Last Update05 Sep 25Fair value Decreased 0.77%

Ping An Insurance (Group) Company of China saw essentially stable valuation metrics, with only marginal decreases in both its future P/E ratio and consensus analyst price target, which slipped slightly from CN¥68.90 to CN¥68.37.

What's in the News

- Ping An Insurance announced an interim dividend of RMB 0.95 per share in cash, up 2.2% year-on-year for the six months ended June 30, 2025.

- A board meeting was scheduled to consider and approve interim results for the six months ending June 30, 2025, and discuss the payment of an interim dividend.

Valuation Changes

Summary of Valuation Changes for Ping An Insurance (Group) Company of China

- The Consensus Analyst Price Target remained effectively unchanged, moving only marginally from CN¥68.90 to CN¥68.37.

- The Discount Rate for Ping An Insurance (Group) Company of China remained effectively unchanged, moving only marginally from 9.12% to 9.24%.

- The Future P/E for Ping An Insurance (Group) Company of China remained effectively unchanged, moving only marginally from 10.00x to 9.96x.

Key Takeaways

- AI and technology enhancements are boosting operational efficiency, reducing costs, and positively impacting net margins within Ping An's services.

- Expansion in finance, health, and senior care, with strong customer engagement, is set to drive revenue by targeting China's aging population and healthcare needs.

- Heavy reliance on China's economy and insurance sector could compress margins, while tech investments pose risk without swift efficiency gains.

Catalysts

About Ping An Insurance (Group) Company of China- Ping An Insurance (Group) Company of China, Ltd.

- Ping An Insurance is leveraging AI and technology to improve operational efficiency and reduce costs, which is likely to positively impact net margins as they optimize processes across their financial services and senior care offerings.

- The company is actively expanding its integrated finance, health, and senior care services, with a large customer base and high retention rates, which is expected to drive revenue growth through increased customer engagement and new service offerings.

- The continued development and expansion of their health and senior care network and services, along with strategic partnerships with top hospitals, are positioned to increase revenue by tapping into the growing aging population and rising healthcare demands in China.

- Ping An's long-term investment strategy with insurance funds in high-yield assets, banking stocks, and diversified tools such as ETFs, aims to maintain or improve investment income and overall profitability, which should enhance earnings stability.

- The company's commitment to sustained dividend growth, supported by robust financial performance and strategic execution, is expected to bolster investor confidence and potentially increase shareholder returns.

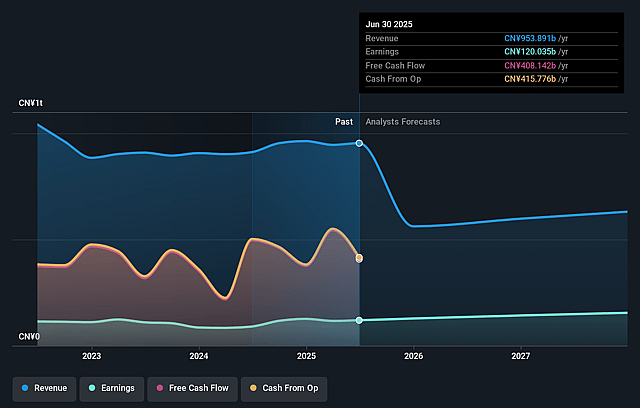

Ping An Insurance (Group) Company of China Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Ping An Insurance (Group) Company of China's revenue will decrease by 11.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 12.6% today to 24.1% in 3 years time.

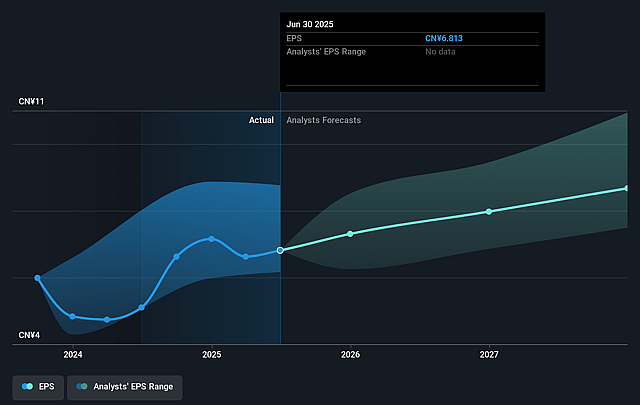

- Analysts expect earnings to reach CN¥162.1 billion (and earnings per share of CN¥9.22) by about September 2028, up from CN¥120.0 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as CN¥137.3 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 10.0x on those 2028 earnings, up from 8.7x today. This future PE is greater than the current PE for the CN Insurance industry at 7.8x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.12%, as per the Simply Wall St company report.

Ping An Insurance (Group) Company of China Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's heavy reliance on the Chinese economy, especially with its extensive investments in local banking stocks, exposes it to risks associated with China's economic fluctuations, potentially impacting future investment returns and profitability.

- Ping An's significant exposure to the insurance sector, particularly life insurance in a low interest rate environment, might compress margins and affect net margins due to reduced return from investment portfolios that support long-term insurance obligations.

- The ongoing competition and pricing pressures in the insurance industry could affect Ping An’s market share and profit margins, as intensified competitive dynamics may force the company to lower premiums or offer more costly benefits to retain customers, impacting revenues and earnings.

- While technology investments and AI integration appear to be strategic priorities, the high investment costs could outweigh the immediate financial benefits, potentially impacting net profits if efficiency gains do not materialize swiftly.

- Despite the reported higher CII, the shift towards more high-return investments such as equity markets increases market risk and volatility, potentially impacting the stability of future investment income and overall earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CN¥68.903 for Ping An Insurance (Group) Company of China based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CN¥81.33, and the most bearish reporting a price target of just CN¥58.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CN¥672.9 billion, earnings will come to CN¥162.1 billion, and it would be trading on a PE ratio of 10.0x, assuming you use a discount rate of 9.1%.

- Given the current share price of CN¥57.78, the analyst price target of CN¥68.9 is 16.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.