Key Takeaways

- Strategic focus on service and modernization, along with innovations like MiniSpace DX, aims to drive resilient growth and boost margins.

- Double-digit modernization growth outside China highlights potential for sustained revenue, despite challenges in specific regions.

- Intensifying challenges in China exert pressure on KONE's revenues and margins amid inflation, liquidity issues, and increased bad debt provisions.

Catalysts

About KONE Oyj- Engages in the elevator and escalator business worldwide.

- KONE's new strategy aims to drive scalable growth and transform the company into a more resilient business, focusing on service and modernization as key earnings growth drivers. This is expected to impact future revenues positively.

- The launch of the KONE High-Rise MiniSpace DX, tailored for both new buildings and modernization, showcases significant hardware and software innovation. This product is expected to attract demand due to its energy efficiency and connectivity features, boosting future revenues and potentially net margins.

- KONE’s emphasis on innovation and sustainability, particularly with digitally enabled services, aims to enhance value propositions. As such offerings reach a wider market, this could positively influence both revenue growth and net margins.

- The performance improvement initiatives, including pricing task forces, sales and operations excellence, and procurement efficiency, are anticipated to accelerate profitability and margin improvement through cost savings and operational optimization.

- The robust growth in service and modernization orders, especially double-digit growth in modernization in three out of four regions outside China, signifies potential for sustained revenue and earnings growth, even if new building solutions face challenges in specific regions like China.

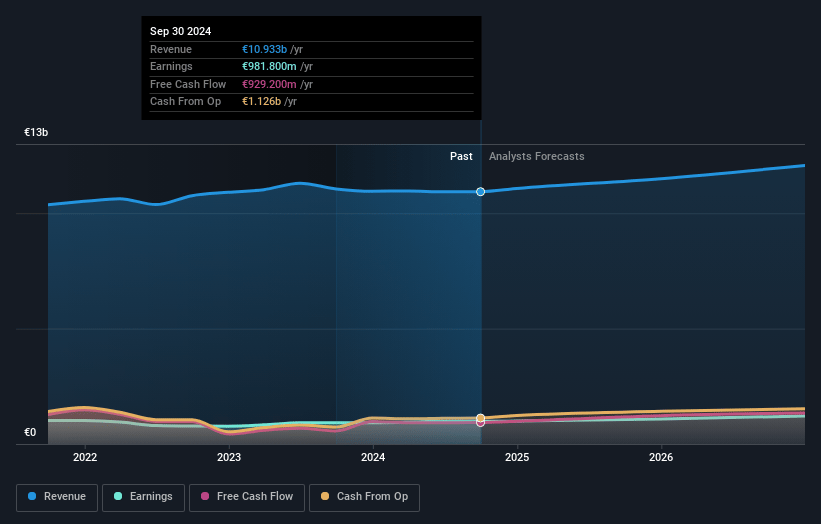

KONE Oyj Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming KONE Oyj's revenue will grow by 4.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.0% today to 10.4% in 3 years time.

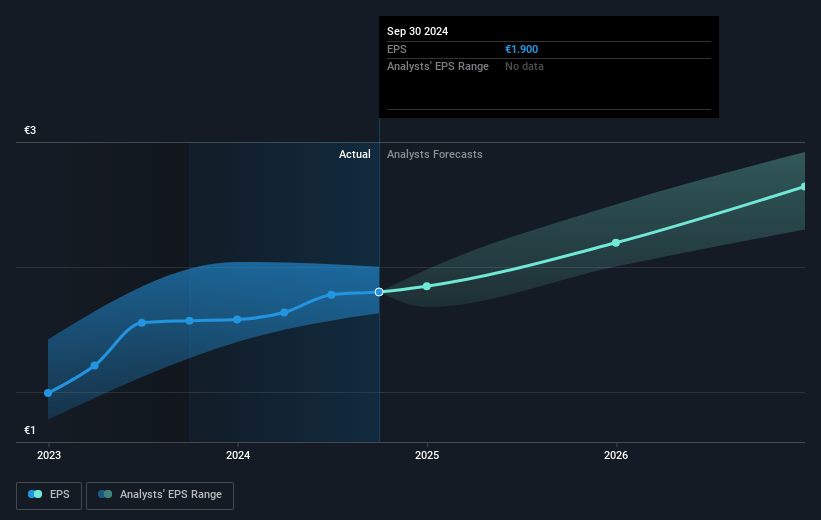

- Analysts expect earnings to reach €1.3 billion (and earnings per share of €2.5) by about January 2028, up from €981.8 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 24.6x on those 2028 earnings, down from 25.5x today. This future PE is greater than the current PE for the GB Machinery industry at 17.2x.

- Analysts expect the number of shares outstanding to grow by 0.28% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.05%, as per the Simply Wall St company report.

KONE Oyj Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Intensifying headwinds in China, with significant sales and profitability declines of around 20%, indicate potential continued pressure on revenues and margins in one of KONE's largest markets.

- The prolonged liquidity challenges faced by property developers in China and increased consumer hesitance could further slow new building solutions sales, negatively impacting revenue growth.

- Ongoing broad-based inflation and margin pressure, especially in New Building Solutions in China, could continue to erode the company's profitability.

- The adjustment of EBIT margin expectations for 2024 from 11.5%-12.2% to 11.5%-11.9% due to a challenging market environment in China highlights the risk of underwhelming performance impacting earnings.

- Increased provisions for bad debt, which had a negative impact of approximately €20 million on adjusted EBIT, suggest potential continuing risks to net margins if economic conditions do not improve.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €51.64 for KONE Oyj based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €65.0, and the most bearish reporting a price target of just €37.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €12.5 billion, earnings will come to €1.3 billion, and it would be trading on a PE ratio of 24.6x, assuming you use a discount rate of 6.0%.

- Given the current share price of €48.42, the analyst's price target of €51.64 is 6.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives