Last Update 10 Dec 25

Fair value Decreased 1.19%SHL: Dividend Growth Will Drive Long-Term Upside Despite Recent Price Target Cuts

Analysts have trimmed their price targets for Siemens Healthineers by EUR 4 to about EUR 57, reflecting slightly lower fair value and growth assumptions, even as margin expectations and longer term valuation multiples remain broadly supportive.

Analyst Commentary

Recent target cuts have been largely incremental, with bullish analysts maintaining a supportive stance on the long term earnings trajectory and valuation framework despite trimming near term expectations.

Bullish Takeaways

- Bullish analysts continue to see upside potential relative to the current share price, as indicated by the new targets remaining clustered in the high 50s. This implies confidence in the medium term growth algorithm.

- The decision to keep Buy ratings intact while reducing targets suggests that execution on core franchises is still viewed as robust. Adjustments appear driven more by macro and sector wide assumptions than by company specific concerns.

- Revisions from the low 60s to the high 50s indicate only modest re calibration of valuation multiples. This points to sustained belief in margin resilience and cash generation supporting a premium to the broader medtech peer group.

- Target changes over time, including the earlier move from EUR 62 to EUR 61 and now to the high 50s, are gradual rather than abrupt. This reinforces the view that earnings risk is manageable and not indicative of a structural downgrade to growth.

Bearish Takeaways

- Bearish analysts are signaling slightly more conservative growth and earnings expectations, with lower price targets reflecting caution around near term demand normalization and the pace of margin expansion.

- The step down in targets from the low 60s toward the mid to high 50s points to some compression in assumed valuation multiples. This suggests increased scrutiny of execution risk and potential delays in achieving planned operating efficiencies.

- Successive downward revisions over recent months highlight lingering uncertainty around the strength of the order pipeline and the sustainability of recent improvements in profitability, particularly in more cyclical or capital intensive segments.

- While not triggering rating changes, the target cuts underscore a more balanced risk reward profile in the short term, with less room for execution missteps before further adjustments to forecasts and valuation assumptions become necessary.

What's in the News

- Siemens Healthineers AG has proposed raising its dividend for 2025 by EUR 0.05 per share, bringing the total to EUR 1.00 per share, signaling confidence in cash generation and shareholder returns (Key Developments).

- The company announced an annual dividend of EUR 1.00 per share payable on February 10, 2026, with an ex date of February 06, 2026 and record date of February 09, 2026, reinforcing its commitment to a steady payout policy (Key Developments).

- New guidance for the first quarter of 2026 indicates revenue growth is expected to be below the 5 to 6 percent outlook range, with full year 2026 comparable revenue still targeted at 5 to 6 percent, but earnings growth seen as constrained by macro headwinds, including a strong euro and tariffs (Key Developments).

- Aiforia Technologies and Siemens Healthineers Finland have entered a local co-marketing and sales agreement to integrate Aiforia's AI powered pathology solutions into Siemens Healthineers' offering, aiming to accelerate adoption of AI driven precision diagnostics across Finnish healthcare providers (Key Developments).

- Siemens Healthineers has launched the Atellica DT 250 benchtop analyzer, which consolidates high throughput drug testing, serum toxicology, and automated specimen validity checks into a compact system designed for both clinical and non clinical settings, extending capabilities that were previously limited to larger floor standing analyzers (Key Developments).

Valuation Changes

- Fair Value: reduced slightly from €57.67 to €56.99, reflecting a modest downward tweak in the intrinsic value estimate.

- Discount Rate: lowered marginally from 6.19 percent to 6.15 percent, implying a slightly less demanding required return.

- Revenue Growth: trimmed modestly from 5.36 percent to 5.32 percent, signaling a small reduction in long term top line growth assumptions.

- Net Profit Margin: increased slightly from 11.76 percent to 11.85 percent, pointing to a minor upgrade in profitability expectations.

- Future P/E: nudged up from 22.63x to 22.79x, indicating a small expansion in the forward valuation multiple applied to earnings.

Key Takeaways

- Innovation in imaging and AI diagnostics, plus digital adoption, is driving order growth, margin improvement, and recurring, higher-quality revenues worldwide.

- Rising chronic diseases, aging populations, and emerging market investments will sustain long-term market expansion, supporting continued revenue and margin gains.

- Tariff pressures, China market challenges, unfavorable currency shifts, operational restructuring, and industry competition all threaten margins, pricing power, and long-term growth.

Catalysts

About Siemens Healthineers- Through its subsidiaries, develops, manufactures, and sells a range of diagnostic and therapeutic products and services to healthcare providers worldwide.

- Strong, ongoing innovation in advanced imaging (e.g., Photon Counting CT, molecular imaging) and AI-driven diagnostic solutions is fueling robust order growth across all global markets, supporting both revenue expansion and higher net margins as adoption increases.

- A rapidly aging population and rising chronic disease incidence are consistently boosting demand for high-precision diagnostics and individualized therapies-core competencies for Siemens Healthineers-indicating a durable multi-year uplift in addressable market size and likely top-line growth.

- Expansion of long-term Value Partnerships with hospitals and healthcare systems is shifting the business mix toward higher recurring revenue streams, which help stabilize earnings, improve revenue visibility, and support sustained operating margin expansion.

- Accelerating digital and AI adoption in healthcare-alongside a growing installed base of automated, integrated diagnostic platforms-positions Siemens Healthineers to capture higher-margin software and solutions revenues, enhancing overall earnings quality.

- Emerging market healthcare infrastructure investments, alongside potential recovery in China, offer significant room for market share gains and volume growth in advanced medical equipment, providing upside potential to both revenue and net margin as global demand resumes.

Siemens Healthineers Future Earnings and Revenue Growth

Assumptions

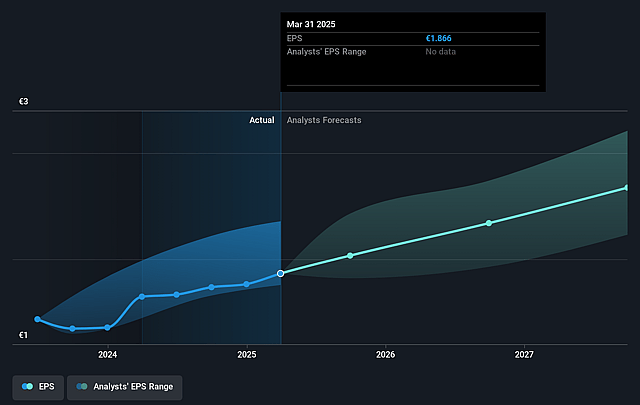

How have these above catalysts been quantified?- Analysts are assuming Siemens Healthineers's revenue will grow by 5.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.3% today to 11.7% in 3 years time.

- Analysts expect earnings to reach €3.2 billion (and earnings per share of €2.86) by about September 2028, up from €2.2 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as €2.6 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 25.2x on those 2028 earnings, up from 23.9x today. This future PE is greater than the current PE for the DE Medical Equipment industry at 17.0x.

- Analysts expect the number of shares outstanding to grow by 0.65% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.93%, as per the Simply Wall St company report.

Siemens Healthineers Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Exposure to significant and increasing tariff headwinds, particularly in the Imaging and Advanced Therapies segments, poses a risk to profitability as mid-term mitigation strategies like value-add relocation and pricing adjustments may take time to fully materialize, likely pressuring net margins and EPS.

- Prolonged weakness and structural challenges in the China market-especially the ongoing impact of China's volume-based procurement (VBP) in Diagnostics-are resulting in a reset of pricing and distribution models, suppressing revenue growth and compressing margins for a key region that has yet to show sustained recovery.

- Unfavorable foreign exchange movements, especially from the depreciation of the U.S. dollar against the euro, create translational headwinds that impact group revenues and margins, with current hedges only delaying the negative effects that are set to increase in coming quarters.

- Ongoing restructuring and portfolio simplification in Diagnostics, including site closures and product line discontinuations, signal underlying operational weaknesses; without a clear timeline for margin recovery, near

- and mid-term earnings could remain under pressure.

- Intense industry competition, particularly in digital diagnostics and imaging, as well as growing price sensitivity from healthcare providers under value-based care models, increase the risk of commoditization and market share loss-threatening Siemens Healthineers' pricing power and sustainable revenue growth over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €60.183 for Siemens Healthineers based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €65.0, and the most bearish reporting a price target of just €50.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €27.4 billion, earnings will come to €3.2 billion, and it would be trading on a PE ratio of 25.2x, assuming you use a discount rate of 5.9%.

- Given the current share price of €46.66, the analyst price target of €60.18 is 22.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Siemens Healthineers?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.