Key Takeaways

- Strong revenue growth and increased orders indicate rising demand and promising future revenue for Tantalus' grid modernization platform.

- Executive talent additions will bolster strategic initiatives and optimize future earnings amid structural industry tailwinds.

- Heavy reliance on existing customers and economic uncertainties may impact future revenue, with tariffs and project delays further challenging financial targets and earnings expectations.

Catalysts

About Tantalus Systems Holding- A technology company, provides smart grid solutions in Canada and the United States.

- Tantalus’ strong start in revenue growth of 27% year-over-year and converting the second highest amount of orders at $19.5 million indicates increasing demand for its grid modernization platform, likely resulting in continued revenue growth.

- The widespread electrification and increased electricity demand forecasted to double by 2050, coupled with federal investment projections of $1.4 trillion over the next 5 years, provide structural tailwinds that should drive future revenue.

- Adoption of Tantalus' TRUSense Gateway by 33 utilities shows the potential for further expansion, representing approximately $100 million in opportunities, a significant catalyst for revenue growth.

- With gross profit margins increasing and staying robust, improvements in product mix, and enhanced efficiency in the Connected Devices segment, the company is positioned to maintain or improve net margins.

- The addition of new executive talent with extensive financial and operational experience, such as the new CFO and COO, is expected to support strategic growth initiatives, optimizing earnings in the future.

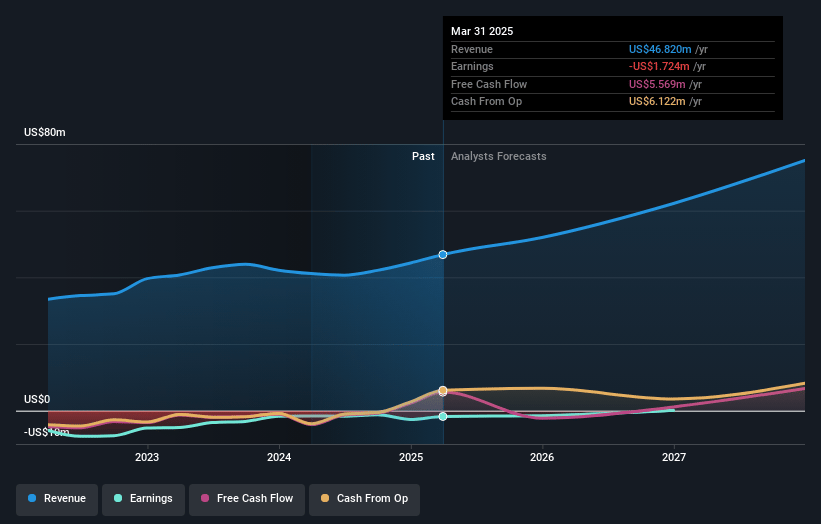

Tantalus Systems Holding Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Tantalus Systems Holding's revenue will grow by 18.9% annually over the next 3 years.

- Analysts are not forecasting that Tantalus Systems Holding will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Tantalus Systems Holding's profit margin will increase from -3.7% to the average CA Electronic industry of 7.7% in 3 years.

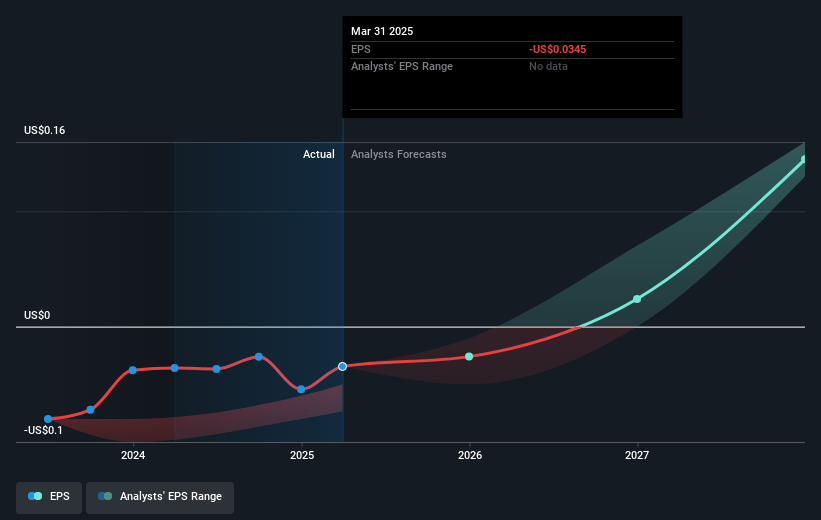

- If Tantalus Systems Holding's profit margin were to converge on the industry average, you could expect earnings to reach $6.1 million (and earnings per share of $0.12) by about July 2028, up from $-1.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 33.6x on those 2028 earnings, up from -73.1x today. This future PE is greater than the current PE for the CA Electronic industry at 21.9x.

- Analysts expect the number of shares outstanding to grow by 0.37% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.38%, as per the Simply Wall St company report.

Tantalus Systems Holding Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The implementation of a 10% tariff on Tantalus' Connected Devices, which are imported from the Philippines, could negatively impact the company's adjusted EBITDA target for 2025 by approximately $700,000 to $800,000, which may hinder net margins.

- The company's financial performance is highly dependent on existing customers, with 85% of Q1 revenue generated from this group, indicating a potential risk to revenue if these customers decrease spending or churn.

- There is ongoing uncertainty in the broader economic climate, including potential inflationary pressures and an economic downturn, which could slow utilities' grid modernization initiatives that Tantalus relies on for revenue growth.

- The long lead times for critical assets and transformers, currently at 30 months, could pose risks in terms of timing and execution for projects that Tantalus relies on, thereby impacting its revenue timelines and earnings expectations.

- While there is strong interest in the TRUSense Gateway, full deployments depend on the utilities' budgeting cycles and approval processes, which vary and may delay revenue realization, impacting the timing of future earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CA$4.45 for Tantalus Systems Holding based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$5.52, and the most bearish reporting a price target of just CA$3.2.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $78.6 million, earnings will come to $6.1 million, and it would be trading on a PE ratio of 33.6x, assuming you use a discount rate of 7.4%.

- Given the current share price of CA$3.38, the analyst price target of CA$4.45 is 24.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.