Key Takeaways

- Expansion into the Australian market aims to boost revenue and EBITDA through strategic acquisitions and synergies.

- Improvement in customer engagement and service delivery is expected to enhance client retention and increase sales.

- Market investigation uncertainty, UK cost pressures, staffing shortages, and increased debt leverage present risks to revenue, margins, and future investments.

Catalysts

About CVS Group- Engages in veterinary, pet crematoria, online pharmacy, and retail businesses.

- CVS Group's entry into the Australian veterinary services market with 27 practices indicates a new geographic growth area, expected to bolster revenue and contribute to EBITDA growth due to lower acquisition multiples and synergies realized earlier than anticipated.

- The redesign and strategic improvements of the Animed Direct website, including enhancements such as guest checkout and Apple Pay, are anticipated to improve the customer experience, thereby potentially increasing online sales volumes and positively impacting revenue.

- Continued focus on recruiting and retaining veterinary staff in the U.K., with a 3% organic increase in the number of vets, aims to replace locums with employed vets, which could enhance net margins by reducing staffing costs and increasing service quality and productivity.

- Adoption of a more comprehensive customer engagement strategy with the implementation of online booking and improved practice websites are expected to increase client retention and satisfaction, contributing to overall revenue growth.

- The expansion and adaptation of clinical practices in Australia, which focus on preventative health care as learned from local clinical advisory committees, could enhance the quality of care and attract more customers, thus having a positive future impact on revenue and earnings.

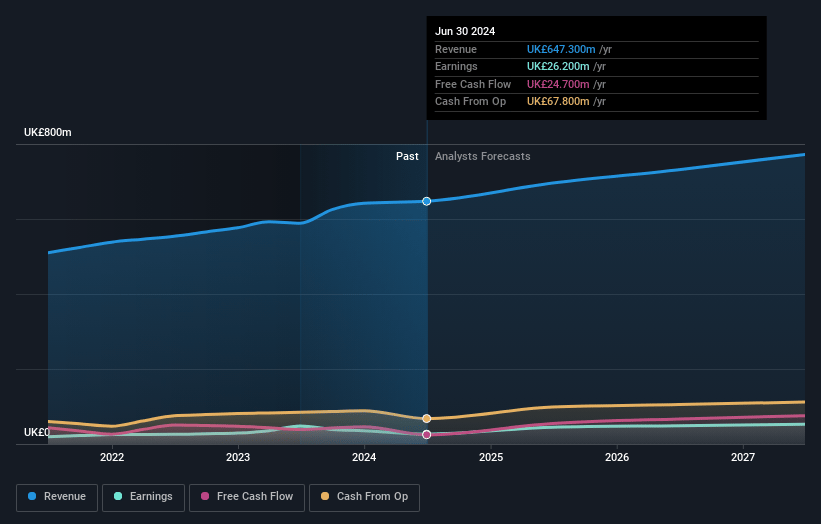

CVS Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming CVS Group's revenue will grow by 5.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.9% today to 6.4% in 3 years time.

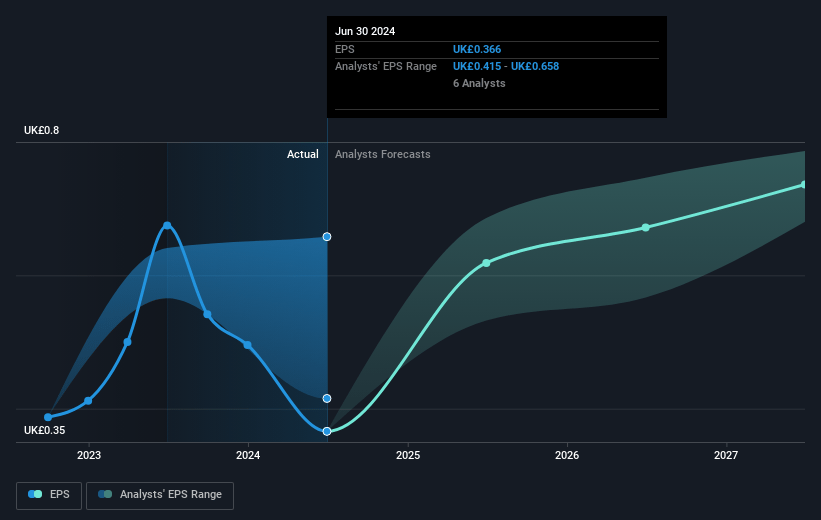

- Analysts expect earnings to reach £50.2 million (and earnings per share of £0.71) by about July 2028, up from £19.4 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as £41 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 26.5x on those 2028 earnings, down from 44.1x today. This future PE is lower than the current PE for the GB Healthcare industry at 31.5x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.64%, as per the Simply Wall St company report.

CVS Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The ongoing CMA market investigation has created uncertainty and led to adverse press, potentially impacting consumer confidence and future revenues.

- Cost of living pressures in the U.K. may cause clients to delay or forgo veterinary visits, which could negatively affect revenue and earnings.

- The transition and temporary volume reduction for the Animed Direct website migration presents a risk to short-term revenue growth.

- Staffing shortages and reliance on locums could affect operational efficiency and increase costs, impacting net margins.

- The increase in debt leverage places pressure on financial resources, which may constrain future investment opportunities and affect earnings if not managed carefully.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of £15.444 for CVS Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £20.0, and the most bearish reporting a price target of just £12.5.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be £779.7 million, earnings will come to £50.2 million, and it would be trading on a PE ratio of 26.5x, assuming you use a discount rate of 6.6%.

- Given the current share price of £11.92, the analyst price target of £15.44 is 22.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.