Key Takeaways

- Strategic focus on AI and GenAI leads to strong revenue growth due to increasing client demand and successful project bookings.

- Operational streamlining aims to enhance agility and efficiency, potentially improving net margins and supporting top-line growth.

- Challenges in key sectors like Manufacturing and stagnation in North America, alongside management changes, could hinder Capgemini's revenue and earnings growth.

Catalysts

About Capgemini- Engages in the provision of consulting, digital transformation, technology, and engineering services primarily in North America, France, the United Kingdom, Ireland, the rest of Europe, the Asia-Pacific, and Latin America.

- Capgemini is currently witnessing significant traction in strategic consulting offers, particularly in AI and GenAI. With an expanding pipeline and increased demand from clients for deploying AI use cases at scale, this is expected to drive growth in revenue.

- Despite a slowdown in some sectors, Capgemini's strong positioning in Financial Services, which is showing signs of recovery, is expected to contribute positively to future earnings as the sector returns to growth.

- The firm's investment in and ongoing projects related to GenAI are beginning to yield results, with substantial bookings generated from these projects, indicating a positive impact on future revenue growth.

- Capgemini is executing initiatives to simplify operations and streamline decision processes, aiming to increase agility and focus on top-line growth. This enhanced operational efficiency could improve net margins.

- The demand for Capgemini's services related to cloud, digital core, and supply chain sustainability continues to grow. This reflects potential future revenue increases as more clients invest in transitioning to a digital economy.

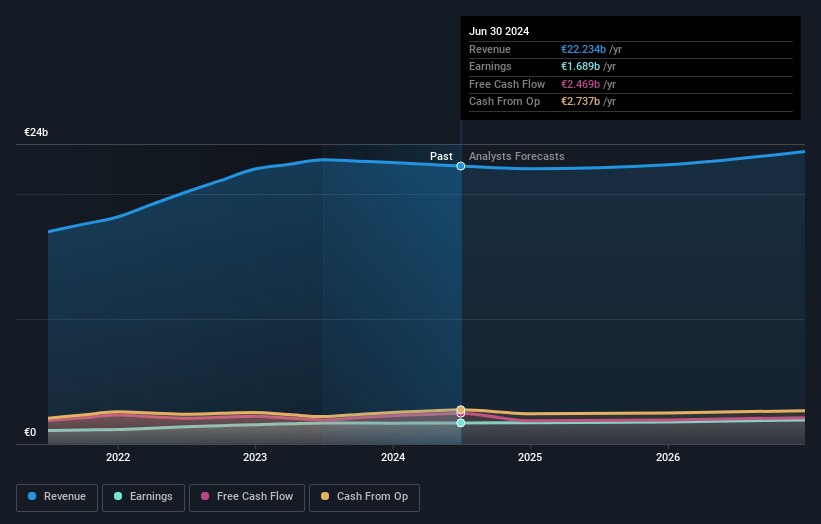

Capgemini Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Capgemini's revenue will grow by 2.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 7.6% today to 8.1% in 3 years time.

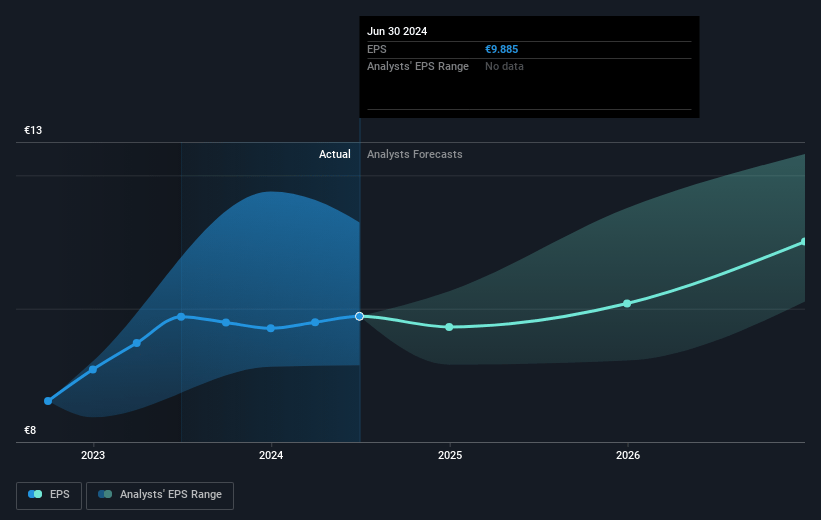

- Analysts expect earnings to reach €2.0 billion (and earnings per share of €11.25) by about January 2028, up from €1.7 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 21.9x on those 2028 earnings, up from 17.4x today. This future PE is greater than the current PE for the GB IT industry at 16.5x.

- Analysts expect the number of shares outstanding to grow by 0.77% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.49%, as per the Simply Wall St company report.

Capgemini Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The slowdown in the Manufacturing sector, which is a major segment for Capgemini, is impacting revenues, with a notable decline in this sector observed across multiple geographies. (Revenue impact)

- North America, an important market, experienced stagnation, partly due to the Manufacturing slowdown, which could affect overall earnings if the trend continues. (Earnings impact)

- The full-year 2024 growth outlook has been revised down to a negative range due to ongoing challenges in key sectors and regions like France, which could signal a persistent revenue headwind. (Revenue impact)

- Despite significant investments in areas like Generative AI, there is no indication of an increase in discretionary spending by clients, potentially limiting future earnings growth. (Earnings impact)

- Management changes, along with an ongoing effort to simplify operations, could introduce transitional risks, affecting strategic focus and potentially impacting net margins. (Net margin impact)

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €199.06 for Capgemini based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €225.0, and the most bearish reporting a price target of just €170.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €24.1 billion, earnings will come to €2.0 billion, and it would be trading on a PE ratio of 21.9x, assuming you use a discount rate of 7.5%.

- Given the current share price of €172.35, the analyst's price target of €199.06 is 13.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives