Key Takeaways

- Mounting regulatory, ESG, and societal pressures threaten project permitting, increase costs, and may constrain Kinross's ability to grow production and earnings.

- Diminishing high-grade reserves, digital asset competition, and industry consolidation risk eroding margins, weakening the revenue base, and challenging long-term growth prospects.

- Operational excellence, financial discipline, and strategic growth initiatives position Kinross to boost earnings, sustain production, and enhance shareholder returns over the long term.

Catalysts

About Kinross Gold- Engages in the acquisition, exploration, and development of gold properties principally in the United States, Brazil, Chile, Canada, and Mauritania.

- Persistent regulatory and societal pressures on the mining industry are likely to intensify, leading to lengthier and more uncertain permitting for key growth projects like Great Bear and Lobo-Marte; this threatens to defer or derail production ramp-ups and ultimately constrain future revenue and cash flow growth.

- The increasing adoption of digital and decentralized assets, such as cryptocurrencies, undermines traditional investor demand for physical gold, which could depress long-term gold prices and erode Kinross's revenue base and potential for margin expansion even as production rises.

- Ongoing depletion of high-grade ore at core assets, combined with the company's limited greenfield exploration focus, raises the risk that future development will be forced to process lower-grade, higher-cost material, thereby compressing net margins and weighing down long-term earnings growth.

- Kinross's major growth and mine-life extension projects face rising capital intensity and higher compliance costs due to accelerating ESG requirements and carbon regulation, which could result in persistent cost escalation and reduced returns on invested capital, despite efforts to maintain operational discipline.

- Heightened competition for quality assets and a consolidating industry landscape may pressure Kinross into overpaying for acquisitions or cause it to miss out on critical assets, stalling production growth and potentially leading to a decline in earnings and compressed valuation multiples over time.

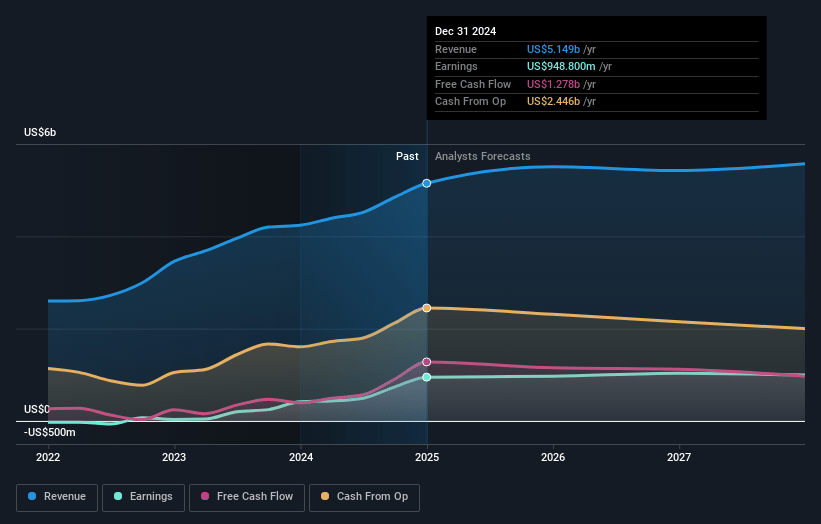

Kinross Gold Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Kinross Gold compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Kinross Gold's revenue will decrease by 3.3% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 21.7% today to 17.5% in 3 years time.

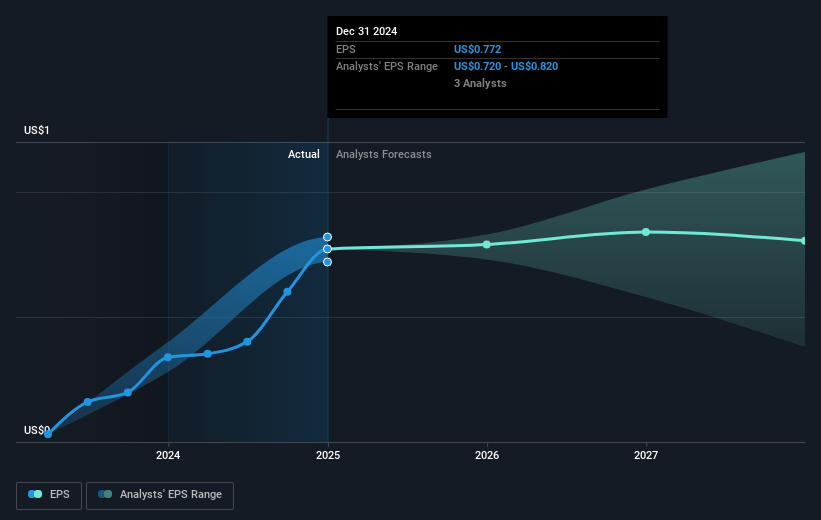

- The bearish analysts expect earnings to reach $878.5 million (and earnings per share of $1.07) by about July 2028, down from $1.2 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 15.8x on those 2028 earnings, down from 16.2x today. This future PE is lower than the current PE for the CA Metals and Mining industry at 16.2x.

- Analysts expect the number of shares outstanding to decline by 0.18% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.69%, as per the Simply Wall St company report.

Kinross Gold Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Sustained operational improvements, strong production execution, and successful grade enhancement strategies at key assets like Tasiast and Paracatu are translating into high margins and robust free cash flow, supporting the potential for improved earnings and stronger net margins over the long term.

- The company's disciplined financial management, demonstrated by substantial debt reduction, a net cash position outlook, and a focus on shareholder returns through a large dividend and aggressive share buyback program, is likely to enhance shareholder value and support higher earnings per share.

- A deep portfolio of organic growth projects and mine life extension opportunities, such as Great Bear, Curlew, Phase X, and ongoing brownfield exploration, underpins Kinross's ability to sustain or potentially grow production levels over the next decade, providing stability and upside for long-term revenues.

- Strong relationships with key stakeholders, including positive and constructive First Nations negotiations and supportive moves toward streamlined permitting processes in Canada, could accelerate project development and reduce risk of delays, enhancing the timeline for bringing new high-margin ounces online and positively impacting future revenues and cash flow.

- Continued investment in technical excellence, process optimizations (such as improved recoveries from gravity circuits), and ESG leadership positions Kinross to benefit from industry consolidation around sustainable producers, broaden its capital access, and command premium market valuations, all of which can contribute to higher long-term earnings and valuation multiples.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Kinross Gold is CA$12.8, which represents two standard deviations below the consensus price target of CA$23.84. This valuation is based on what can be assumed as the expectations of Kinross Gold's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$29.8, and the most bearish reporting a price target of just CA$10.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $5.0 billion, earnings will come to $878.5 million, and it would be trading on a PE ratio of 15.8x, assuming you use a discount rate of 6.7%.

- Given the current share price of CA$21.81, the bearish analyst price target of CA$12.8 is 70.3% lower.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.