Key Takeaways

- MTU is positioned for revenue growth with increased aircraft demand, MRO services, and significant contract wins boosting market share and earnings.

- New Eurofighter orders and the GTF Advantage program promise steady income and expanded product offerings, enhancing long-term revenue stability.

- Management turnover, supply chain delays, cash flow volatility, and dependence on the GTF program strain MTU's profitability and financial flexibility.

Catalysts

About MTU Aero Engines- Engages in the development, manufacture, marketing, and maintenance of commercial and military aircraft engines, and aero-derivative industrial gas turbines in Germany, other European countries, North America, Asia, and internationally.

- The strong forecasted growth in passenger (8%) and cargo (6%) traffic for 2025 by the IATA, combined with ongoing high demand for new aircraft, positions MTU to benefit from increased sales of spare and lease engines, which can bolster revenue growth.

- Increased demand for maintenance and spare parts due to airlines extending the service lives of older aircraft and supply chain constraints providing pricing opportunities in MRO services could enhance MTU's net margins through improved pricing power and higher utilization of limited MRO capacities.

- The GTF Advantage program, which is expected to receive final FAA certification in H1 2025, indicates a pipeline of future engine deliveries and associated revenues. This could also improve earnings as product offerings expand.

- Recent contract wins totaling USD 5.6 billion in the commercial MRO sector demonstrate MTU's ability to secure significant business, which is likely to continue driving revenue growth and expanding market share, thus impacting earnings positively.

- Growth in the Military business due to new Eurofighter orders and development work on the New Generation Fighter Engine promises long-term steady income streams that could positively influence MTU’s overall revenue and provide stability to earnings.

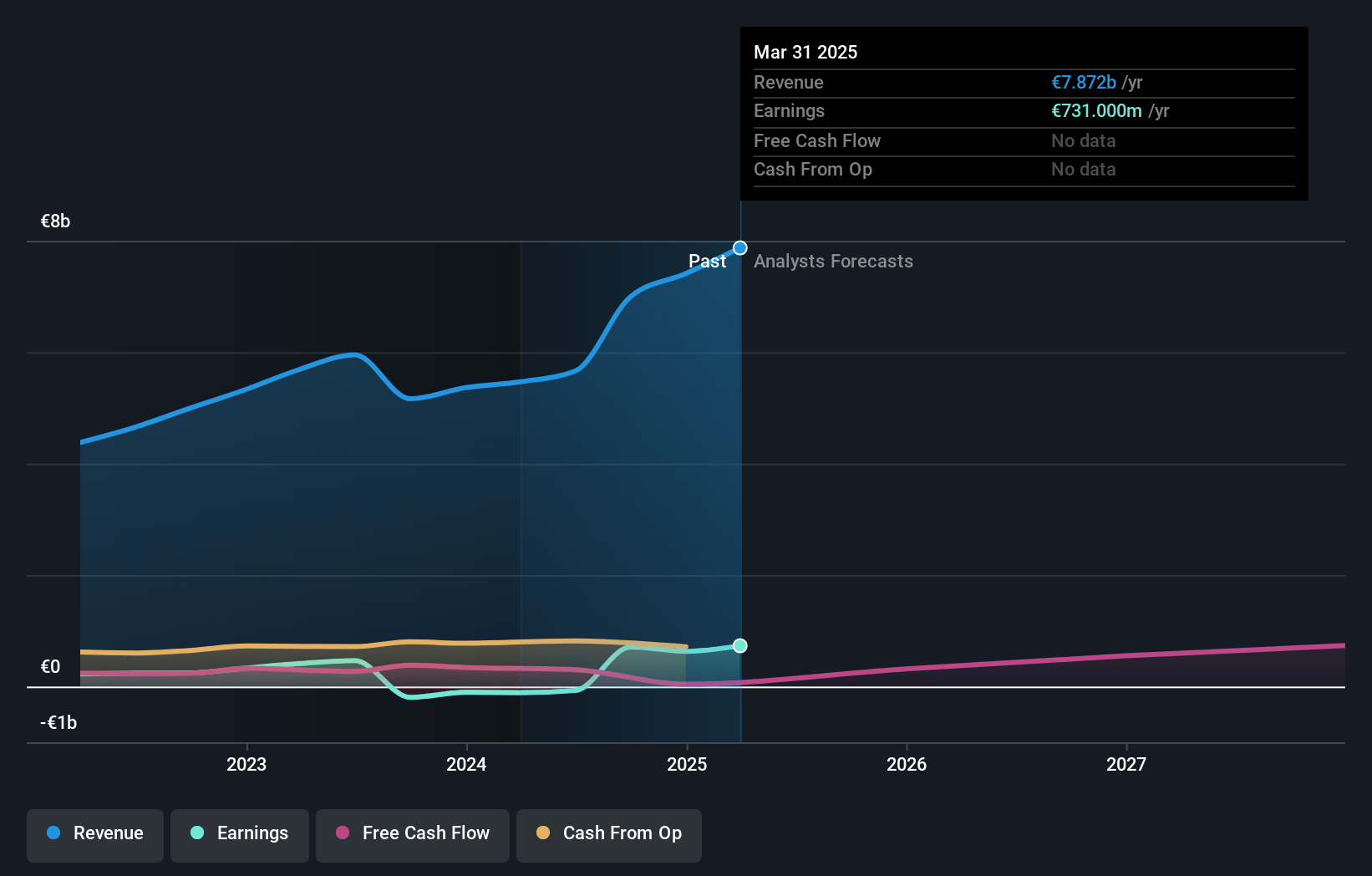

MTU Aero Engines Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming MTU Aero Engines's revenue will grow by 11.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 8.5% today to 9.7% in 3 years time.

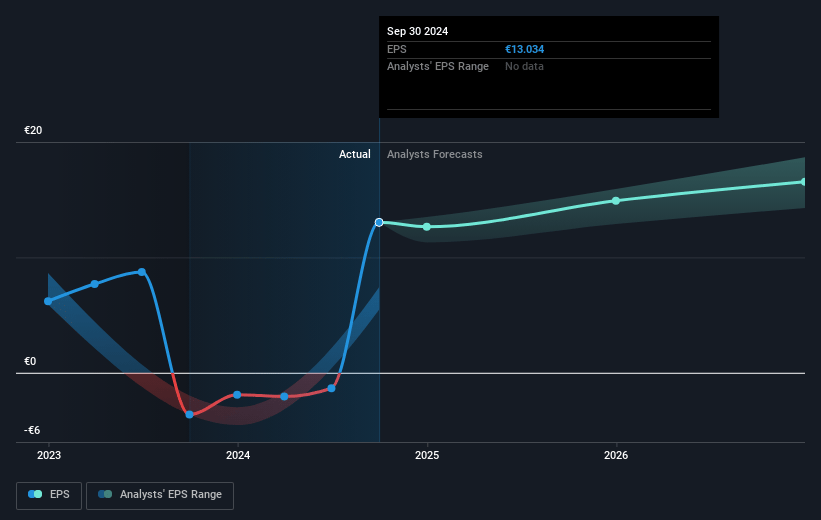

- Analysts expect earnings to reach €991.0 million (and earnings per share of €17.92) by about May 2028, up from €633.0 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as €882 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 21.3x on those 2028 earnings, down from 25.8x today. This future PE is lower than the current PE for the GB Aerospace & Defense industry at 70.9x.

- Analysts expect the number of shares outstanding to grow by 0.39% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 4.79%, as per the Simply Wall St company report.

MTU Aero Engines Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Management turnover poses a risk, as both the CEO and CFO are set to change, potentially leading to strategic realignments and disruptions. This could affect MTU’s strategic execution and operational efficiency, impacting profits and overall financial performance.

- Ongoing supply chain challenges are leading to delays in aircraft deliveries and elevated turnaround times for Maintenance, Repair, and Overhaul (MRO) services, which can result in increased working capital requirements, impacting cash flow negatively.

- The volatility in free cash flow highlighted by the significant impacts of the GTF fleet management plan, including cash payments to airlines for fleet management, puts pressure on MTU’s liquidity position, limiting financial flexibility.

- Dependence on the GTF engine program, which involves upfront costs and deferred payments, can strain MTU's revenue recognition and working capital over time, affecting short-term profitability and earnings.

- Potential reduction in leasing revenue and a normalization of leasing rates in the Asset Management business could decrease MTU’s profitability if not compensated by other revenue streams, impacting margins and earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €339.053 for MTU Aero Engines based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €416.0, and the most bearish reporting a price target of just €250.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €10.2 billion, earnings will come to €991.0 million, and it would be trading on a PE ratio of 21.3x, assuming you use a discount rate of 4.8%.

- Given the current share price of €303.9, the analyst price target of €339.05 is 10.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.