Key Takeaways

- Strong growth in the Environment and Water segments, driven by strategic acquisitions and rate increases, suggests potential future earnings and stable profit margins.

- U.S. market expansion and significant Concessions growth signal potential revenue enhancements and margin improvements, despite reductions in Construction revenues.

- Revenue decrease from major project completions and foreign exchange volatility may impact earnings and investor confidence; increased debt could strain financial resources.

Catalysts

About Fomento de Construcciones y Contratas- Engages in the environmental services, water management, infrastructure development, and real estate businesses in Europe and internationally.

- The Environment segment demonstrated strong growth with a 16.7% increase in revenues, driven by organic growth and strategic acquisitions, significantly improving EBITDA by 46.2%, which suggests potential future increases in earnings.

- The Water division benefitted from rate increases across multiple geographies, leading to a revenue growth of 10.1% and stable EBITDA margins, indicating potential for sustained revenue growth and profit margins.

- Expansion in the U.S. market through organic contracts and new acquisitions, such as the Recycling Holdings Group, suggests potential future revenue enhancements and earnings from a growing market.

- The Concessions segment saw significant revenue growth of 26.5%, driven by new project developments in Spain, which could point to future increases in revenues and positive impacts on net margins as these projects mature.

- Reductions in Construction revenues due to completed projects like the Maya Train project are offset by growth in new project portfolios, particularly in the U.S., which indicates resilience and potential long-term revenue and earnings stability from newly secured contracts.

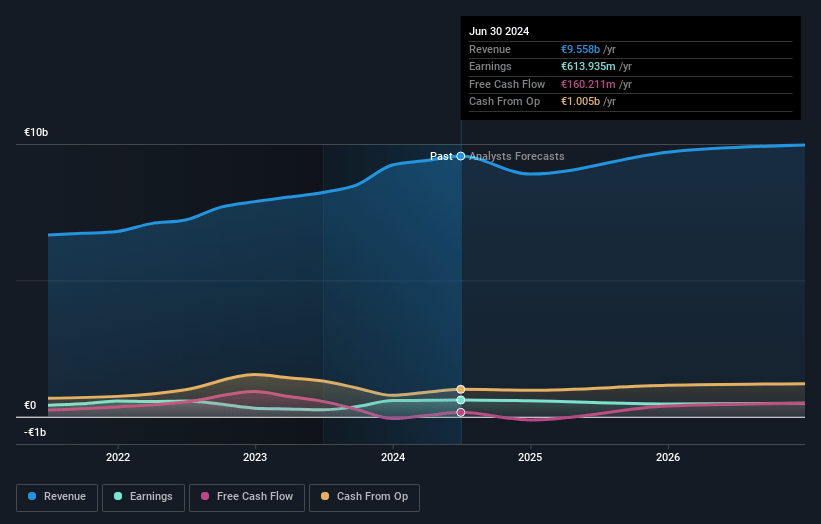

Fomento de Construcciones y Contratas Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Fomento de Construcciones y Contratas's revenue will grow by 2.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 3.2% today to 4.5% in 3 years time.

- Analysts expect earnings to reach €455.1 million (and earnings per share of €1.25) by about May 2028, up from €293.7 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €534 million in earnings, and the most bearish expecting €386 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 17.4x on those 2028 earnings, up from 16.5x today. This future PE is greater than the current PE for the GB Commercial Services industry at 14.2x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 10.56%, as per the Simply Wall St company report.

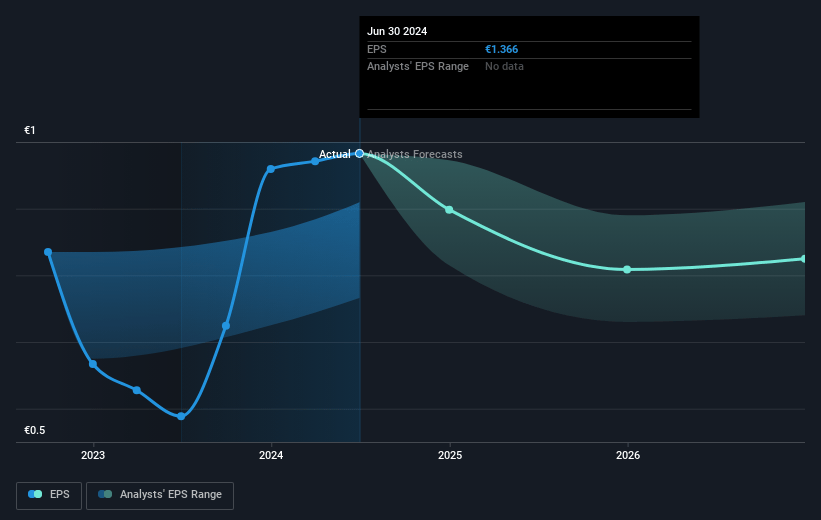

Fomento de Construcciones y Contratas Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The partial carve-out of Cement and Real Estate in 2024 has led to a significant fall in net profits, which could impact the company's overall earnings and investor confidence.

- The completion of key projects like the Maya Train in Mexico and the Santiago Bernabeu stadium in Spain has resulted in a revenue decrease in the Construction sector, potentially affecting future revenue streams.

- The asymmetrical impact of foreign exchange rate fluctuations has negatively affected net profit, indicating potential instability in earnings due to exchange rate volatility.

- Completion of certain significant projects without equivalent replacements has led to reduced revenues in some geographical markets, risking future revenue consistency.

- Expansion of working capital has slightly increased net financial debt, which may strain financial resources and affect profit margins if not managed effectively.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €12.943 for Fomento de Construcciones y Contratas based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €15.4, and the most bearish reporting a price target of just €11.5.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €10.1 billion, earnings will come to €455.1 million, and it would be trading on a PE ratio of 17.4x, assuming you use a discount rate of 10.6%.

- Given the current share price of €10.63, the analyst price target of €12.94 is 17.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.