Key Takeaways

- Tryg's price increases in key segments and investment in synergies are expected to combat inflation, boost revenue, and improve profit margins.

- A focus on risk profile transformation and portfolio derisking is aimed at stabilizing returns and achieving consistent earnings growth.

- Reliance on price increases amidst inflationary pressures and unfavorable currency fluctuations could risk revenue stability, while derisked investments may reduce income.

Catalysts

About Tryg- Provides insurance products and services for private and corporate customers, and small and medium-sized businesses in Denmark, Sweden, the United Kingdom, and Norway.

- Tryg is implementing price increases in its Private and Commercial segments to combat inflationary pressures, particularly in Norway, which should boost revenue and improve profit margins over time.

- The company plans to achieve synergies from the RSA Scandinavia acquisition by leveraging scale across systems, infrastructure, and customer excellence, which is expected to lift earnings by DKK 930 million in the full year of 2024.

- Tryg's strategy to run a smaller, more controlled Corporate book is transforming its risk profile to focus on areas with higher familiarity, which is likely to stabilize or improve net margins.

- The derisking of Tryg's investment portfolio by selling risky assets and buying highly rated government bonds ensures more stable investment returns, which should contribute to consistent earnings growth.

- Tryg aims to improve the overall Insurance Service Result (ISR) by DKK 1 billion by 2027 through the pillars of Scale & Simplicity, Technical Excellence, and Customer & Commercial Excellence, driving revenue and expanding profit margins.

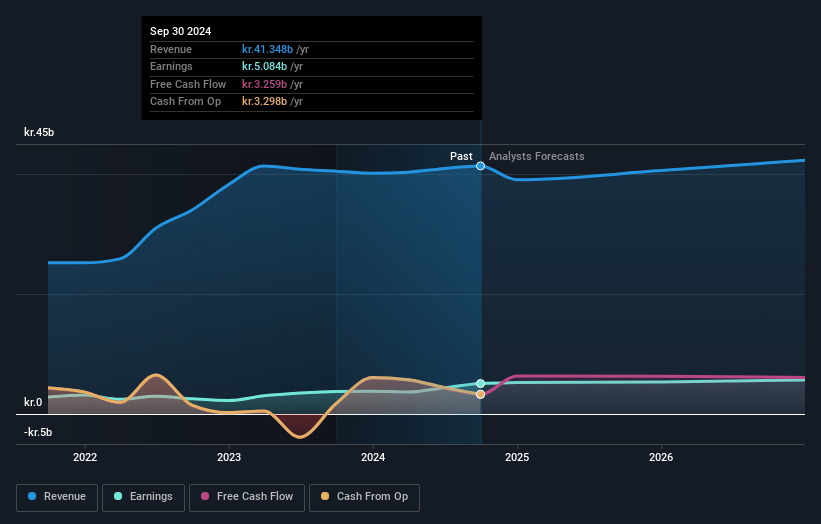

Tryg Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Tryg's revenue will grow by 2.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 11.5% today to 12.8% in 3 years time.

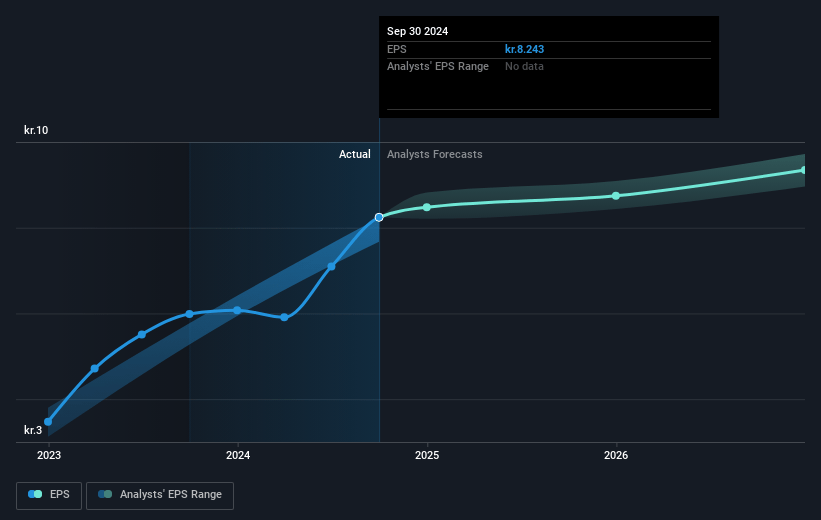

- Analysts expect earnings to reach DKK 5.6 billion (and earnings per share of DKK 9.54) by about April 2028, up from DKK 4.7 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 21.6x on those 2028 earnings, up from 19.6x today. This future PE is lower than the current PE for the GB Insurance industry at 25.2x.

- Analysts expect the number of shares outstanding to decline by 0.37% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 4.78%, as per the Simply Wall St company report.

Tryg Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's reliance on price increases to offset inflationary pressures may not be sustainable if inflation persists or worsens, potentially impacting revenue and margins.

- The reduction of their Corporate segment to a more controllable size could potentially limit revenue growth opportunities from larger corporate clients.

- Possible currency fluctuations, particularly with the Norwegian krone and Swedish krona, have been unfavorable and could continue to impact the synergies and financial results, thus affecting net earnings.

- The investment result is expected to be lower but more stable due to the derisking of the free portfolio, suggesting a potential decrease in investment income, which can affect overall earnings.

- Loss of customer satisfaction due to price increases might lead to lower retention rates, threatening future revenue stability and growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of DKK176.273 for Tryg based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of DKK190.0, and the most bearish reporting a price target of just DKK152.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be DKK44.0 billion, earnings will come to DKK5.6 billion, and it would be trading on a PE ratio of 21.6x, assuming you use a discount rate of 4.8%.

- Given the current share price of DKK153.0, the analyst price target of DKK176.27 is 13.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.