Key Takeaways

- Strategic acquisitions and focus on sustainability aim to enhance Metso's product offerings and capitalize on demand for sustainable solutions in Aggregates and recycling.

- Anticipated growth in the Minerals segment and successful productivity improvements are set to drive future revenue and margins through increased orders and cost efficiencies.

- Lower order intakes and cash flow issues could negatively impact revenue and net margins, compounded by inventory challenges and operational inefficiencies.

Catalysts

About Metso Oyj- Provides technologies, end-to-end solutions, and services for aggregates, minerals processing, and metals refining industries in Europe, North and Central America, South America, the Asia Pacific, Greater China, Africa, the Middle East, and India.

- Metso is anticipating growth in the Minerals segment with larger projects expected to progress, contributing to an increase in future orders and revenues as this segment is still experiencing active market dialogues that may lead to significant orders.

- The company secured new orders in the Minerals segment after the end of the third quarter, indicating potential for a sustained order pipeline and future revenue growth, particularly in copper-related initiatives.

- Metso has implemented ongoing productivity improvement actions and completed restructuring efforts, which are expected to support improved future margins through cost efficiencies and operational effectiveness.

- The company's focus on sustainability and investment in energy-saving vertical mills through acquisitions like Swiss Tower Mills aims to capitalize on the growing demand for sustainable solutions, potentially bolstering future sales and margins.

- Acquisitions, such as Diamond Z and Screen Machine, are aligned with Metso's strategic growth initiatives in Aggregates and recycling sectors, aiming to broaden product offerings and improve revenue streams, while the overall strategy remains focused on maintaining strong margins.

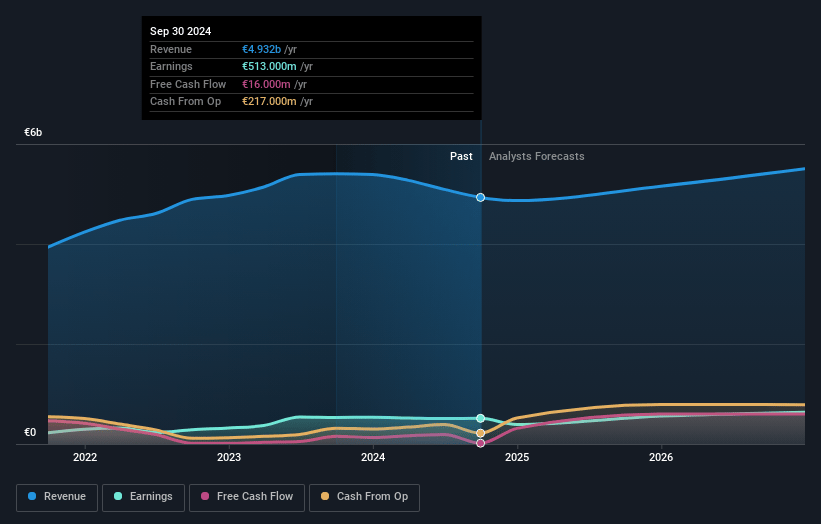

Metso Oyj Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Metso Oyj's revenue will grow by 4.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 10.4% today to 11.3% in 3 years time.

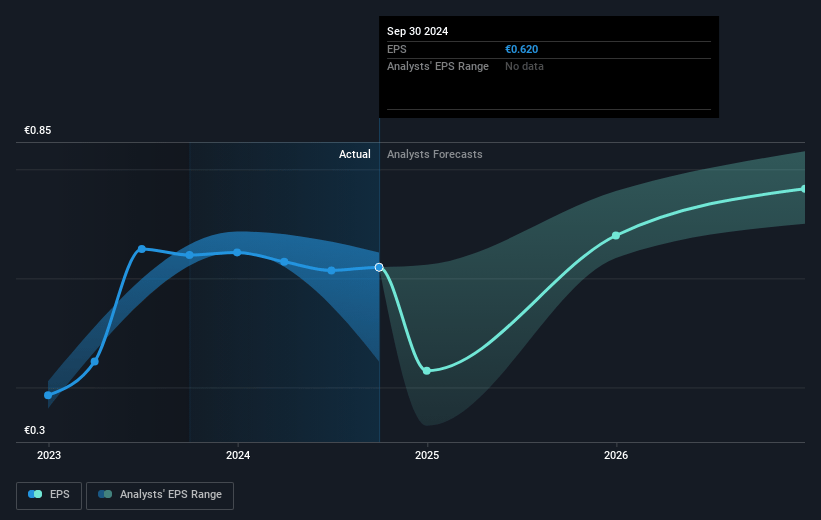

- Analysts expect earnings to reach €636.4 million (and earnings per share of €0.77) by about January 2028, up from €513.0 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as €704.2 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 17.4x on those 2028 earnings, up from 15.6x today. This future PE is greater than the current PE for the FI Machinery industry at 17.2x.

- Analysts expect the number of shares outstanding to grow by 0.14% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.5%, as per the Simply Wall St company report.

Metso Oyj Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- A significant decline in sales due to lower order intakes across multiple quarters could continue to negatively impact revenue.

- The termination of the waste-to-energy business has resulted in a one-off cash expense, pulling down earnings and cash flow from operations.

- Despite strong profitability, cash generation has been flagged as an ongoing issue, which, if not improved, could impact net margins and liquidity.

- Temporary hesitancy in customer decision-making, particularly around larger upgrades in Minerals, could lead to further delays in revenue recognition and affect earnings consistency.

- Challenges in achieving inventory reduction targets, especially in finished goods, may lead to inefficiencies and potential write-downs, affecting the cost structure and hit margins.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €11.03 for Metso Oyj based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €13.7, and the most bearish reporting a price target of just €8.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €5.6 billion, earnings will come to €636.4 million, and it would be trading on a PE ratio of 17.4x, assuming you use a discount rate of 6.5%.

- Given the current share price of €9.67, the analyst's price target of €11.03 is 12.3% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives