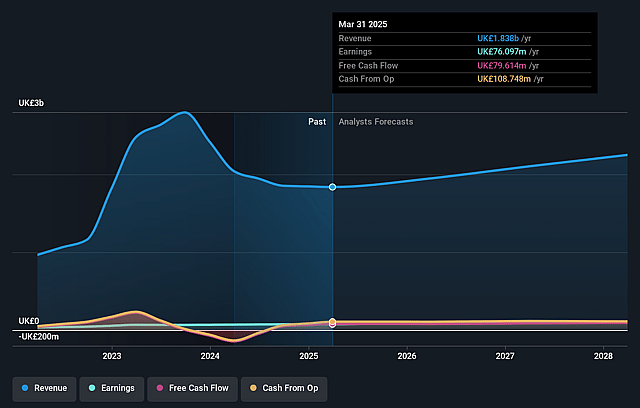

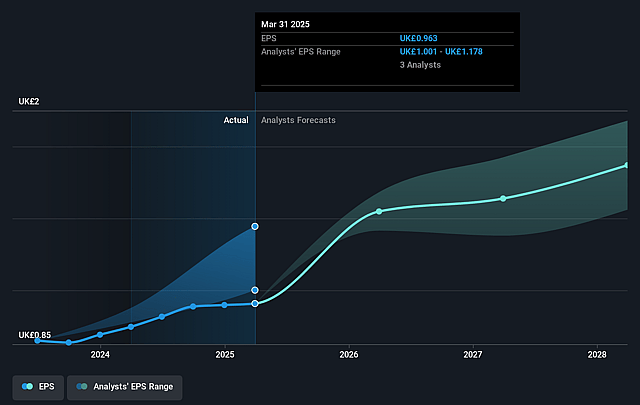

- Analysts expect earnings to reach £108.7 million (and earnings per share of £1.35) by about September 2028, up from £76.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 23.2x on those 2028 earnings, up from 18.9x today. This future PE is greater than the current PE for the GB Integrated Utilities industry at 18.4x.

- Analysts expect the number of shares outstanding to grow by 0.67% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.82%, as per the Simply Wall St company report.

Telecom Plus Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Heightened competition in the energy market, with major suppliers actively seeking new customers and engaging in extensive advertising, may challenge Telecom Plus's ability to sustain its customer growth and maintain market share, potentially impacting revenue growth.

- The impact of energy price volatility, particularly the significant fall in energy prices, has affected profit growth, which was smaller relative to customer growth. Ongoing price fluctuations could continue to affect revenue and profitability.

- Temporary pauses in insurance sales and changes in customer preferences for service bundles have led to slower service growth relative to customer growth, which could hinder future revenue growth and diversification efforts.

- Rising admin costs per customer and the need for continued investments in technology and AI to enhance efficiency and customer service expose the company to margin pressures and increased operating expenses, which could affect net margins and overall profitability.

- Increasing bad debt levels across the industry, coupled with the challenge of maintaining high-quality customer service while reducing admin costs, pose risks to earnings and cash flow, potentially influencing Telecom Plus's financial stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of £25.537 for Telecom Plus based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be £2.3 billion, earnings will come to £108.7 million, and it would be trading on a PE ratio of 23.2x, assuming you use a discount rate of 6.8%.

- Given the current share price of £18.06, the analyst price target of £25.54 is 29.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Telecom Plus?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.