Key Takeaways

- Improved operational efficiency through better resource management and scheduling enhances capacity and potentially boosts earnings.

- Focus on infrastructure expansion and strategic pricing supports revenue growth and margin improvement.

- Macroeconomic softness and operational challenges reduce revenue growth, while labor disruptions and decreased volumes impact net margins, leading to financial strain.

Catalysts

About Canadian National Railway- Engages in the rail, intermodal, trucking, and marine transportation and logistics business in Canada and the United States.

- Implementation of the scheduled operating plan has led to improved car velocity and train speeds, indicating greater operational efficiency, which should positively impact earnings through better customer service and increased capacity for volume handling.

- Adjustments to resource levels, particularly in labor and equipment, to more closely match anticipated demand, are expected to drive margin improvement, impacting net margins positively by reducing unnecessary costs.

- Strong pipeline of customer-specific growth initiatives, which are unique to the CN network, is anticipated to drive over half of future volume growth, potentially increasing future revenues.

- Expansion and optimization efforts, including double-tracking in key areas, to accommodate growth in energy, bulk, and intermodal markets, are geared toward enhancing infrastructure capacity, expected to boost future earnings and revenue streams.

- Management's focus on pricing ahead of rail inflation combined with incremental margin improvements is set to support the delivery of a high single-digit EPS growth CAGR, impacting both revenue and net margins.

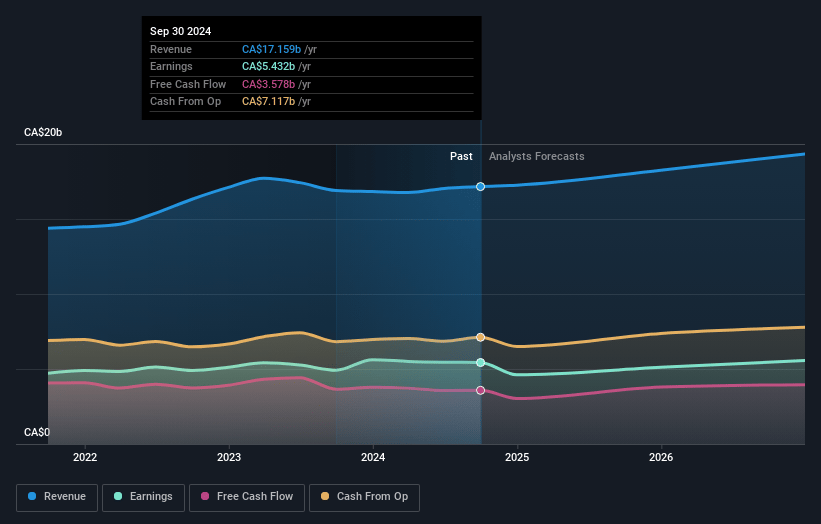

Canadian National Railway Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Canadian National Railway's revenue will grow by 4.9% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 31.7% today to 28.9% in 3 years time.

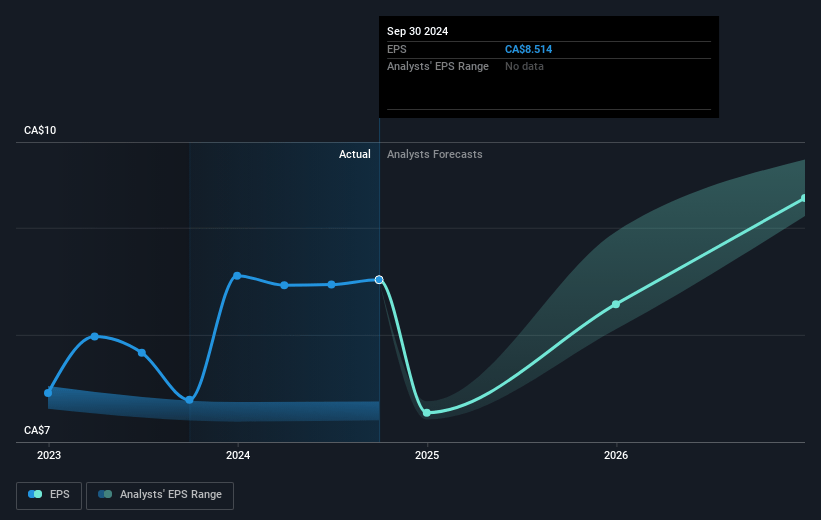

- Analysts expect earnings to reach CA$5.7 billion (and earnings per share of CA$9.74) by about January 2028, up from CA$5.4 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 21.4x on those 2028 earnings, up from 17.5x today. This future PE is greater than the current PE for the US Transportation industry at 21.2x.

- Analysts expect the number of shares outstanding to decline by 2.21% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.72%, as per the Simply Wall St company report.

Canadian National Railway Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The macroeconomic environment is softer than expected, particularly impacting the merchandise business, construction, and automotive sectors. This could lead to lower-than-expected revenue growth.

- Labor uncertainty and disruptions, such as work stoppages and forest fires, have previously caused operational challenges and financial strain, impacting net margins due to increased costs and inefficiency.

- Reduced volumes compared to expectations have led to adjustments in resources, such as halted hiring and furloughs. This could hurt earnings if the anticipated demand does not materialize.

- Decreased automotive volume, attributed to rising dealer inventories and plant retooling, could continue to depress revenues and net margins in this sector.

- Oversupply of truck capacity and market softness in domestic intermodal could result in lower-than-anticipated volume growth and associated revenues in this segment.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CA$171.24 for Canadian National Railway based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$200.0, and the most bearish reporting a price target of just CA$155.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CA$19.8 billion, earnings will come to CA$5.7 billion, and it would be trading on a PE ratio of 21.4x, assuming you use a discount rate of 6.7%.

- Given the current share price of CA$151.39, the analyst's price target of CA$171.24 is 11.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives