Last Update 15 Dec 25

Fair value Increased 1.19%HLMA: Raised Price Views Will Likely Sustain Premium Multiple Amid Mixed Sentiment

The analyst price target for Halma has been nudged higher, with our updated fair value estimate rising from about £36.67 to £37.11 per share. Analysts highlight a richer future earnings multiple supported by a series of upward target revisions across the Street, despite slightly softer long term growth and margin assumptions.

Analyst Commentary

Recent target hikes across the Street reinforce the view that Halma can sustain a premium valuation, even as near term ratings remain mixed. Bullish analysts argue that stronger pricing power, resilient end market demand, and disciplined capital allocation support higher fair value estimates, while more cautious voices point to already elevated multiples and execution risk in delivering the growth implied by the new targets.

Bullish Takeaways

- Bullish analysts see the cluster of price target increases, including moves into the mid 3,000 GBp range and above, as validation that Halma can justify a richer earnings multiple versus the broader industrial peer set.

- Upward revisions are framed around confidence in the company's ability to compound earnings through acquisitions and organic growth, supporting a long runway for double digit total shareholder returns.

- Optimistic views emphasize Halma's defensive characteristics, with diversified safety and environmental exposure helping to underpin visibility on margins and cash generation that supports premium pricing.

- Where ratings skew more positive, the case centers on execution track record and the belief that incremental operational efficiencies can offset slightly softer long term growth assumptions embedded in some models.

Bearish Takeaways

- Bearish analysts acknowledge the higher targets but retain more neutral stances, arguing that the shares already discount much of the long term growth story, leaving limited valuation upside in the near term.

- Cautious views highlight that even with raised targets, recommendations such as Hold or Neutral signal concern that multiples are stretched relative to Halma's historical range and global industrial benchmarks.

- Some skeptics question whether the company can consistently deliver the margin expansion and acquisition synergies implied in the revised fair value estimates, especially amid a more uncertain macro backdrop.

- There is also focus on execution risk around capital deployment, with concerns that overpaying for deals or slower integration could undermine the growth and returns underpinning current target levels.

Valuation Changes

- Fair Value: risen slightly from approximately £36.67 to £37.11 per share, reflecting a modest uplift in the intrinsic value estimate.

- Discount Rate: edged up marginally from about 8.85 percent to 8.86 percent, indicating a very small increase in the implied cost of capital.

- Revenue Growth: fallen slightly from around 7.53 percent to 7.48 percent, signaling a minor tempering of long term top line expectations.

- Net Profit Margin: declined modestly from roughly 15.62 percent to 15.17 percent, suggesting somewhat more conservative profitability assumptions.

- Future P/E: risen slightly from about 38.1x to 39.7x, implying a modestly richer earnings multiple applied to Halma's projected profits.

Key Takeaways

- Strong cash generation and balance sheet support significant R&D and acquisition investments, ensuring sustainable growth and increased future revenues and earnings.

- Focus on niche markets and talent investment boosts high margins and long-term growth potential, enhancing future profit margins and earnings.

- Geopolitical instability, currency impact, and reliance on M&A and niche markets may challenge Halma's revenue, profit margins, and financial flexibility.

Catalysts

About Halma- Together its subsidiaries, provides technology solutions in the safety, health, and environmental markets in the United States, Mainland Europe, the United Kingdom, the Asia Pacific, Africa, the Middle East, and internationally.

- Continued strong cash generation and a healthy balance sheet have enabled substantial investments in R&D and acquisitions, ensuring sustainable future growth, which is likely to drive up revenues and earnings.

- Acquisitions and a robust M&A pipeline spanning all sectors are contributing to EBIT growth and are expected to enhance future profit margins and earnings growth.

- Organic revenue growth supported by price increases and strong demand ensures maintained high gross margins and potentially improved earnings.

- Investment in talent and collaborative culture across a diverse portfolio positions Halma for consistent growth, enhancing long-term earnings potential.

- Focus on high-value niche markets with strong, long-term growth drivers supports high margins and returns on invested capital, suggesting an increase in future net margins and earnings.

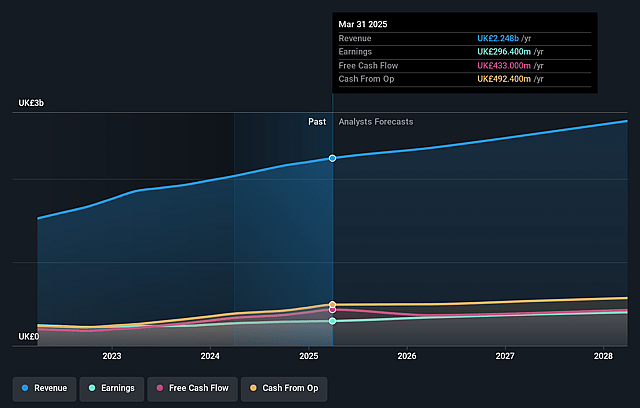

Halma Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Halma's revenue will grow by 6.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 13.2% today to 14.7% in 3 years time.

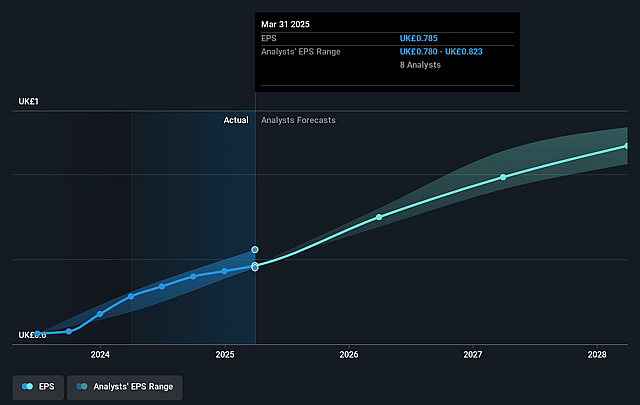

- Analysts expect earnings to reach £397.1 million (and earnings per share of £1.07) by about September 2028, up from £296.4 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 39.2x on those 2028 earnings, down from 41.1x today. This future PE is greater than the current PE for the GB Electronic industry at 29.1x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.45%, as per the Simply Wall St company report.

Halma Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The ongoing geopolitical and economic volatility, along with an adverse currency movement impacting revenue growth, presents a risk that could limit Halma's financial performance. This currency drag, specifically the strengthening of sterling, has been noted as a headwind (revenue impact).

- The decline in the Healthcare sector, notably in eye health therapeutics due to delays in OEM product launches and destocking, offsets growth in other areas and could strain profit margins if not rectified promptly (net margin and revenue impact).

- The strategy of continuous M&A could present risks, especially if integration challenges arise or if acquired companies underperform. Recently acquired businesses, despite contributing to growth, sometimes require additional investment, affecting short-term profitability (earnings impact).

- The reliance on high-margin niche markets and regulated industries means any shifts in regulatory policies or changes in market conditions could impact revenue streams and the overall margin performance, particularly if robustness in sustainability diminishes (net margins and revenue impact).

- While current cash generation and dividend growth are strong, any shift in interest rates or economic conditions affecting cash conversion rates could challenge Halma's financial flexibility and ability to sustain high reinvestment and acquisition activities (cash flow and earnings impact).

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of £32.388 for Halma based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £37.4, and the most bearish reporting a price target of just £24.9.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be £2.7 billion, earnings will come to £397.1 million, and it would be trading on a PE ratio of 39.2x, assuming you use a discount rate of 8.4%.

- Given the current share price of £32.28, the analyst price target of £32.39 is 0.3% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Halma?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.