Key Takeaways

- Docebo's AI-driven transformation and recent product releases are expected to boost revenue, enhance customer engagement, and improve net margins.

- Achieving FedRAMP status and partnerships with integrators aim to expand market access and drive predictable revenue growth.

- Gen AI and automation risks, complex procurement, lowering net retention, fierce SMB competition, and leadership changes pose revenue and margin challenges for Docebo.

Catalysts

About Docebo- Operates as a learning management software company that provides artificial intelligence (AI)-powered learning platform in North America and internationally.

- Docebo's recent product releases, including community and analytics components, have shown early positive impacts and are expected to drive future growth, which could increase revenue and improve earnings in the coming years.

- The company's strategy to transform into an AI-first learning platform using generative AI and Agentic AI to automate and personalize learning experiences is likely to enhance customer engagement and retention, thereby positively impacting revenues and net margins.

- Achieving FedRAMP status by the end of Q3 2025 will enable Docebo to bid on US federal contracts, potentially driving substantial new business and increasing overall revenues.

- Increasing partnerships with system integrators (SIs), such as Deloitte, are expected to expand market access and strengthen customer wins, potentially boosting revenue and lowering operational costs, thereby improving net margins.

- Docebo's focus on long-term contracts and internal efficiencies, including leveraging AI to improve sales and operations, is anticipated to lead to more predictable and consistent revenue growth, while enhancing net margins and operating leverage.

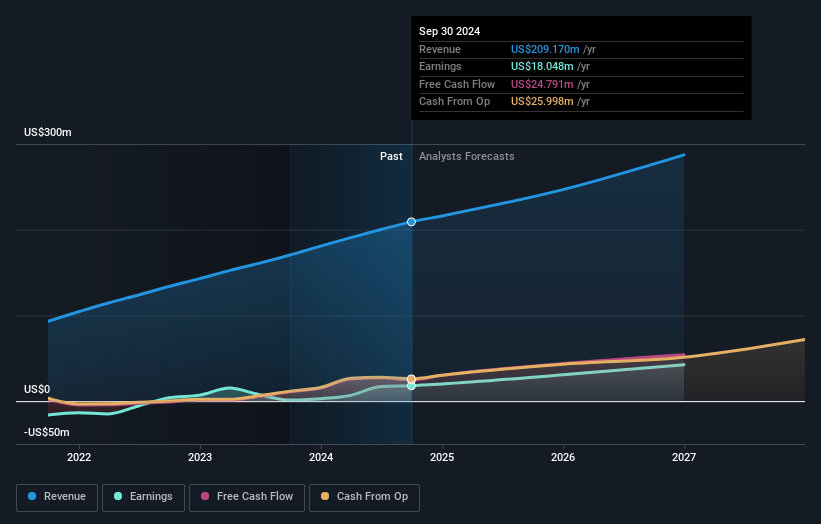

Docebo Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Docebo's revenue will grow by 10.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 12.3% today to 16.5% in 3 years time.

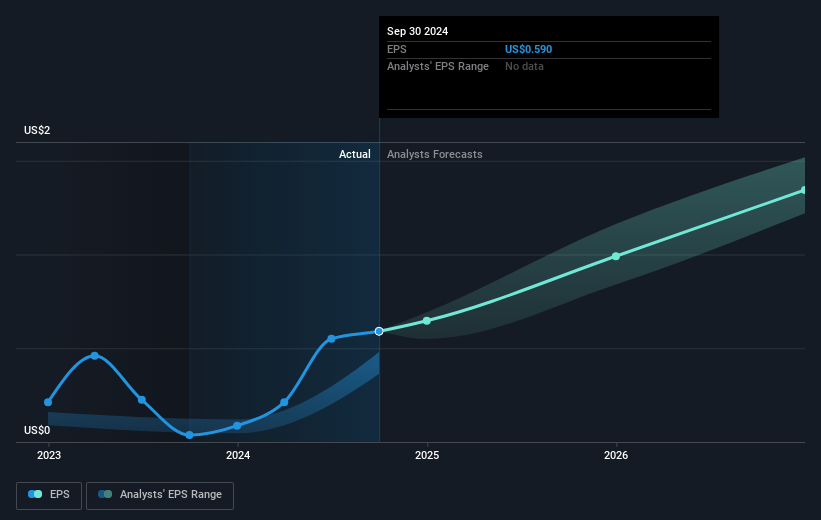

- Analysts expect earnings to reach $48.3 million (and earnings per share of $1.5) by about May 2028, up from $26.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 35.4x on those 2028 earnings, down from 35.8x today. This future PE is greater than the current PE for the CA Software industry at 32.2x.

- Analysts expect the number of shares outstanding to decline by 0.34% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.25%, as per the Simply Wall St company report.

Docebo Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The introduction of Gen AI and automation could lead to a reduction in head count, posing a potential risk of reducing seats or causing downsells, which could impact future top-line revenues.

- Complex procurement processes in enterprise deals create challenges in accurately forecasting quarterly results, which could impact revenue projections and financial performance.

- The net retention rate has decreased from 104% to 100%, partly due to customers downsizing to lower tiers, which may lead to future challenges in maintaining and growing revenue from existing customers.

- Significant competition in the SMB space, described as a race to the bottom, could lead to pricing pressures and lower-than-expected revenues if market dynamics shift in the broader enterprise space.

- Changes in leadership roles and internal restructuring could create execution risks and impact the ability to maintain or grow revenue and net margins during extended periods of strategic transformation.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CA$66.184 for Docebo based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$74.85, and the most bearish reporting a price target of just CA$57.52.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $293.5 million, earnings will come to $48.3 million, and it would be trading on a PE ratio of 35.4x, assuming you use a discount rate of 7.3%.

- Given the current share price of CA$43.76, the analyst price target of CA$66.18 is 33.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.