Key Takeaways

- Customer growth and mortgage recovery in Europe are driving Crédit Agricole's revenue through increased business volume and higher loan interest income.

- Emphasis on sustainable finance and asset management growth strengthens revenue potential through green loans, increased margins, and asset management fees.

- Economic challenges and climate risk factors threaten to increase Crédit Agricole's costs and credit risk, while pressures on revenue and margins persist across key segments.

Catalysts

About Crédit Agricole- Provides retail, corporate, insurance, and investment banking products and services in France and internationally.

- Crédit Agricole is benefiting from robust customer growth across its retail banks in Europe, with a net increase of over 100,000 new customers this quarter. This growing customer base is expected to drive future revenue growth as new customers contribute to increased business volume.

- The rebound in home loans in France for both regional banks and LCL in Q3 suggests a potential recovery in the mortgage lending market, which is likely to boost revenue through higher loan volumes and improved interest income in the near future.

- Crédit Agricole's asset management arm, Amundi, is reaching record levels of assets under management, which is expected to augment future revenues through asset management fees. This growth is indicative of strong performance in the Large Customers division, enhancing overall earnings.

- The integration of Degroof Petercam within Indosuez has contributed to a significant uplift in asset-gathering revenues, which should continue to enhance top-line performance. The resulting efficiencies and expanded service offerings are likely to have a positive effect on net margins over time.

- Crédit Agricole's continued emphasis on supporting the energy transition is aligned with increasing regulatory and consumer demand for sustainable finance solutions. This initiative involves a partnership with Caisse des Dépôts to finance green loans, positioning the bank for future growth in sustainable finance, thus potentially increasing revenues and improving profitability.

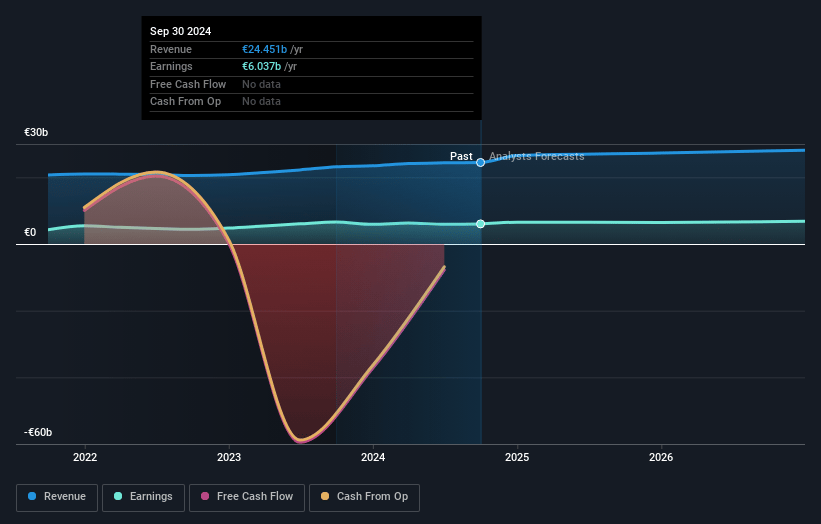

Crédit Agricole Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Crédit Agricole's revenue will decrease by -6.2% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 24.4% today to 24.0% in 3 years time.

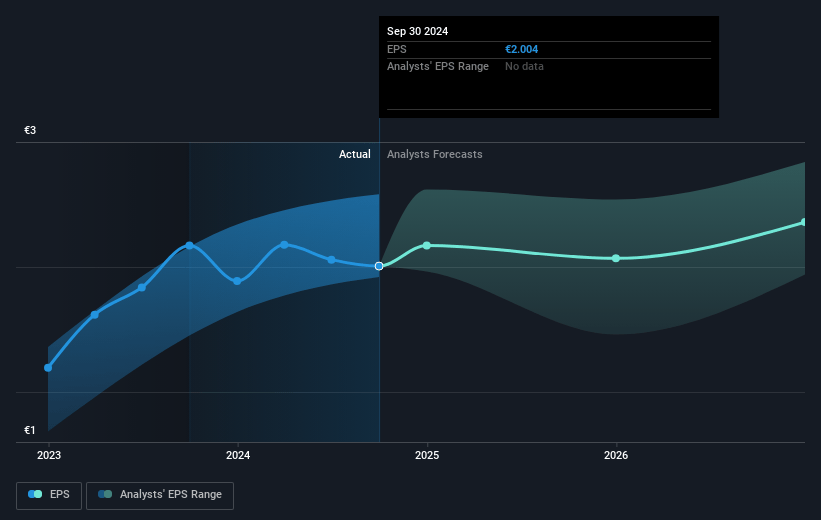

- Analysts expect earnings to reach €6.8 billion (and earnings per share of €2.11) by about January 2028, down from €8.4 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €7.9 billion in earnings, and the most bearish expecting €5.9 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 9.4x on those 2028 earnings, up from 5.2x today. This future PE is greater than the current PE for the GB Banks industry at 6.2x.

- Analysts expect the number of shares outstanding to grow by 2.07% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.62%, as per the Simply Wall St company report.

Crédit Agricole Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Increased corporate taxes in France could lead to higher operational costs, impacting Credit Agricole’s net earnings, as approximately 40% of its revenue is derived from France.

- Climate change-related events, such as increased claims from crop insurance, present a risk of higher P&C claims expenses, potentially affecting net margins within its insurance division.

- The consumer finance segment is still recovering from increased refinancing rates, which may continue to pressure revenue and margins until the back book yields improve.

- Risk-weighted asset (RWA) consumption is elevated due to increased exposure to certain segments with economic downturns, impacting the capital requirements and cost structure.

- Economic pressures, such as downgrading of creditworthiness within segments like SME and corporate sectors in France, could elevate credit risk, potentially deteriorating the asset quality and increasing provisions which affect overall profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €16.38 for Crédit Agricole based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €23.4, and the most bearish reporting a price target of just €13.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €28.4 billion, earnings will come to €6.8 billion, and it would be trading on a PE ratio of 9.4x, assuming you use a discount rate of 6.6%.

- Given the current share price of €14.47, the analyst's price target of €16.38 is 11.7% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives