Key Takeaways

- Burford Capital's impressive portfolio recovery and case conclusions support future revenue and cash flow growth, enhancing net margins and earnings potential.

- Transitioning to U.S. filing standards aims to improve transparency, attract investors, and positively influence stock valuation and earnings per share.

- Burford Capital's reliance on fair value accounting and high-stakes legal outcomes creates financial volatility, with regulatory and interest rate risks impacting operations and market sentiment.

Catalysts

About Burford Capital- Provides legal finance products and services worldwide.

- Burford Capital has seen an impressive recovery in its portfolio performance, resulting in record levels of net realized gains for 2024, which could support future revenue and cash flow growth as more cases are concluded successfully.

- The company is experiencing significant growth in its litigation finance portfolio, having achieved a compound annual growth rate of about 15% over the last few years. This growth, combined with higher target realizations, is expected to drive future revenue and earnings.

- Burford Capital's expanding focus on originating high-quality new business, including corporate monetizations and diverse case types, should enhance its future net margins and earnings potential, even as individual investment strategies evolve.

- The firm's effective cash management and realization of significant amounts of cash from concluded cases underscore operational efficiencies, potentially providing better net margins and positively impacting future earnings.

- Burford's ongoing transition to U.S. domestic filing standards and enhanced disclosure aims to provide greater transparency and attract investor interest, potentially influencing stock valuation and market perception, thereby supporting higher earnings per share in the future.

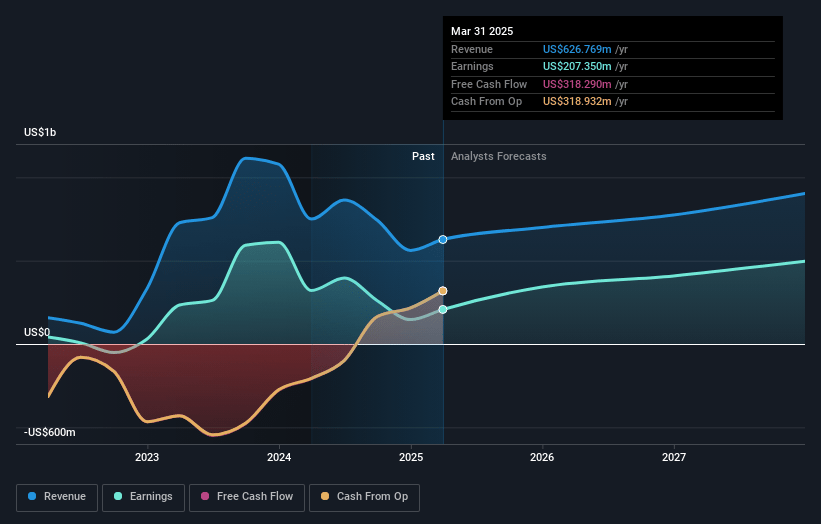

Burford Capital Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Burford Capital's revenue will grow by 17.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 26.1% today to 54.9% in 3 years time.

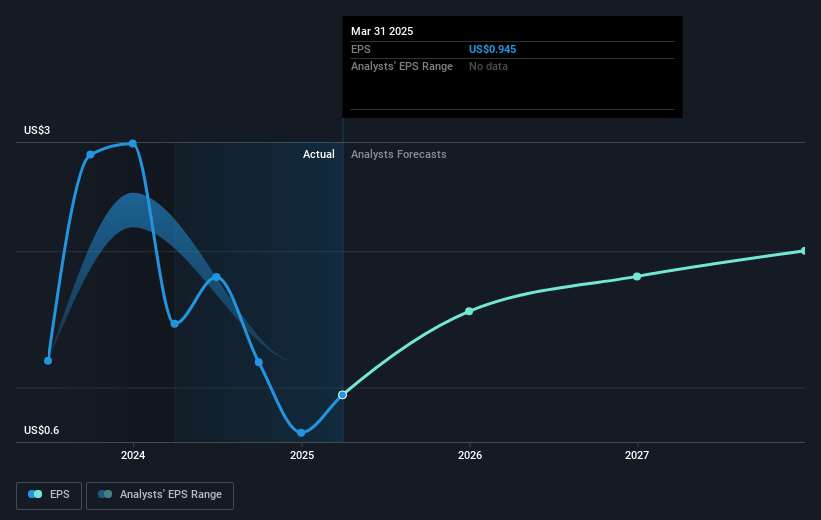

- Analysts expect earnings to reach $497.6 million (and earnings per share of $2.02) by about May 2028, up from $146.5 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $549.3 million in earnings, and the most bearish expecting $446 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.7x on those 2028 earnings, down from 20.4x today. This future PE is lower than the current PE for the GB Diversified Financial industry at 14.9x.

- Analysts expect the number of shares outstanding to grow by 0.34% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.63%, as per the Simply Wall St company report.

Burford Capital Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The reliance on fair value accounting and unrealized gains remains a concern for some investors, as any negative unrealized loss figures can trigger adverse market reactions, impacting overall investor sentiment and potentially affecting share price. (Earnings)

- The business model’s dependence on high realization of legal cases can lead to volatile revenue streams, and any downturn in legal case success rates or longer case durations could negatively affect financial performance. (Revenue, Earnings)

- Significant returns are tied to large, high-stakes cases like YPF. Delays or unfavorable outcomes in such cases could adversely impact Burford's financial outcomes. (Net Margins, Earnings)

- The firm's cash-oriented focus combined with exposure to variable interest rates could pose financial risks during periods of interest rate volatility, potentially affecting valuation metrics used in their assets. (Net Margins, Earnings)

- New U.S. regulatory changes, although considered unlikely, could impact the firm’s ability to operate freely, potentially affecting future revenue and market expansion. (Revenue, Net Margins)

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of £17.309 for Burford Capital based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $906.2 million, earnings will come to $497.6 million, and it would be trading on a PE ratio of 12.7x, assuming you use a discount rate of 7.6%.

- Given the current share price of £10.25, the analyst price target of £17.31 is 40.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.