Last Update 04 Dec 25

Fair value Decreased 0.84%FLS: Capital Markets Day Will Unlock Upside Despite CEO Transition And Guidance Update

The analyst fair value estimate for FLSmidth has edged down by DKK 4 to DKK 470.88, as analysts balance a slightly higher discount rate against a reaffirmed positive long term outlook, supported by recent upward revisions to several Street price targets despite mixed ratings.

Analyst Commentary

Recent Street research reflects a generally constructive view on FLSmidth, with several firms lifting price targets and one notable downgrade tempering the consensus. Overall, the pattern points to confidence in medium term growth and capital allocation, offset by concerns about near term execution and valuation after a strong share price run.

Bullish Takeaways

- Bullish analysts have raised price targets into the DKK 540 to DKK 580 range, indicating upside potential versus the current fair value estimate as they factor in stronger long term earnings power.

- Several upgrades to Buy highlight improving conviction in FLSmidth's growth profile, particularly around its ability to convert its order backlog and capitalize on structural demand in mining and cement technologies.

- The upcoming capital markets day is viewed as a near term catalyst, with expectations that management will provide clearer medium term margin and cash flow targets that could support a re rating.

- Positive target revisions suggest confidence that recent operational missteps, including a weaker Q3, are temporary and that management can deliver on cost efficiency and project execution improvements.

Bearish Takeaways

- Bearish analysts have moved to more neutral stances with Hold ratings, citing a risk that recent share price strength already discounts much of the anticipated margin expansion and growth recovery.

- Concerns persist around the company’s ability to consistently meet quarterly expectations, with recent estimate misses reinforcing execution risk in complex project businesses.

- Some targets remain materially below the most optimistic levels, signaling skepticism that FLSmidth can fully achieve or sustain the higher profitability and growth embedded in the upper end of Street forecasts.

- There is caution that any disappointment at the capital markets day, particularly on long term margin guidance or capital allocation, could trigger multiple compression from current valuation levels.

What's in the News

- CEO Mikko Keto has informed the Board of his intention to step down to join a non competing company, with a structured succession process underway and his departure expected in the first half of 2026, following a tenure marked by portfolio rationalisation and operational streamlining (Key Developments).

- FLSmidth updated its 2025 earnings guidance, now expecting revenue of around DKK 14.5 billion, narrowing and effectively lowering the previous range of DKK 14.5 billion to DKK 15.0 billion (Key Developments).

- The company secured a major order from a long standing Indian mining and steel customer to supply core technologies for what is set to be one of the world’s largest and most sustainable iron ore beneficiation plants, including the world’s largest filtered tailings system and high rate thickeners, with delivery expected in 2026 (Key Developments).

Valuation Changes

- Fair Value edged down slightly from DKK 474.88 to DKK 470.88, reflecting a modest tightening in the valuation range.

- The Discount Rate has risen slightly from 6.48 percent to 6.52 percent, implying a marginally higher required return and modest pressure on the valuation.

- Revenue Growth is effectively unchanged at around minus 5.33 percent, indicating no material shift in top line expectations.

- The Net Profit Margin is effectively stable at about 10.68 percent, with changes too small to alter the earnings quality view.

- Future P/E eased slightly from 17.11x to 16.98x, suggesting a marginally lower multiple applied to forward earnings.

Key Takeaways

- Expansion of resilient, high-margin service and aftermarket operations, alongside cost base optimization, sets the stage for sustainable earnings growth and improved margins.

- Streamlined focus on mining, brownfield upgrades, and decarbonization strengthens market leadership, positioning the company for enhanced cash flow and shareholder returns.

- Heavy reliance on cyclical mining capex and slow structural transition to services leave FLSmidth exposed to volatile revenue, margin pressure, and risks from industry shifts or poor execution.

Catalysts

About FLSmidth- Provides flowsheet technology and service solutions for the mining and cement industries in Denmark, the United States of America, Canada, Chile, Brazil, Peru, Australia, North and South America, Europe, the Middle East, Africa, and Asia.

- FLSmidth's focus on expanding its service and aftermarket business (which generates recurring, higher-margin revenue and is more resilient through cycles) positions it to sustainably grow net margins and earnings stability, especially as the company replicates successful practices from its high-growth, high-profitability PCV segment across its Service operation.

- The company is proactively streamlining its fixed cost base (SG&A and corporate overhead) and rightsizing the Product division to ensure a scalable platform; when capital equipment demand recovers (expected towards late 2026/2027), operating leverage should drive a step up in EBITA margin and earnings as volumes rebound.

- Strength in brownfield upgrades, process optimization, and digital solutions-closely aligned with mining clients' needs to improve resource efficiency and comply with stricter environmental standards-positions FLSmidth to capture a greater share of customer spend and grow both topline and gross margins as decarbonization and circularity become more important in the industry.

- FLSmidth's leading installed base and dominant market position in key growth geographies (notably Chile for copper), combined with the industry's long-term need for minerals essential to the energy transition, is set to boost order intake and revenue growth once major project sanctions resume and mining capex rebounds.

- Ongoing disposal of the low-margin Cement business, portfolio simplification, and a focus on high-aftermarket potential equipment will free up capital, reduce risk, and enhance overall return on invested capital, supporting improved cash generation and shareholder returns over time.

FLSmidth Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming FLSmidth's revenue will decrease by 6.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.6% today to 9.9% in 3 years time.

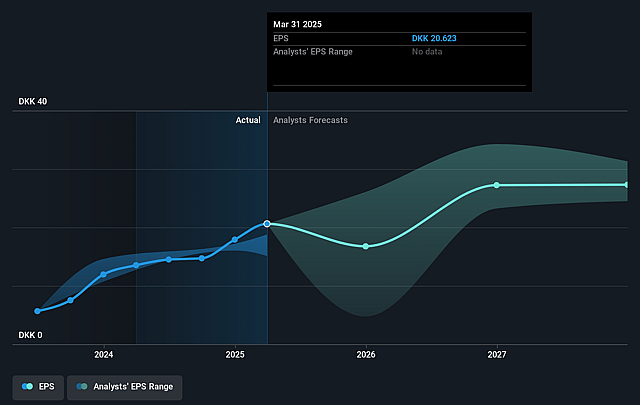

- Analysts expect earnings to reach DKK 1.6 billion (and earnings per share of DKK 30.04) by about September 2028, up from DKK 1.3 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as DKK1.4 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 18.6x on those 2028 earnings, up from 18.1x today. This future PE is greater than the current PE for the GB Machinery industry at 18.1x.

- Analysts expect the number of shares outstanding to grow by 0.28% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.12%, as per the Simply Wall St company report.

FLSmidth Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Persistent softness and volatility in the Product (capital equipment) business segment, with cyclical, lumpy demand, high fixed costs, and current negative EBITA, expose FLSmidth to prolonged periods of weak revenue and earnings, especially if the anticipated upturn in late 2026/2027 is delayed or softer than expected.

- Customer hesitancy and delays in sanctioning new mining projects-particularly in core markets like South America-reflect a broader global trend of capital expenditure caution, regulatory uncertainty, and potentially longer cycles, creating downside risk to order intake, revenue growth, and cash flow.

- FLSmidth's dependence on mining sector capex cycles and overexposure to large, one-off product orders heightens revenue volatility and limits resilience to structural shifts such as decarbonization policies, resource nationalism, or technological disruption (e.g., Industry 4.0, alternative processing solutions) that could shrink the addressable market or redirect investment to new solutions beyond FLSmidth's portfolio.

- Ongoing rightsizing and restructuring efforts in Products and SG&A reductions signal underlying challenges with adapting the legacy business model to a scalable, service-led operation; execution risk, slow transition, and failure to fully align cost base could result in margin compression and suboptimal profitability, especially in a capex-light market.

- The successful transformation to a higher-margin, recurring revenue service and PCV business is heavily reliant on replicating internal best practices and commercial excellence across regions; if these efforts fall short, or if intensified competition, substitution by alternative solutions, or supply chain disruptions increase, FLSmidth's net margins and earnings stability could be undermined.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of DKK446.75 for FLSmidth based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of DKK500.0, and the most bearish reporting a price target of just DKK344.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be DKK16.2 billion, earnings will come to DKK1.6 billion, and it would be trading on a PE ratio of 18.6x, assuming you use a discount rate of 6.1%.

- Given the current share price of DKK421.0, the analyst price target of DKK446.75 is 5.8% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on FLSmidth?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.