Last Update 03 Nov 25

Narrative Update on LEM Holding

Analysts have maintained their fair value estimate for LEM Holding at CHF 765.00. This reflects stable expectations and minimal recent shifts in key financial assumptions.

Valuation Changes

- Fair Value Estimate remains unchanged at CHF 765.00.

- Discount Rate has risen slightly, moving from 5.82% to 5.94%.

- Revenue Growth projection is virtually flat and maintains at 9.42%.

- Net Profit Margin is stable, holding at approximately 15.76%.

- Future P/E Ratio has increased marginally from 14.55x to 14.60x.

Key Takeaways

- Strategic expansion and R&D investments aim to improve competitiveness, revenue, and cost efficiency, enhancing margins and profitability.

- Growth in Chinese market shares, especially in automotive and renewable energy, is poised to elevate revenues and regional earnings.

- Increased competition, pricing pressure, and financial strain on cash flow and equity could challenge LEM Holding's future earnings and capital raising ability.

Catalysts

About LEM Holding- Provides solutions for measuring electrical parameters in China, Japan, South Korea, India, Southeast Asia, Europe, Middle East, Africa, NAFTA and Latin America.

- The Fit for Growth performance improvement program is aimed at enhancing competitiveness by optimizing operating expenses and the organizational setup, which could positively impact future net margins and profitability.

- Continued investment in research and development (R&D) and innovation, particularly in expanding the product portfolio and opening new R&D centers, aims to drive revenue growth through the development of new markets and applications.

- The strategic expansion into lower-cost manufacturing locations in Malaysia, China, and Bulgaria is expected to improve cost efficiency and potentially enhance gross margins over time.

- The stabilization and potential growth of the Chinese market, as reflected in the increased market share in automotive and renewable energy sectors, could lead to higher revenues and improved earnings from this region.

- The introduction of new ERP systems and digitalization initiatives in SG&A functions are expected to lead to increased operational efficiency, potentially improving net margins in the future.

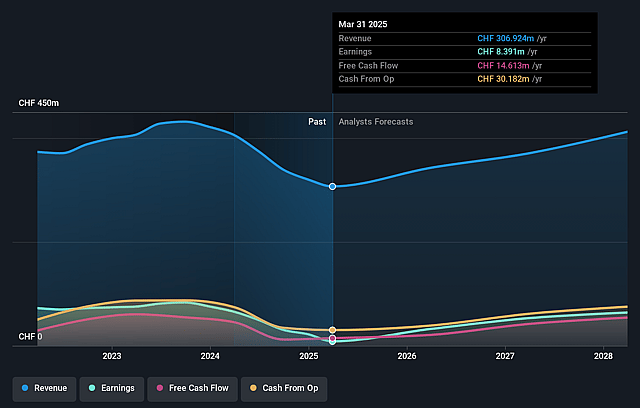

LEM Holding Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming LEM Holding's revenue will grow by 9.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 1.9% today to 16.7% in 3 years time.

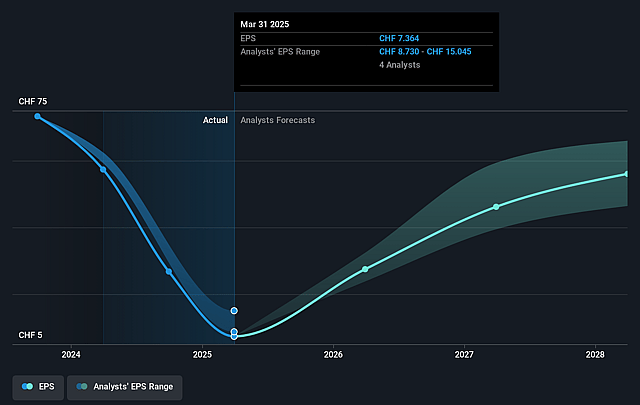

- Analysts expect earnings to reach CHF 66.3 million (and earnings per share of CHF 41.44) by about September 2028, up from CHF 5.6 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as CHF40.3 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 15.2x on those 2028 earnings, down from 100.5x today. This future PE is lower than the current PE for the GB Electronic industry at 32.5x.

- Analysts expect the number of shares outstanding to decline by 0.06% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.66%, as per the Simply Wall St company report.

LEM Holding Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company reported a significant 30% drop in sales due to high levels of destocking at customers, impacting revenue and net margins.

- LEM's equity ratio fell to 35% following a dividend payout and low net profit, which could impact the company's financial stability and its ability to raise capital.

- The net working capital increased significantly due to inventory growth and low sales, which could further strain cash flow and limit operational flexibility.

- The company's order backlog has returned to pre-COVID levels, suggesting a lack of forward sales visibility, which may limit future earnings growth.

- There's increased competition and pricing pressure, particularly from newer Chinese market players, which could negatively impact revenue and profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CHF851.667 for LEM Holding based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CHF940.0, and the most bearish reporting a price target of just CHF800.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CHF397.4 million, earnings will come to CHF66.3 million, and it would be trading on a PE ratio of 15.2x, assuming you use a discount rate of 5.7%.

- Given the current share price of CHF494.5, the analyst price target of CHF851.67 is 41.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on LEM Holding?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.